Introduction

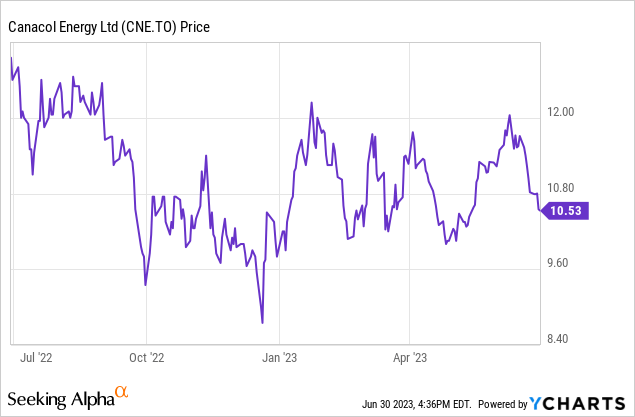

I have been following Canacol Energy (TSX:CNE:CA) (OTCQX:CNNEF) for a while here at Seeking Alpha and although I’m looking to generate capital gains on the back of an increasing natural gas production and increasing reserves, the share price has gone nowhere in the past three years as the stock is now trading about 50% lower than three years ago. As the natural gas price in Colombia is very flat, Canacol did not partake in the natural gas hype in 2022 in North America and Europe. And while the predictability of the natural gas price has its advantages, the lack of volatility means there are very few punters and Canacol should not be bought as an option on the natural gas price. Fortunately the dividend yield of around 10% keeps me happy, while the company invests its incoming operating cash flow on its assets in an attempt to further increase the reserves.

The cash flows remain robust, but the capex remains high

The average production rate in the first quarter of the year was approximately 185,500 Mcf per day resulting in an oil-equivalent production of around 33,000 barrels per day. The company also produced just under 600 barrels per day of oil, resulting in a total production of 33,600 barrels of oil-equivalent and a net production of 33,133 boe/day (after deducting the natural gas used during the production process).

Canacol Energy Investor Relations

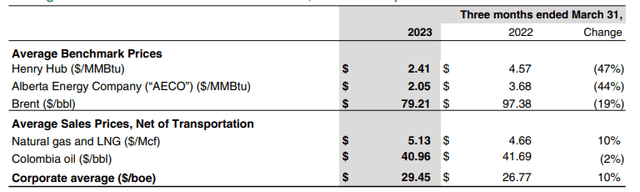

As you can see above, the average realized natural gas price was US$5.13, an increase of 10% compared to the first quarter of 2022, and substantially higher than the North American natural gas prices. So while Canacol didn’t see a spike in its realized price in 2022, it’s also not seeing the natural gas price drop to the same extent as in North America.

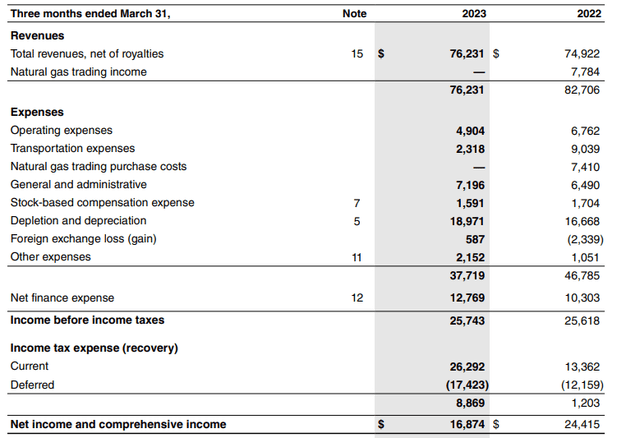

Canacol Energy reports its financial results in US dollars and the total revenue in the first quarter came in at US$76.2M. That’s lower than in the first quarter of last year, but the simple explanation is that the company did not do any natural gas trading. That boosted the total revenue in Q1 last year, but the margins were relatively thin (about 4%). So while the revenue decreased, so did the operating expenses as there obviously also were no expenses related to the natural gas trading.

Canacol Energy Investor Relations

The total operating expenses were less than $38M and about half of that was related to depreciation and depletion expenses. And while the net finance expenses increased, the pre-tax income of $25.7M and the net income of $16.9M were still very strong. On a per share basis, the EPS was $0.49, and that’s approximately C$0.65 per share.

The cash flow result is even more important than the reported net income, as Canacol Energy will be spending quite a bit of cash this year on its properties.

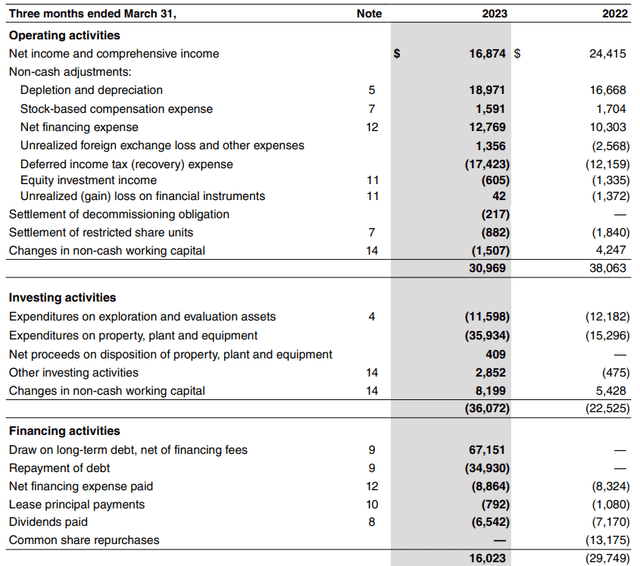

As you can see below, the operating cash flow was $31M but this included a $1.5M investment in the working capital position and excluded the approximately $9.5M in interest and lease payments. On an adjusted basis, the operating cash flow was $23M. This would have been around $40M after normalizing the cash tax payments.

Canacol Energy Investor Relations

This still wasn’t enough to be cash flow positive as Canacol spent about $47.5M on capital expenditures. This isn’t a surprise as Canacol currently is investing heavily in its assets to boost the reserves ahead of the completion of a new pipeline to serve the Medellin market.

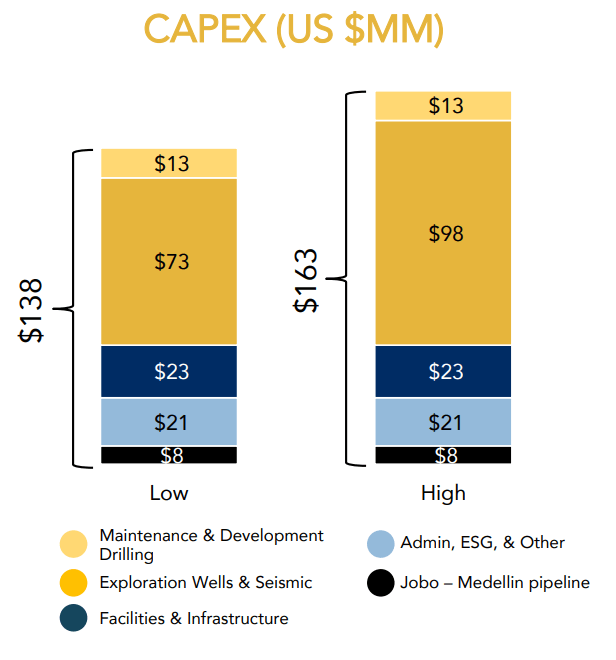

The full-year capex guidance remains unchanged at $138-163M, which represents an average of $35-40M per quarter. This means Canacol’s Q1 capex was trending above the average for this year and the capital expenditures will be lower in the next few quarters.

Canacol Energy Investor Relations

The exploration activities are starting to pay off and in the most recent update, Canacol disclosed a new well (Lulo 2) encountered 230 feet of net gas pay. The well will now be cased and completed and tied into the gas treatment facility. This will help to prepare the company for an anticipated increase in the demand for natural gas in Colombia in the second half of the year as Canacol expects a positive impact from the El Nino season.

While the company continues to aggressively drill and prepare wells, it continues to pay a rather generous dividend. The next quarterly dividend of C$0.26 per share will be payable on July 17 and on an annualized basis, the dividend yield is now almost 10%. As Canacol is a Canadian company, Canadian dividend withholding taxes will be withheld where applicable.

Investment thesis

While I was originally pursuing capital gains with my investment in Canacol Energy, I now have to be happy with the generous 10% dividend yield. Fortunately the company’s cash flow results are very strong and the current negative free cash flow result is solely caused by the very high investment in the gas project to boost the reserves and get the output capacity ready for when the new Medellin pipeline will be completed.

So I will just have to be patient. Canacol Energy is doing all the right things and I’m still getting a 10% dividend yield while I wait for the share price to move. With in excess of $70M in cash on the balance sheet and no debt maturities before 2027, Canacol can easily continue to invest in its properties.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here