Zurn Elkay Water Products Corporation (NYSE:ZWS) has experienced a recent recovery in operating margins along with share price performance. I believe that the company is currently a hold even though the company has experienced recovery, a solid dividend, and product innovation due to overvaluation assuming my DCF figures and share dilution over the years.

Business Overview

The Zurn Elkay Water Products Corporation develops, acquires, manufactures, and markets water management products internationally, including in the US and Canada. Under the Zurn and Wilkis brand names, the company provides an extensive range of water safety and control solutions. Interceptors, water control and backflow systems, fire prevention tools, PEX pipework and tubing, valves, fittings, and installation equipment are some of the items on this list.

Zurn Elkay Water Solutions Corporation offers flow system products such point drains, fire hydrants, fixture carriers, chemical systems for drainage, intercepting devices and separators, neutralizing acid systems, and surveillance systems as well as water safety and control. Zurn and Green Turtle are the brands that are used to market these goods.

The firm also specializes in the design, production, and marketing of alerts, applications, and services for remote tank monitoring. This area of the company focuses on delivering effective and trustworthy tank-level monitoring.

A variety of sensor-operated flush valves are also available from Zurn Elkay Water Solutions Corporation under the Aquaflush, AquaSense, and AquaVantage names. They offer water-saving fixtures under the EcoVantage and Zurn One brands in addition to heavy-duty commercial faucets under the AquaSpec brand. Under the Just Manufacturing brand, the company’s product line includes stainless steel items like sinks and plumbing fittings. Additionally, they provide a range of drinking water items, such as dispensers and filters.

Zurn

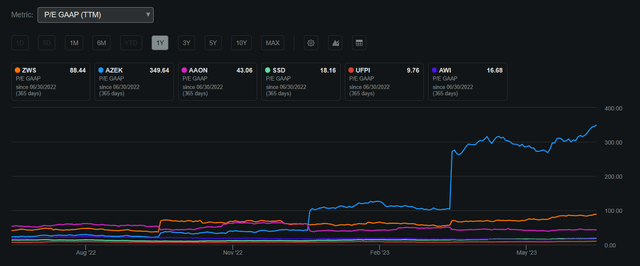

Zurn Elkay Water Solutions Corporation, currently valued at $4.7 billion, has achieved a return on invested capital of 5%. The stock price of Zurn has reached a 52-week high of $32.86 and a low of $19.29, with the current price standing at $26.89. However, it is worth noting that the company’s GAAP price-to-earnings ratio GAAP stands at 88.44, indicating a potentially higher valuation compared to its industry peers.

Zurn P/E GAAP Compared to Peers 1Y (Seeking Alpha)

Zurn Elkay Water Solutions Corporation also offers a dividend yield of 1.04%, providing investors with a potential source of passive income in addition to the potential for share price appreciation. This dividend demonstrates Zurn’s commitment to rewarding shareholders, considering its payout ratio of 66.8%. It is worth noting that the company’s free cash flow is rebounding after experiencing challenges related to profitability declines.

The sustainable payout ratio and improving FCF position indicate the resilience of Zurn’s dividend and its potential for future growth. This financial flexibility allows the company to not only support its dividend program but also invest its FCF strategically to maintain competitiveness during the recovery phase. This strategic allocation of resources contributes to Zurn’s long-term sustainability and enhances its ability to capture opportunities in the market.

An interesting observation, as anticipated, was the annual dilution of Zurn’s shares through issuance. This dilution was particularly pronounced during periods of profitability challenges and strains on free cash flow. However, this strategic approach allowed Zurn to secure sufficient cash reserves to support its core operations effectively.

Share Price Performance (Seeking Alpha)

Earnings

Zurn has delivered exceptional performance in the first quarter of 2023, exceeding market expectations despite challenging economic conditions. The company surpassed both revenue and earnings estimates, surpassing earnings per share by $0.03 at $0.18 and surpassing revenue projections by $25.11 million at $372 million, reflecting a remarkable 55% year-over-year growth. This achievement not only demonstrates Zurn’s ability to overcome profitability concerns but also highlights its robust growth trajectory and expanding profit margins. Furthermore, the company’s reaffirmed guidance for the year instills confidence and underscores its resilience in the face of adversity as it looks ahead to a promising second half of 2023.

Underperforming the Broader Market

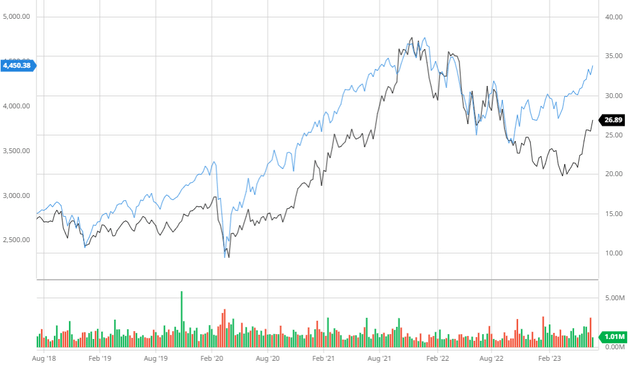

In the last 5 years, Zurn has underperformed the S&P 500 when adjusting for dividends. Although the company has seen a reduced return compared, Zurn has maintained performance until current FCF strains and has demonstrated a strong recovery on pace to outperform in the future.

Zurn Compared to the S&P 500 5Y (Created by author using Bar Charts)

Analyst Consensus

In the past three months, analysts have consistently recommended Zurn as a strong buy. However, their average price target of $26.43 suggests a slight downside of 1.72%. I believe that this projection may become more accurate as analysts incorporate the recent stock price increases and the margin recovery demonstrated in the last earnings report.

Analyst Consensus (TradingView)

Balance Sheet

Despite recent declines, Zurn maintains a relatively strong balance sheet, as evidenced by its interest coverage ratio of 5.07x. This indicates the company’s capacity to meet its debt obligations even with reduced operating income. Additionally, Zurn boasts a current ratio of 2.97, highlighting its ability to navigate uncertain times and pursue expansion opportunities in a stable environment.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

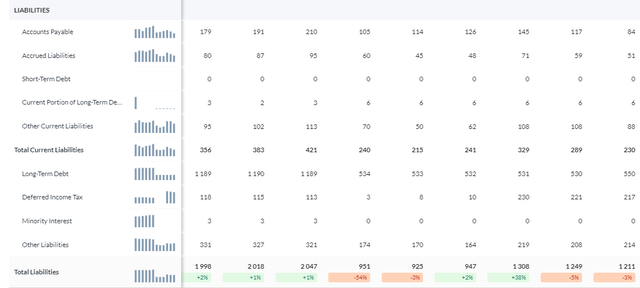

An encouraging factor lies in Zurn’s robust balance sheet, particularly in its liabilities. The company has diligently made repayments toward its long-term debt and successfully reduced its current liabilities. This strategic approach enhances Zurn’s future free cash flow flexibility, paving the way for potential expansion opportunities.

Zurn Liabilities Annual (Alpha Spread)

Valuation

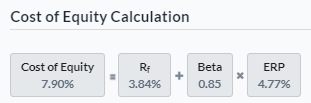

Before proceeding with my assumptions and performing a discounted cash flow analysis, I recognized the importance of determining Zurn’s Cost of Equity and Weighted Average Cost of Capital using the Capital Asset Pricing Model. With a risk-free rate of 3.84% based on the 10-year treasury yield, my calculations yielded a Cost of Equity of 7.9%. This figure represents the expected return demanded by investors to offset the risk involved in holding Zurn’s equity.

Cost of Equity Calculation (Created by author using Alpha Spread)

Using the previously mentioned Cost of Equity, I conducted a comprehensive analysis to calculate Zurn’s Weighted Average Cost of Capital. As a result, I determined the WACC to be 7.44%, which falls below the industry average of 9.82%. This indicates that Zurn’s overall cost of capital, considering both debt and equity, is comparatively lower than that of its industry counterparts.

WACC Calculation (Created by author using Alpha Spread)

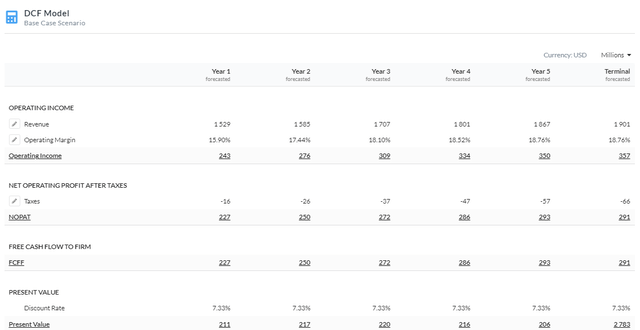

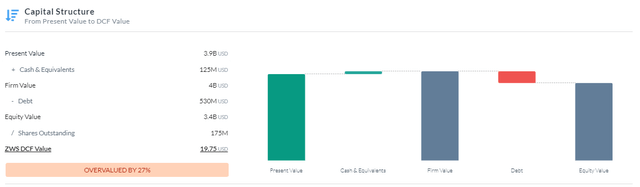

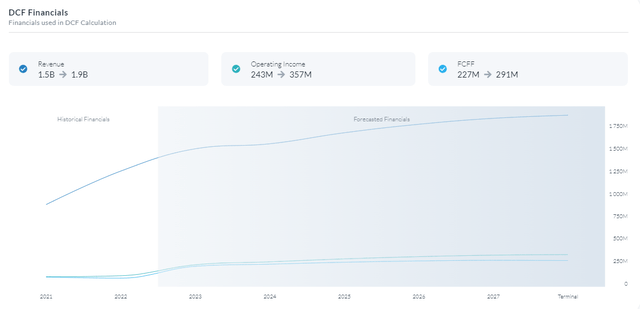

After conducting an analysis using a Firm Model DCF approach, specifically focusing on Free Cash Flow to the Firm, I have concluded that Zurn is currently overvalued by around 27%, with a fair value estimate of approximately $19.75. This valuation takes into account a discount rate of 7.33% applied over a 5-year period. Furthermore, my estimation suggests that Zurn will recover its operating margin over time and leverage product enhancements to increase its revenue potential.

5Y Firm Model DCF Using FCFF (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

Production Innovation Fostering Growth

The product innovation strategy of Zurn Elkay Water Solutions Corporation is centered on creating and providing cutting-edge water management solutions that answer their clients’ changing needs. They seek to offer cutting-edge products that improve water efficiency, sustainability, and performance by utilizing technology breakthroughs and industry knowledge.

Zurn Connected Products is one example of innovation from Zurn Elkay Water Solutions Corporation. This product line uses smart technologies and networking to improve water management’s functionality and effectiveness.

The Zurn Connected Flush Valves are just one example of the breadth of Zurn Connected Products. IoT technology is used by these flush valves to provide remote monitoring and management of water usage in business toilet facilities. The flush valves have sensors that can track usage and send information to a central system. Through a cloud-based platform or mobile app, facility managers can obtain real-time data on water use, usage patterns, and potential problems.

Zurn Connected Flush Valves have a number of advantages. First, by offering information on trends in water consumption, they enable proactive water management. Facility managers can spot high-use areas and put water-saving measures in place. Second, the remote monitoring functionality allows maintenance workers to get notifications for potential issues like leaks or malfunctions, enabling quick fixes and reducing water waste. Finally, the connectivity of these flush valves improves maintenance procedures by enabling remote diagnostics and adjustment, which eliminates the need for in-person inspections.

Zurn Elkay Water Solutions Corporation exhibits its dedication to innovation and sustainability by incorporating smart technology into its products. The Zurn Connected Flush Valves are an example of how commercial toilet facilities may use connectivity and data analytics to increase water management effectiveness, decrease water use, and improve overall performance. I believe that such innovation would enable the company to charge higher prices and still remain competitive due to additional product utility which could improve margins or offset utility lost during inflation for consumers resulting in a competitive pricing advantage.

Zurn Innovations (Zurn)

Risks

Competitive Pressures: Zurn competes against both established firms and new entrants in a very competitive market. Competitors might provide comparable goods and services for less money or with greater features, which could cause Zurn to lose market share and experience diminished profitability.

Regulatory and Compliance Risks: Zurn works in a regulated sector and is bound by a number of rules and legislation pertaining to worker safety, environmental preservation, and product safety. Failure to follow these rules may result in penalties, legal repercussions, reputational harm, and business interruptions.

Conclusion

To summarize, I believe that Zurn is currently a hold even though the company has experienced recovery, a solid dividend, and product innovation due to overvaluation assuming my DCF figures and share dilution over the years.

Read the full article here