Introduction

It’s time to talk about Brookfield Infrastructure Partners LP (NYSE:BIP) and its twin, the Brookfield Infrastructure Corporation (NYSE:BIPC).

BIP/BIPC combines a number of things that I like. The company has a breathtaking portfolio of wide-moat businesses that cover every major infrastructure segment. It has consistent long-term growth, a satisfying yield, and the ability to generate satisfying long-term returns.

Even better, it comes with inflation protection and very reliable operating cash flow on top of a healthy balance sheet.

In this article, I’ll walk you through my thoughts, starting with the difference between BIP and BIPC.

BIP? BIPC? What’s The Difference?

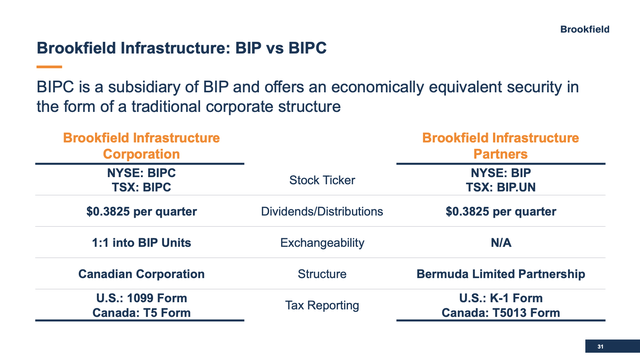

BIP and BIPC are the same company.

BIP is a Canadian Corporation. BIPC is a Bermuda limited partnership. This LP issues a K-1 form in the United States. In other words, the main difference is the tax situation.

Brookfield Infrastructure Corporation

The dividend is the same. Taxes are not. Depending on where you live, you may encounter a different tax situation. For example, in my standard brokerage account in Europe, I cannot buy BIP shares. I can only buy BIPC shares that are subject to a tax treaty between my country and Canada.

Furthermore, limited partnership shares should not be held in a Roth because if they generate more than $1,000 in dividends, the account loses its tax-advantaged status.

So, please be aware of these differences and look into what makes the most sense in your individual position. Also, bear in mind that I’m not an accountant or tax specialist.

The difference between dividend yields is based on taxes and the valuation:

- The BIP dividend is $1.53, which translates to a 4.3% yield.

- The BIPC dividend is also $1.53 (same company), yet its yield is 3.4%, which is the result of a higher valuation of BIPC shares, which is a benefit of BIP.

What’s BIP/C And Why It is So Awesome?

In my dividend account, I have roughly 50% industrial exposure. A big part of that consists of transportation stocks. I also own energy stocks and other companies that are in some way related to infrastructure.

Infrastructure isn’t just a very big segment, but it’s tangible and very important. It connects people, and it’s the foundation for every single business in the world, and while infrastructure will change, it’s a rather predictable business.

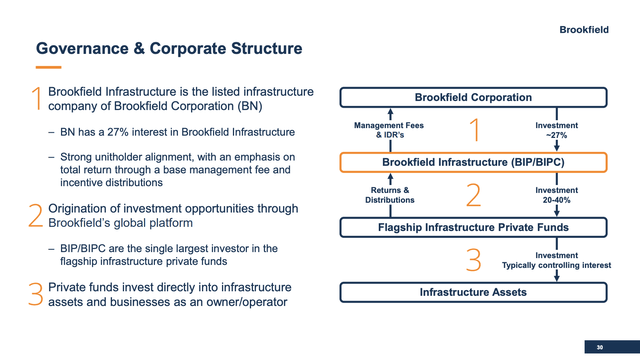

With that in mind, The Brookfield Corporation (BN) owns 27% of Brookfield Infrastructure. The company also owns 100% of the voting interest in BIP through its ownership of the general partnership unit of BIP.

Brookfield Infrastructure Corporation

Brookfield was founded in 1899 and is a Canadian multinational and one of the world’s largest alternative investment management companies. In 2022, the company had more than $700 billion in assets under management and a focus on real estate, renewable energy, infrastructure, credit, and private equity. It’s also the owner of distressed securities investment company Oaktree Capital.

With that said, BIP/C has a fantastic foundation of experienced management and resources that others simply cannot compete with. This also goes for the talent pool, as I assume that Brookfield has the resources to attract smart people who not only find opportunities but also unlock value once these assets are acquired.

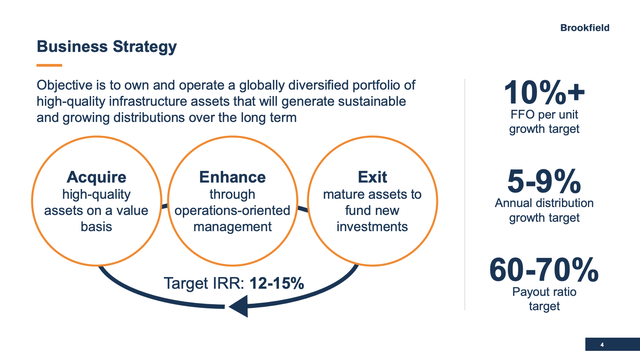

The company’s objective is to own and operate a globally diversified portfolio of high-quality infrastructure assets that will generate sustainable and growing distributions over the long term. It’s like buying dividend stocks, except that BIP/C is actively managing these assets.

As the overview below shows, the company targets an internal rate of return of at least 12%, used to sustain annual distribution/dividend growth of 5% to 9% per year, maintaining a 60% to 70% payout ratio.

Brookfield Infrastructure Corporation

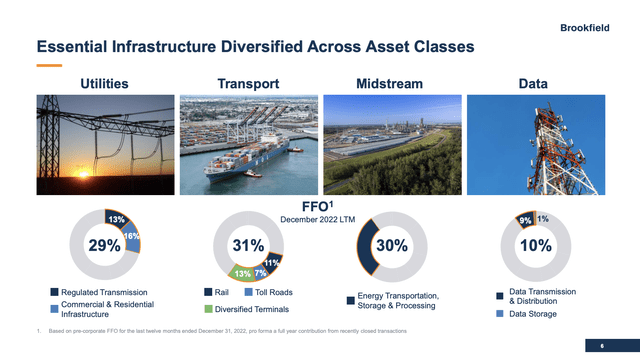

BIP/C’s portfolio consists of the four key infrastructure segments: utilities, transport, midstream (which is also a form of transport), and data. The company manages assets using 11 corporate offices in all major economic hubs around the world.

- 44% of its operating cash flow is generated in North America.

- Europe, South America, and Asia account for roughly 20% each.

- The company has almost equal exposure in utilities, transport, and midstream, with 10% data exposure.

Brookfield Infrastructure Corporation

These assets include 62,000 kilometers of operational electricity distribution and transmission lines, natural gas pipelines, almost 26,000 kilometers of gathering, transmission, and transportation pipelines, 32,3000 kilometers of rail, toll roads, 11 terminals, and two export facilities.

In the data segment, the company has more than 200 thousand telecom towers, two semiconductor manufacturing foundries, and almost 47,000 kilometers of fiber optic cable. It also has 50 data centers.

Companies include the Genesee & Wyoming railroad, which is a holding company with interest in 122 railroads in the United States, Canada, Belgium, Netherlands, Poland, and the UK.

The railroad was stock listed until it was acquired in 2019. I’m bringing this stock up because I have significant rail exposure and because that’s when I started to follow Brookfield’s acquisitions a bit. To this day, I’m impressed by the deals this company closes. I believe it owns some of the best infrastructure assets in the world.

Furthermore, in 2020, I was researching a company operating in the steel industry for a hedge fund client of mine. Brookfield had (and still has) a major stake in that company and was working on a turnaround. I really liked the company’s approach, which is why my client got interested as well.

The good news is that Brookfield Infrastructure shareholders (unitholders in case of the limited partnership) benefit from this.

Where’s The Shareholder Value?

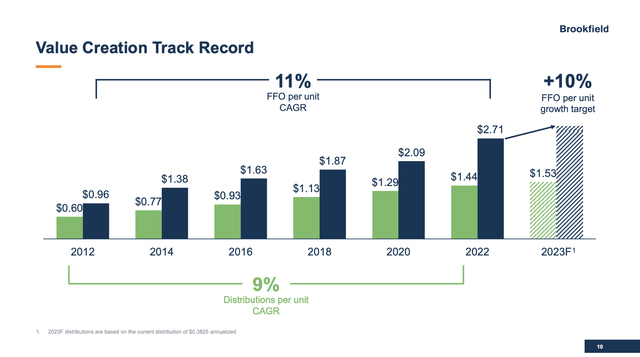

BIP/C has a terrific track record. Between 2012 and 2022, the company has grown funds from operations by 11% per year, growing its dividend by 9% per year.

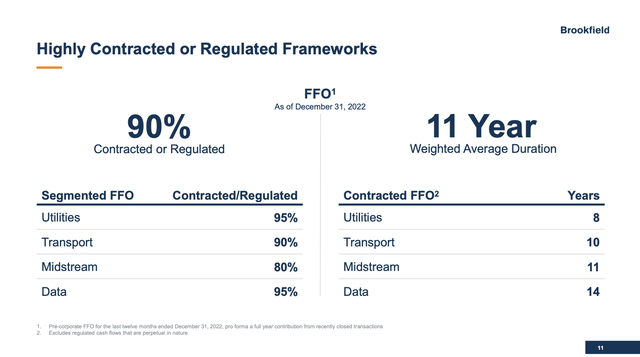

Furthermore, more than 80% of FFO is protected from or indexed to inflation, with 90% of FFO being contracted or regulated, which adds tremendous safety and stability to the company’s cash flows. It’s also not uncommon, given the firm’s exposure to midstream and utility operations.

Brookfield Infrastructure Corporation

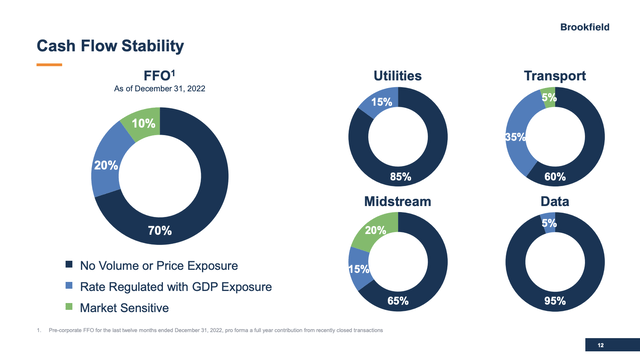

Even better, 70% of total FFO has no volume or price exposure, which does limit growth a bit, but it also protects the downside.

Brookfield Infrastructure Corporation

To put it differently, BIP/C has a well-covered, steadily rising dividend, which is backed by solid operating cash flow.

Brookfield Infrastructure Corporation

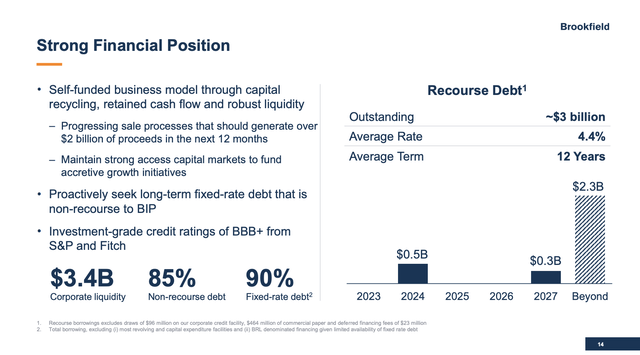

Furthermore, the company has a healthy balance sheet. In its first-quarter earnings call, BIP/C made the case that its balance sheet remained strong with excellent liquidity.

Despite capital market volatility during the quarter, the company maintained confidence in the strength of its balance sheet. S&P reaffirmed their BBB+ credit rating, and Fitch assigned them a newly secured investment-grade credit rating of BBB+. These credit ratings reflect the stability and predictability of the company’s infrastructure assets. It’s also just one step below the A-range.

Brookfield Infrastructure Corporation

The company also raised over $5 billion of capital from nine relationship banks across North America, Europe, and Asia to support their transactions. They ended the first quarter with total corporate liquidity of $2.4 billion, which will be further enhanced by proceeds expected from their capital recycling program.

Adding to that, 90% of operating cash flow is generated from companies with investment-grade debt.

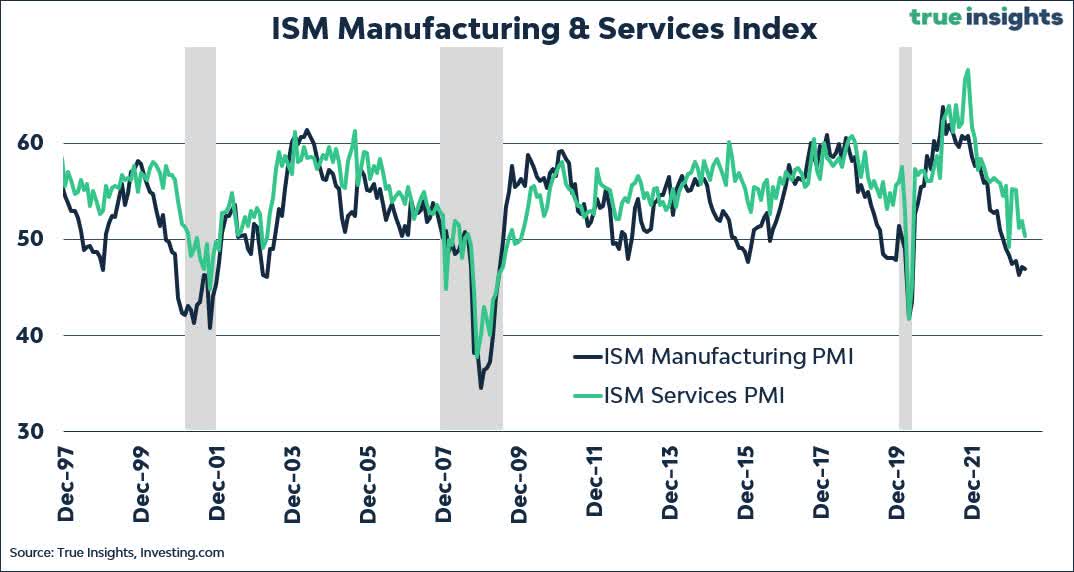

It also needs to be said that the business has proven to be extremely resilient in light of ongoing challenges. After all, this is what manufacturing and services sentiment currently looks like:

True Insights

During the first quarter of 2023, BIP/C reported strong financial and operational results. The company’s regulated and contracted business generated funds from operations of $554 million or $0.70 per share/unit, a 12% increase compared to the previous year.

Organic growth was 9%, which exceeded the company’s annual target. This growth was driven by elevated levels of inflation on tariffs, strong volumes across its transport networks, and the completion of approximately $1 billion in new capital projects over the past year.

The company also deployed about $2.4 billion in new acquisitions, contributing to its positive performance.

In addition to that, the company had a major acquisition in April, when it bought Triton International (TRTN) in a deal worth $13.3 billion, including debt.

According to Triton:

Triton leases and sells high-quality intermodal shipping containers and related equipment through a global network of more than 400 independent, third-party depots and locations across the world. Our extensive global scale enables us to deliver best-in-class service while also operating with the lowest cost ratios in the industry.

Brookfield believes that Triton’s global network, lower procurement and financing costs, high fleet utilization, and margins differentiate it from competitors.

The acquisition is expected to improve customer relationships, create organic growth opportunities, and enhance the intelligence in capital allocation for the broader transportation franchise.

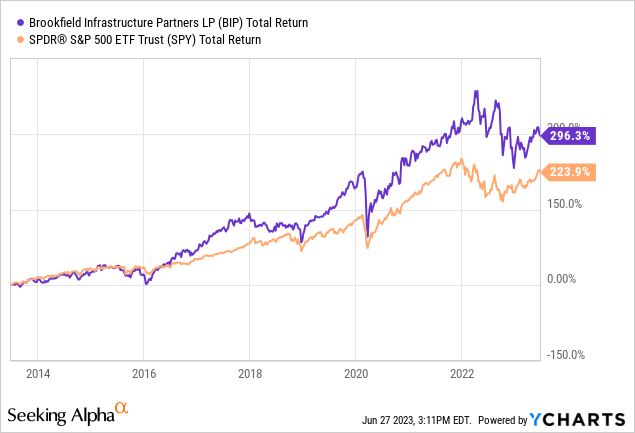

Moreover, and going back to the bigger picture, not only does BIP yield more than 4%, but it also comes with a strong total return. Over the past ten years, BIP shares have returned close to 300%, which outperformed the market by a wide margin.

While BIP doesn’t yield close to 10% like some other LPs (especially in the energy sector), I think it’s a perfect mix between growth and value.

It’s a safe dividend backed by a rock-solid business that comes with dividend growth, inflation protection, financial stability, and satisfying total returns.

If I were in the market for a safe yield and diversification, I would be a buyer of BIP – assuming I could legally buy it.

For now, I stick to building my own Brookfield, meaning buying my own infrastructure plays for my dividend growth portfolio.

Takeaway

In conclusion, Brookfield Infrastructure Partners LP and its twin, Brookfield Infrastructure Corporation, offer an impressive combination of wide-moat businesses, consistent growth, attractive yields, and satisfying long-term returns.

BIP/C stands out due to its experienced management, vast resources, and access to a talented talent pool. The company’s objective is to own and operate a diversified portfolio of high-quality infrastructure assets, actively managed to generate sustainable and growing distributions.

With a strong track record, consistently rising cash flows, and a healthy balance sheet, BIP/C offers a well-covered dividend and stability.

Despite not yielding as high as other LPs, the company strikes a balance between growth and value, making it an appealing option for investors seeking a safe yield, diversification, and satisfying total returns.

To be honest, it’s the most impressive diversified infrastructure investment I’ve come across so far.

Read the full article here