With almost €900 bl assets, 15 million customers, and a footprint spanning several EU countries, UniCredit (OTCPK:UNCRY) is the only Italian bank in the list of Global Systemically Important Banks (G-SIBs) published by the FSB. The company shares have performed very well in recent months, as the bank is seen as an apparent benefactor of the higher interest rates environment. Earnings have rapidly increased over the last year, and the company is buying back shares at a steady pace. Is an investment worth consideration? Let’s have a look to find out.

Investment thesis

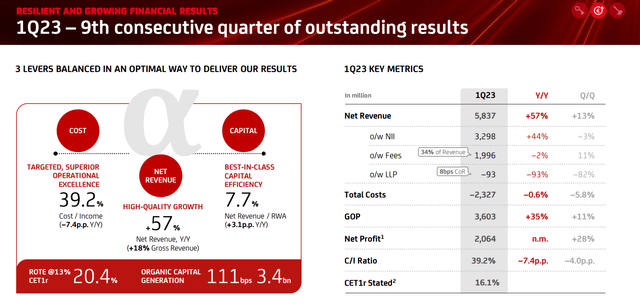

UniCredit 1Q23 results reported in May were exceptional and represented the bank’s ninth consecutive quarter of growing results. NII increase of +44% (+66% in the Italian core market) was the main driver behind the outstanding €1.06 EPS result, +186% from 1Q21 (€0.37 per share) and +54% vs. LY adjusted EPS of €0.69. The adjustment of €0.56 vs. statutory results (€0.13 EPS per share) reflects the writing off by UniCredit of its Russian assets last March. Considering the somewhat limited exposure to Russia, this painful but necessary step did not cause long-term damage.

UniCredit 1Q23 Earnings presentation

The bank, which at the beginning of 2023 low-balled its guidance, offering a profit outlook in-line with 2022 (€5.2 billion), raised it by a whopping 20% to €6.5 billion. In light of the 1Q23 results, with €2.1 billion earned, the guidance still seems conservative compared to the potential outcome.

And Value For All / company material

I don’t think 2Q23 results will be any lower than last year, which leads me to believe the bank is projecting material headwinds in the back half of the year. A 5% increase vs. 2022 in the coming quarter and a 20% decrease in the following two would leave UniCredit earning roughly €6.5 billion.

Based on the 1.94 billion shares currently outstanding, the updated EPS projection of €3.34 per share for FY23 still does not account for the ongoing buyback activity. In fact, UniCredit promised last month to return to shareholders at least €5.75 billion (90% payout ratio) out of the €6.5 billion. The current dividend estimate by analysts is €2.4 billion (€1.24 per share or 6.2% yield based on a €20 share price), which leaves another €3.4 billion available for the repurchasing activity, enough to retire 9% of the outstanding shares at current prices.

UniCredit is performing well also on the cost containment front. Driven by the bank’s digitalization and reduction of physical footprint, its 1Q23 costs decreased by 0.6% vs. the prior year, magnifying further the revenue growth and reducing the cost/income ratio to below 40%. The CET1 ratio remained strong at 16.1%, and the bank remains well above the MREL requirements set by authorities.

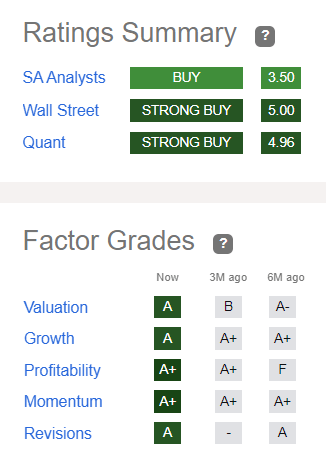

Seeking Alpha proprietary screening also highlights UniCredit as one of the most promising stocks. Besides having excellent ratings from both the analysts’ communities and Quant ratings, UniCredit earns excellent factor grades.

Seeking Alpha

Relative attractiveness against peers

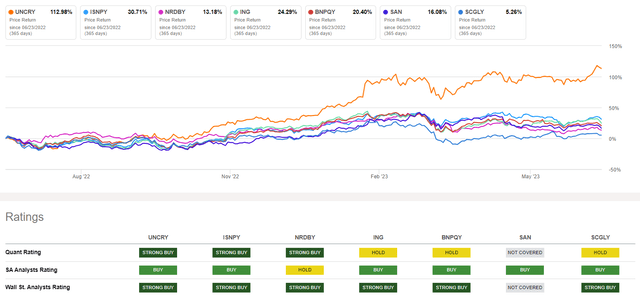

Despite the excellent optics for UniCredit, investors should note that most EU banks are currently trading at undemanding multiples. The buy case is not obvious even if UniCredit trades at 6x fwd earnings. Among other European G-SIBs, Dutch ING Groep (ING) seems richly priced and sells at 8x fwd earnings! Spanish Santander (SAN) and French BNP Paribas (OTCQX:BNPQY) trade at about 5x – 5.5x earnings, Société Générale (OTCPK:SCGLY) below 6x. Non- G-SIB Italian peer Intesa Sanpaolo (OTCPK:ISNPY) also at about 6x.

Seeking Alpha

UniCredit shares the best SA ratings of the group with Intesa, which I covered last quarter, although it is arguably hard to find a bank with negative sentiment among the pack. Intesa, like UniCredit, reported much-improved results vs. 1Q22 last month. Still, despite a 66% YoY increase in NII, the EPS increase was less pronounced than UniCredit, and the bank was not as effective in its cost/income ratio, slightly higher at 41.9%, and overall costs, which increased by 0.5%.

What really stands out is the performance of UniCredit shares, which surged compared to EU peers and Intesa. The divergence starts in September 2022. Before, the bank traded at close range with Intesa during much of the pandemic.

Seeking Alpha

With the Italian economy holding up, the effect of higher rates in motion, and Italian deposit holders seemingly willing to accept 0% interest on their bank accounts, things seem to be shaping up well in 2Q23 for UniCredit. Things could fare even better than management’s expectations for the rest of the year. Considering momentum and the analysts’ laziness in revising UniCredit’s outlook upwards, the bank could be a decent swing-trade idea. Considering management’s outlook for the rest of the year, there seems to still be a lot of sandbagging at play. If UniCredit beats estimates in Q2 and Q3, the bank could project earnings for about €7.5 billion (almost €4 per share) before an actual recession kicks in.

The upside for UniCredit would imply a short-term run-up to the €24-€28 region (6x-7x fwd P/E), which is also in line with the €25 consensus target. Under these assumptions, the highest-rewarding bullish play could be purchasing call options with strikes slightly above the current market price and a 6-9 month time frame.

UniCredit’s re-rating from 0.3x-0.4x tangible book value per share (TBVPS) to the current 0.7x based on a 1Q23 book value of almost €28.5 drove its recent outperformance vs. peers. Even if some fuel could still be in the tank, thanks to share repurchases, there’s not much of a chance to see UniCredit trading past 0.9x book value.

A sizable discount has been the norm among EU banking institutions after the GFC, but in UniCredit’s case, it was particularly steep. Nevertheless, that seemed warranted, given that the bank’s NPL situation was a total mess that took over a decade to clean out. Now that UniCredit is finally out of that tunnel, the macro situation is weakening again. I remain skeptical that the bank will continue to deliver alpha over the long term.

Stormy seas ahead

Citing the macro-outlook as a risk is a bit of a cliché. After all, not many equity investments are expected to perform well in a recession. That said, if history is any indication, banks have been among the most susceptible ones. While I am not implying that we will see another Credit Suisse (CS) event in Europe anytime soon, a glimpse of what can happen to bank stocks when investors start to run for the hills has just occurred in the US. Investors should be aware by now that when things sour in banking, they sour quickly and badly. UniCredit’s own long-term stock return looks like this:

Google

So, if the prospect of having the bank trading at €28 and more than doubling the share price since last year seems great, take a step back and put yourself in the shoes of a buy and hold shareholder who got its UniCredit shares at €35.5 in July 1993.

I question the effectiveness of aggressive share repurchase plans at a likely market peak and for a bank with a history of massive capital raises to bail out from crises. The last raise in 2017 issued 13 new UniCredit shares for every five shares owned, a 260% increase.

Also, I question the banks’ ability to profit from elevated NIM much longer. The bank does not readily share the information with investors, and the reason could be that Italian banks are currently profiteering from unreasonably high spreads. Italian bank accounts pay almost no interest, and Italians have been sluggish in moving away from cash deposits, which yielded less than 0.5% on average at the end of 2022. Nevertheless, I foresee NIM rapidly peaking out in 2023.

Italy’s general economic outlook remains somewhat of a mystery. The country, plagued by political instability, high public spending, and low wages, has arguably fared better than most expected. Regardless, the risks remain elevated. In March, I discussed the possibility that the Italian government could implement a populistic measure like a mortgage payments jubilee to harm bank profits. While that particular risk seems very low now, Italian media has recently started reporting that discussions could be ongoing regarding levying potential surtaxes on bank profits.

Add to the mix the high risk of NPLs bursting off scale again in the event of an economic downturn, and the cocktail becomes too explosive for my liking. UniCredit has an extensive portfolio tied to Italian mortgage loans. While the problems wouldn’t likely be as huge as during the GFC, they still have the potential to harm TBVPS again and subdue future profitability for years.

Conclusion

The takeaway for investors here reflects the complex and evolving macro situation and is more problematic than a simple buy or sell rating.

UniCredit’s short-term outlook seems favorable. I believe SA quant rating is correct, and I see further momentum for the stock. Upward EPS revisions, further enhanced by UniCredit’s ongoing buybacks, should be the catalyst driving the stock price, and even the TBVPS, higher. Even if NIM and NII seem to be approaching a peak, I do not think we are past it yet. Because of these reasons, I am attaching a BUY rating to UNCRY shares, with the caveat that I see this as a swing trade or an option play.

Longer-term, I am skeptical that a buy and hold position in UniCredit will bear outsized returns to investors. I am not only wary that the bank can sustain current profitability levels, but I am looking cautiously also at its strategy focused on buybacks. Investors interested in exposure to the Italian banking sector should still favor Intesa Sanpaolo instead because the bank pays out most of its profits in the form of dividends. Intesa Sanpaolo stock can probably fit specific portfolio allocations that favor high-yield income investments.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here