Today I will take a little detour and talk about a tech-oriented stock. The technology industry has been witnessing a remarkable growth trajectory in recent years, with further snowballing by the introduction of artificial intelligence and machine learning. Advanced Micro Devices, Inc. (NASDAQ:AMD) is a significant player in the industry, widely regarded as one of the three top computer chip producers in the world alongside competitors Nvidia Corporation (NVDA) and Intel Corporation (INTC).

With AMD chips currently deployed in over 30% of the world’s computing devices, it has garnered significant attention and investor enthusiasm. Underneath this optimistic market behavior, however, is a more cautious viewpoint that contends AMD’s shares have risen in price proportionally to their price-to-earnings (P/E) ratio. This article explores the argument that the market’s exuberance surrounding Advance Micro Devices may be misplaced.

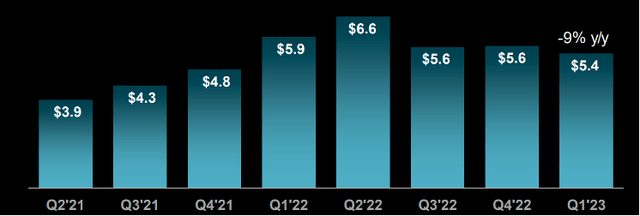

AMD had an overall revenue of $5.4 billion in Q1 2023. This figure is down 9% YoY compared to the overall revenue of $5.9 billion in Q1 2023. I believe this signals AMD’s first step into its current bear market performance.

AMD

We can clearly see since its peak revenue of $6.6 billion in Q2 2022, which coincides with the sudden boom of AI and the public release of Chat GPT, that AMD has struggled to maintain the highs of this publicity push. It has garnered less garnered significantly less market in the data center industry compared to its direct rival in that space, Nvidia.

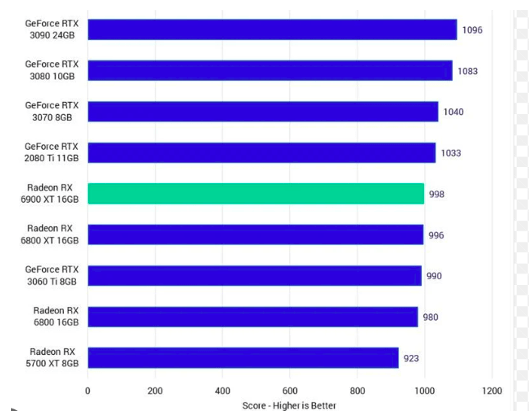

This may also be directly correlated to the performance of their GPUs. Historically and even now, Advance Micro Devices flagship GPUs just fall below their Nvidia counterpart’s line. In an industry where every minute increase in performance matters, it apparently is worth more for consumers to buy an Nvidia GPU than an AMD GPU, as seen by the graphic below.

AMD

AMD’s performance across different segments varies. The Data Center segment achieved a relatively stable operating income, while the Gaming segment saw a decline in operating income. The Client segment experienced an operating loss, while the Embedded segment witnessed a decrease in net revenue but an improvement in operating income.

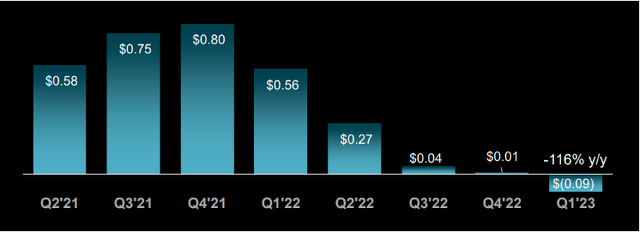

Earnings per share (EPS) for Advance Micro Devices have decreased significantly. AMD posted an EPS of $(0.09) in Q1 2023 instead of $0.56 in the same quarter the year prior, indicating a significant decline of -116% YoY.

AMD

The performance of the client segment and the effects of amortizing acquisition-related intangible assets are a few reasons AMD’s EPS declined. Due to difficulties in the client segment, there was an overall operating loss of $(145) million in the most recent quarter, significantly lower than the mammoth overall operational profit of $951 million in the prior year. This decline in operating income highlights the challenges presented by lower client segment revenue, as we discussed before, requiring AMD to restrict processor shipments below production to reduce inventory holdings dramatically.

AMD’s financial records show that the amortization of acquisition-related intangible assets has also increased significantly. These intangible assets, such as Xilinx, which was acquired last year, are frequently linked to purchasing other businesses and their technological assets to help AMD lower operational costs. While buying Xilinx may have long-term strategic advantages as Xilinx provides embedded chips like field-programmable gate arrays (FPGAs) and adaptive compute acceleration processors for AMD, the related amortization costs may harm profitability in the short term for investors like you and me.

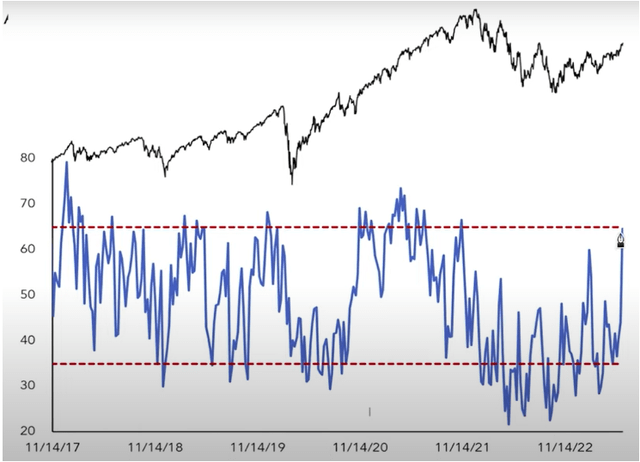

One thing I find fascinating about the market is how psychology plays a significant role. We have seen one of the biggest flips in investor sentiment recently. Back in October 2022, many investors were convinced of the bearish case, but now they have turned bullish as the market shows signs of a possible reversal, as seen in the graph below. It’s intriguing to see this shift in sentiment and how it affects market dynamics.

AMD

However, I must emphasize that this might not be the ideal moment to enter the technology market. There are indications of complacency, such as extreme levels in market indicators like the put-call ratio and the all-investor sentiment survey. These indicators have reached optimistic extremes, which can be a warning sign. It’s crucial to be cautious when everyone seems overly optimistic.

The situation could be more favorable for the future at the time of writing. The Advance Micro Devices P/E ratio stands at an astronomical level of 49.62x, indicating that the shares have become overpriced compared to the earnings generated. The market’s exuberance surrounding AMD’s growth potential due to the emphasis on the data center industry during the commercial Artificial Intelligence and Machine Learning boom has resulted in an inflated valuation that appears disconnected from the company’s current financial performance.

I believe you should exercise caution and conduct a thorough analysis of AMD’s financial health, competitive landscape, and growth prospects to determine whether the high P/E ratio is justified. It is crucial to consider the company’s ability to address challenges in its client segment, effectively manage acquisition-related expenses, and sustain or improve profitability in the future.

While Advanced Micro Devices has undoubtedly capitalized on the growing trends in AI and gaming, it is essential to temper optimism with a realistic assessment of the company’s valuation. The current market environment, coupled with concerns of an impending correction, suggests that the shares of AMD have become overpriced and vulnerable to a potential market downturn. Investors should exercise caution and carefully evaluate the risks before allocating significant capital to this high-growth but potentially overvalued stock. However, I recommend that Advanced Micro Devices, Inc. stock is a guaranteed SELL for me in this market.

Read the full article here