While most retailers have given back Covid related gains, DICK’S Sporting Goods, Inc. (NYSE:DKS) remains a major winner. The sporting goods retailer benefited greatly from Covid pull forwards, but corporate moves to make the company more competitive in shipping and the positive Nike, Inc. (NKE) inventory steps should help the 2H of the year. My investment thesis remains Bullish on DICK’S Sporting Goods as the stock will likely retest strong resistance at $150.

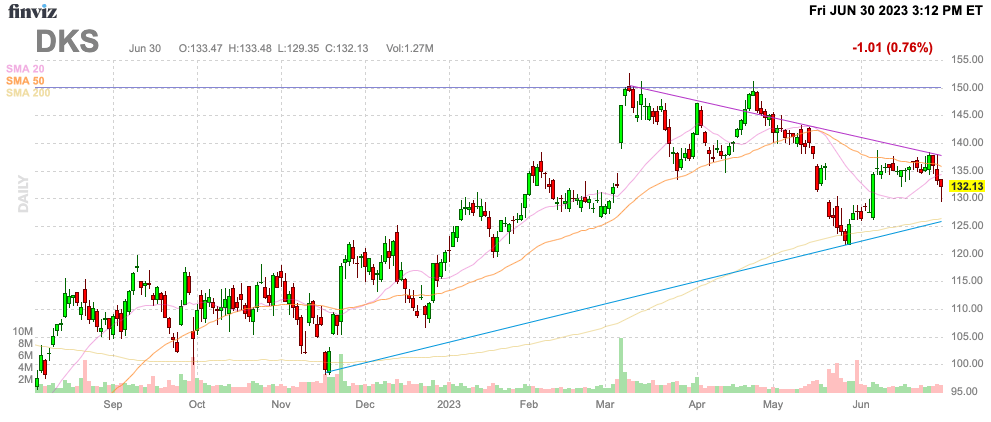

Source: Finviz

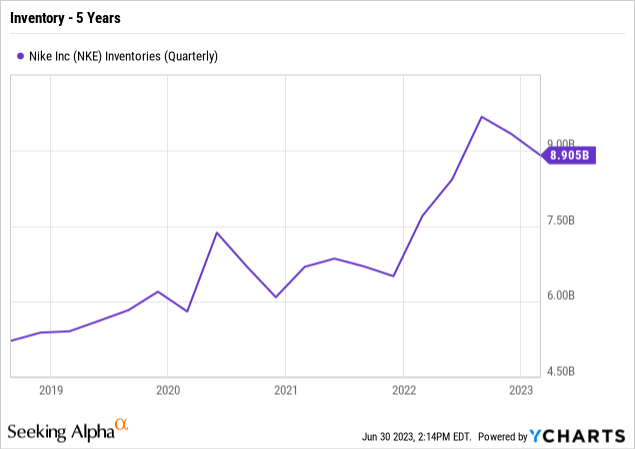

Nike Inventory

The biggest issue facing any company in the athletic apparel and footwear segment was large inventory levels at industry giant Nike. DICK’S should benefit from Nike finally getting their inventory issue under control per the company. Nike reported May inventories of $8.5 billion, down $400 million from $8.9 billion in the prior quarter.

Source: Ycharts

The inventory levels are still far above the pre-Covid levels. However, CEO John Donahoe was upbeat on the inventory levels on the FQ4’23 earnings call:

…we return to healthy inventory ahead of our competition. Our inventory is flat year-over-year in value and down in units versus 12 months ago. The actions we’ve taken position us for more profitable growth moving forward.

The CFO went further to reiterate the inventory position is far better now setting Nike up for a return to profit growth as follows:

To go a little deeper on inventory, NIKE Inc. inventory dollars are flat versus the prior year, with units down double-digits across both footwear and apparel. Apparel units are down more than 20% versus the prior year. Our mix of in-transit inventory has normalized, and days in inventory show improvement versus the prior quarter and the prior year.

DICK’S reported a solid quarter for the period ending April 29 (off one month from Nike), but the company was hit by lower margins YoY. Gross margins were down 28 basis points YoY with merchandise margins down 136 basis points.

The sporting goods retailer forecasts gross margins improvements throughout the year. The company doesn’t plan to lead with promotions and the whole sector should start moving away from lowering merchandise margins in order to clear inventory.

Guidance Looks Solid

The sporting goods sector definitely faces some headwinds with student debt repayments restarting and a potential recession, but the Nike inventory news is a big offset for the sector. DICK’S should finally be able to move forward in a more normal business environment.

DICK’S guided to FY23 EPS of $12.90 to $13.80 after a strong FQ1 and the stock no longer reflects this outcome. Analysts forecast the retailer earning $13.43 for the year leaving a 10x PE for the stock on the year ending in January.

A big dynamic investors are missing on why DICK’S can continue to report EPS close to the Covid peaks are the big improvements in the business. The company reported a FY21 EPS of $15.70 per share, so the current guidance for FY23 is definitely some giveback from those peak levels. The key is that DICK’S has maintained a large portion of those earnings from the Covid period.

On top of the sporting goods retailer becoming far more competitive with shipping options, DICK’S continues to explore other retail concepts, including a new focus on expanding premium footwear and elevated services. Any athlete regularly shopping at the main DICK’S concept knows that most sporting goods categories only carried the basics providing a great opportunity for a more premium selection and experience considering consumers can easily purchase the basics online.

The House of Sports concept is already delivering much higher sales and profits and the retailer plans to open up to 10 stores in each of the next couple of years while GameChanger now has engagement with millions of people through 2 million games covered on the platform. Newly acquired Moosejaw along with Public Lands provide store concepts to explore outdoor athlete needs and provide potential growth drivers in the years ahead.

Source: DICK’S FQ1’23 presentation

Takeaway

The key investor takeaway is that DICK’S Sporting Goods stock is just too cheap at 10x EPS targets, while the promotional issues of the sector appear headed to an end. The holiday shopping season should be clear this year, potentially providing some upside to DICK’S Sporting Goods, Inc. guidance while the stock is already cheap.

Read the full article here