Dear readers/subscribers,

My articles on Brazilian businesses, which I’ve done more of the last year, haven’t really garnered much attention or interest. I nonetheless believe there to be significant value in these businesses. That is why I not only continue to write about them but continue to invest in them as well. Klabin (OTCPK:KLBAY) is a great example of this – and it showcases what sort of RoR you can make when you allow for the internationalization of your portfolio and your investments.

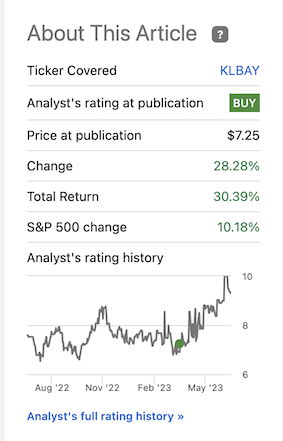

While it can be volatile at times, it can also allow developments such as this one, where you outperform the market by a factor of 3x in less than 3 months.

Klabin RoR (Seeking Alpha)

In this article, I’ll show you what we can expect if we continue to invest in Klabin after a 30% climb. Because that’s a very good RoR in a very short time.

Klabin – What upside is left after 30% in 3 months?

“Risky paper” was my description of Klabin as I started writing about the company a few months back. The appeal here is the fact that the company is one of the more significant and larger paper manufacturers on earth, and certainly the largest in all of Brazil.

35% pulp and 32% papers with a 31% conversion remain attractive prospects here. Despite a 30%+ RoR, the company can still be considered significantly undervalued by some analysts. However, the company shares the unattractive qualities of many Brazilian companies that are publicly listed, in that their trends and up/downward volatility is on the very extreme side. To give you an example – since 2016, the company’s annual EPS has trended (in Brazilian Real) from 2.39 down to 0.13, down to -2.4, up again to 2.73, up to 4.05 in the last year, and is currently forecasted by FactSet to drop 50% this year, then another 27% next year.

This makes it hard to suggest any sort of long-term valuation that could be considered “fair.”

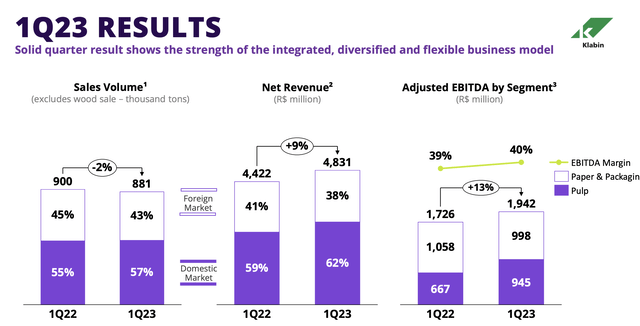

Still, the Klabin 1Q23 has been good. Revenue grew by 9%, FCF yield is up to 20.6% on a TTM basis, a good 19.4% ROIC again on a TTM basis, and the company’s debt is stable at 2.6x net debt/EBITDA – though of course there’s some degree of EBITDA coloring here since current EBITDA is at near-record levels for the company. On a normalized level, debt is somewhat more moderate.

Results are still good though – take a look at these 1Q23.

Klabin IR (Klabin IR)

Results were positive in all segments. Pulp EBITDA was positive due to pricing, diversification and good mix, and Coated board saw price adjustments resulting in increased revenues, thanks to a resilient overall market. The company is also bringing new capacity online, yet another positive with the market as it currently is.

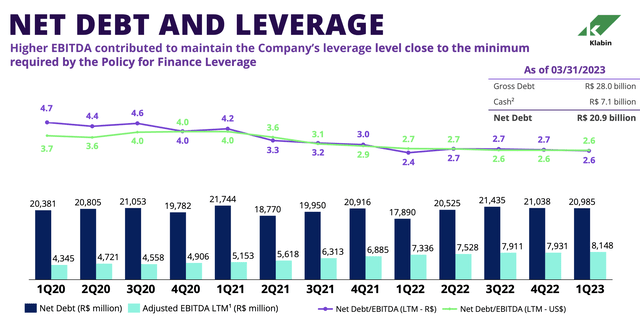

Strong OCF generation led to strong FCF, with 20.6% year-over-year growth in free cash flow, and the overall trends have been very positive for the company’s leverage. I don’t want to give the impression that leverage has only been lowered as a product of earnings – it’s both higher EBITDA and downpayment of debt.

Klabin IR (Klabin IR)

The company has 47 months of cash debt coverage on its balance sheet, with a current average debt maturity of almost 9 years and an average cost of debt of 5.4% – high, but not high in the Brazilian context. The dividend yield today is almost 8%, which sounds great – but the fact is that there are plenty of qualitative wood/fiber/paper/carton businesses which offer a very appealing yield at a good valuation at this time. And I invest in several of them, including but not limited to Billerud, Stora Enso, UPM, Holmen AB, and others.

The fact that the company is one of the highest percentile businesses in the sector isn’t surprising based on the degree of positivity in results. The company’s gross margin is close to 50%, with a net margin of close to 23% – but these are likely to be non-recurring results, which means we need to forecast the company far lower than that.

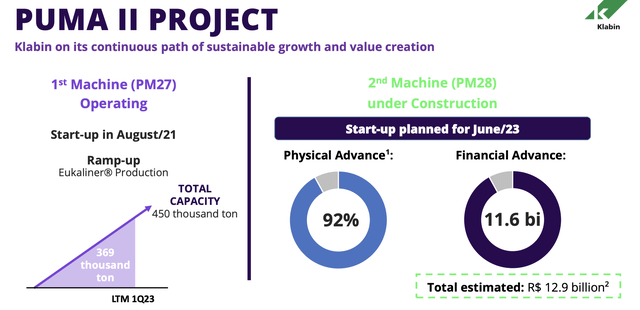

The appeal in the company is the sheer amount of new capacity it’s bringing online – PUMA II being the latest, which is planned to start up any day now, with a startup planned for June.

Klabin IR (Klabin IR)

Remember, there are currently clear trends in the industry. Graphic paper and printer paper businesses are declining. Klabin, like other businesses, including some of the Scandinavian ones I mentioned above, is moving to focus on Tissue, Containerboard, coated boards, Kraft paper and other papers. These sectors are expected to grow by at least 1% per year until 2035, securing the company’s operations and profits – theoretically.

However, most of that demand growth isn’t set to come from traditional regions such as NA, EU, or Japan, which requires the company to expand its geographical coverage and operations. While the overall paper/fiber markets are expected to expand slowly, the mix in these markets is somewhat problematic. As we’ve seen in EU and NA companies, the companies that can offer high-expertise and tailored solutions as opposed to mass-market standard cardboard/packaging solutions are being premiumized – that’s why I invest so much in Holmen AB, which has a segment that focused entirely on luxury packaging.

The “standard” business isn’t unattractive per see – but it’s more commoditized, and barriers to entry are lower. Klabin also does things that others do not, such as the manufacturing of so-called fluff, which is used in things like diapers. This is perhaps one of the things I like most about Klabin because it exposes the company to things like adult incontinence, babies, feminine hygiene, and non-woven is expected to grow at a rate of 3-5% per year, with feminine hygiene sales already firmly up over time – and Klabin is well-represented in the area.

In fact, this is relevant specifically for Klabin given its geographical exposure. Brazil is the 3rd-largest disposable diaper market in the entire world, with no sign of slowing down.

The company has an admirable degree of vertical integration. I said in my last article that I don’t expect Klabin to do much worse than any of its peers – and this has obviously and definitely come to pass here.

What I would generally be on the lookout for when it comes to Klabin now that we’ve seen 30% RoR, include the following:

- Cyclicality. This remains a very up-and-down sort of sector, and people have a tendency to forget the downside when we’re in an upside, and vice versa. Remember that paper and carton goes up and down, and we’re likely to see plenty of ups and downs here. Klabin, like most companies here, talks about preserving profitability in the light of increasing inflation and pricing as well as interest rates, but I fully expect this to start trending down, rather than up. For instance, the company is expecting a per-tonne increase of 12-13% (Source: 1Q23 Earnings call), and this is higher than most of the European peers are seeing at least in the near term.

- The company’s dependence on secondary feedstock and input, like chemicals and fuel, and how these COGS pick up or go down respectively.

- Input pricing in general remains the core question to me about Klabin – it’s what resulted in the historical ups and downs, and it’s likely what will drive the ups and downs going forward here as well – so this is what I will watch.

It’s important to mention that there’s a difference in EU pricing and others. The EU price index is more of a benchmark reference, not 100% accurate in the light of the global pulp market.

Let’s look at the company’s current valuation and what potential upside we may see.

Klabin Valuation – It’s still attractive, but the downside is becoming clearer

Klabin definitely comes with more risk now. I am not changing my conservative price target for the company at this time – not yet. My previous one was R$5.5/share, and this is still where we are today. It’s also lower than most analysts and other ways of viewing the company, which based on sales values, Graham numbers, Tangible book value, and projected FCF assign the company a valuation of close to R$8/share for the native KLBN3 ticker (Source: Gurufocus), or analysts with an average of R$25.5 for the native KLBN11 ticker, thus coming to an undervaluation of 10-20% even today. 14 analysts follow the company here, and 8 of 14 consider the company a “BUY” – but they’ve also lowered their overall PTs by about 20-25% in the last 12 months.

I want to re-emphasize at this point, that this company, in its peer group, is actually a margin leader. The peer group consists of many companies I invest in, such as UPM-Kymmene (OTCQX:UPMKY), Stora Enso (OTCPK:SEOJF), Holmen AB (OTCPK:HLMNY) and Billerud (OTCPK:BLRDY). However, I still prefer to invest in companies I view as safer, which are those mentioned in the peer group here. My own biggest position is at the moment Billerud and Stora Enso, while slowly adding to Holmen – but Klabin is definitely part of my list here as well, due to their margin and pricing power.

We have one analyst following the company – and that analyst is for the ADR KLBAY, but the company recently reached the PT here. DCF valuation methods don’t work – so we need to use relatively “rough” valuation tools, which have the drawback that they don’t account well for volatility or changes. The problem also remains that the entire sector is at a pretty good valuation, or even a great one – so while you could invest in Klabin, you can also invest in 5 other companies at similarly excellent prices, many of them without having to consider Brazilian exposure, which is not something everyone wants to go into.

This leads me to, despite outperformance, stick to my native PT to Klabin here. I’m not raising or lowering it, despite excellent performance. Despite the company’s class-leading profitability and ROIC scores, and the fact that I can’t really find any particular fundamental risk (beyond political/Brazilian/sector-specific) to the company’s operations, I want to remain conservative here.

The current target is “good enough” for the company, and where I would consider buying more. I’m not selling my stake here and may add more going forward.

Here is my thesis for Klabin.

Thesis

- Klabin S.A. is class-leading and should not be underestimated. It’s a South American paper and pulp producer, with full vertical integration in the market. Even if it’s just a fifth of the size of some of the more major players, it’s nonetheless a solid investment at the right price.

- Earnings volatility and political instability make the company difficult to compare or value properly – but I arrive at a conservative PT of R$5.5/share, based on fundamentals, sales, revenues, Graham multiples, and historicals, which implies an upside here.

- Klabin S.A. is a “BUY”, and you can invest here with a profit – as I see it.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

4 out of 5 criteria is enough for me, though this one comes with a warning of being somewhat volatile – but Klabin is a “BUY”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here