Dear readers/followers,

The time has come to update Sampo (OTCPK:SAXPF), a Finnish holding company for a variety of insurance-based operations. Since divesting its significant stake in Nordea (OTCPK:NRBAY), the company has changed its focus. I still hold a take in Sampo, but it’s no longer as significant or large as it once was.

Why?

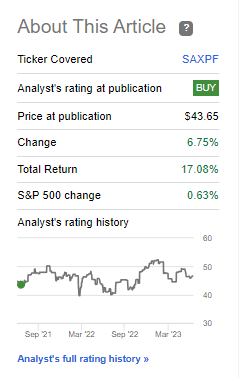

Because when the company hit €45+, it became so obviously overvalued to anything it’s likely able to perform in the next few years, that I decided to sell. Sampo isn’t a bad company, and my call from 1+ years back was actually the correct one. Take a quick look at what has happened since I made that particular call.

Seeking Alpha Sampo (Seeking Alpha)

Sampo is a very solid business with an upside. It’s essentially a multi-line insurer, and you know that I love insurance companies. However, for the past year and more, I’ve focused on other insurance companies than Sampo.

Let’s update things here and see where we are.

Sampo – A lot has changed since late 2021.

Sampo has performed nicely if we look at the market outperformance we’ve been able to get since my last article. However, leaving Nordea has also completely changed the company’s operating and income structure, as well as its earnings potential. I don’t believe the market has yet fully appreciated or normalized how different this will look in the next few years.

After the payout of Nordea shares, which we can see in the company’s earnings here, the focus of Sampo has changed to straight insurance. This is a positive change and one I applauded in most of the articles where I covered this change. A pure-play insurance company, even multi-line, is easier to cover than one with exposure to diversified banking given the different considerations and strategies for the companies. It’s a common criticism I levy on some articles and analysts – you cannot equate banks to insurance companies. Their strategies, safeties, and risks are different.

For more basic information about Sampo, I refer you to my older articles – they are still very much relevant to what the company is today.

This marks the first article in over a year where I look at Sampo as the pure-play multi-line insurer that it is. 1Q23 is the latest set of results we have for the company, and these were good.

Why were they good?

Because while some NA insurance companies boast of combined ratios of below 95%, Sampo manages sub-85% combined ratios. For 1Q23, the Sampo group Combined ratio, which is the sum of incurred losses and expenses and then dividing them by the earned premium, meaning lower is better, is 84%. The combined ratio is a good measure of the money flowing out of the company, not only in terms of losses and expenses but also dividends.

Combined ratio is arguably one of the most important metrics for an insurance business because it’s a comprehensive measure of how well they are doing their job.

Anything above 100% means that the company is not making an underwriting profit. For instance, an insurer with a 101% combined ratio means that it’s paying out 1% more money in claims and other expenses/losses/dividends than it is making from its income – in this case, premiums. So 84% is good.

For 1Q23, the premium growth was good. 5% group-wide despite negative FX, with price increases, high retention of customers, and progress on key growth initiatives. Underwriting profit was up, and EBIT came in at nearly €360, over €1B as a run rate.

Sampo remains extremely conservative. The company has a solvency coverage of 208%, including the accrual of company dividends, and a financial leverage below 28%, net of annual capital returns.

Sampo is not yet done with its structural changes either. The latest set of news is that the BOD has proposed to separate Mandatum from group, through a partial demerger of the Sampo PLC.

What exactly would de-merging Mandatum mean?

Well, as I said – Sampo is a multi-line insurer. Demerging Mandatum, which is Health/Life, would make Sampo pure P&C.

This is an attractive change because the risk considerations for Life/health and P&C are somewhat different. Underlying provisioning considerations are far more impactful in Life/health, which you can see in both Unum (UNM) and similar companies, which saw their block considerations and provisioning change on the basis of new research/morbidity data results. This is somewhat different in P&C, which is more exposed to environmental disasters, say flooding, hurricanes, or other things.

The separation is logical – and it would work to enable higher and more stable returns as reinsuring for P&C, while not “simpler”, is different than Life/health.

Other than that, the results have been very solid. The company is seeing good momentum, with personal insurance premiums up 12% YoY, and growth in Commercial and SME by 7%. Retention is incredibly high across all business areas. Uk-based Hastings is unfortunately not doing as well, with rising prices causing churn, but above all, the loss-cost trends remain challenging, with first-quarter adverse effects due to weather-driving claims, and continued high weather-related claims inflation weighing on margins. This is really the problem for P&C – weather events can cause claim inflation. Neither area in insurance is completely safe – but it makes sense to separate P&C from Life/health and run them expertly as two different businesses, rather than trying to mingle the two.

The Nordics continue to be an absolute company stalwart area for Sampo. With over 140 bps combined ratio improvements, the area is slowly trending towards an 80% combined ratio, currently at 82.4% and premiums were up over 6%, leading to an underwriting profit of 10% for the year. Claims levels are at about the same level here as well.

At the right price, Sampo is one of the better insurers in Europe. I would not put it above a cheap Allianz (OTCPK:ALIZY), nor a cheap reinsurer like Munich Re (OTCPK:MURGY), or even a French company like AXA (OTCQX:AXAHY). But Sampo has its part – and out of the companies I mentioned here, I have been long, and remain long one way or another in all of them – though at very different levels than 1-2 years ago.

Sampo is a profitable business at about the 60-70th percentile in multi-line insurers. It generates high returns, though the latest few years have seen many strategic changes in its way of making money. This has caused the company to be volatile in terms of valuation, and I would say that gauging where they should be valued is anything but easy here.

So let me show you where I believe the company should be rated here.

Sampo – Plenty to like, but the valuation is high for what is on the table

So, the issue that I have with Sampo is simply the valuation. Sampo has traded essentially flat for going on 3 years now if we exclude the dividends, and about 6% annual RoR with dividends, thanks to some of the reorganizations and shifts that have been ongoing for that time. This is not particularly positive.

The company’s P/E is starting to normalize at what I view as being the current realistic EPS run rate for the next few years. However, the reorganization of Mandatum is another component that needs to be taken into consideration. Any company in such a shift should not be premiumized, but a premium is what Sampo currently has.

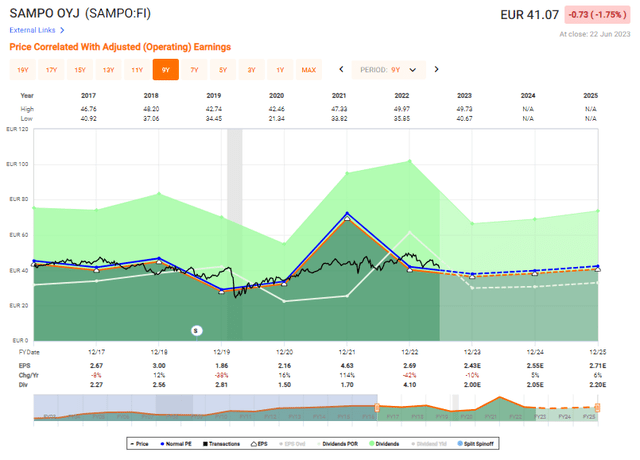

F.A.S.T graphs Sampo (F.A.S.T Graphs)

Any premium for Sampo here assumes growth – which might come, but also based on the Mandatum separation is not as clear going forward as it might once have been. The FactSet estimates are around 4-6% per year after 2023E, but this based on a 15x P/E- which is actually high for an insurer, gives us an annualized RoR of less than 4% with dividends based on a current normalized valuation of 16x.

So based on sector comps, based on historical valuations, and based on projected earnings, the company is currently expensive. That usually seals the deal for me – I don’t argue with math when I believe it shows me a clear implication and I don’t engage in what I would view as being too exuberant – or being too negative for that matter.

It becomes a matter of price. At under €38/share, this company’s upside even on a conservative 14-15x P/E is above 7% annually – that’s when I would start to become interested in the company again, doubly so for the resilience of its home markets.

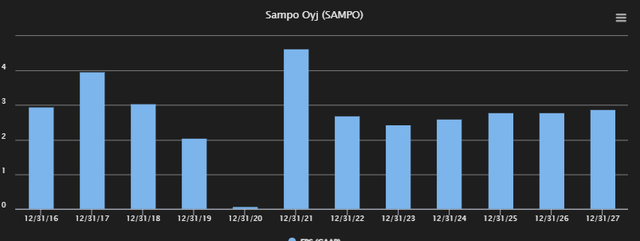

Here are the current EPS forecasts for Sampo.

Sampo Forecasts (TIKR.com)

I think you’d agree that these, beyond 2024-2025 do not look all that exciting at 16-17x P/E. If we’re talking 12-13x P/E, that’s a different story – then we get reversal potential. But at this valuation, it’s all about the potential growth the company can bring to the table that’s above the average.

And I do not believe that Sampo will be able to do that.

S&P Global forecasts would disagree with my assertion – which is fine. They’ve disagreed since I sold my shares at €45-€46 and didn’t look back. 15 analysts follow the company, and not a single analyst has a target that’s below €42/share, with the high-range target at an insane €58/share – I’d love to see those calculations upon which they are based.

Despite that, only 5 out of those 15 analysts are actually willing to give the company a “BUY”, despite the average PT being €49.15 next to a current price of €41.07/share.

This shows you the degree of conviction, despite the share price target, that these people have for the company – which is unfortunately very little.

I believe this further confirms my thesis – Sampo is simply too expensive here. I want to see where the de-merger goes, and I want to see the actual increases in earnings this and next year, to see if the company may warrant a higher premium.

For now, there are so many great insurers on sale, that I’m happy to take my money and go elsewhere for what I view as a safer, and better potential profit.

Here is my 2023 thesis on Sampo as it stands today.

Thesis

- Sampo is one of the better insurance companies in all of Europe. Together with Allianz, Munich Re, and AXA, I consider them the 4 prime investments in multi-line and reinsurance. Whenever one of them is cheap, that is a time to “BUY” the company for me.

- Sampo, at this particular time, is not a cheap company per se. Trading at 16x P/E, both on a European and International comparison, it’s an expensive insurance company for what it offers, despite its superb management and A-rated credit safety as well as very low leverage and over €20B worth of market cap.

- I would currently view Sampo as a “HOLD” here. Once the company hits below €38/share, I would consider it a “BUY” again.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Because it is neither cheap nor has a solid upside potential, I view this as not being an interesting or valid investment at this time based on my goals. I give the company a “HOLD”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here