Co-authored with PendragonY

In recent years, Electric Vehicles (‘EVs’) have become more popular and common. While Tesla (TSLA) is the most well-known of the brands, there are plenty of choices of vehicles. The major automakers are getting serious about producing such vehicles, and states like California and even the Federal Government are pushing regulations to get more EVs into the market. In Europe and several countries across the globe, the trend is going even faster.

While EVs are viewed as a clean source of energy, many forget that these EVs need conventional energy to charge. Most of this energy comes from traditional power plants, including natural gas, coal, or other types of carbon fuels. With the exponential growth of EVs, and just to keep up with population growth and increased living standards, the world will need to produce more electricity. If electric vehicles were to completely replace gasoline-powered vehicles, that would require roughly an additional 1 trillion kWh of electric supply on an annual basis. That amounts to nearly one-quarter of the current total electricity consumption! This will most certainly require new electric transmission lines from the new electric plants, no matter how they generate electricity.

With the green revolution in full swing, most countries are opting to generate electricity from Natural Gas plants, which is currently the “greener” source of energy. Today, even with solar and wind energy, natural gas remains the “cleaner” energy source available. It is projected that it will remain so for the next decade at least. Natural gas plants are easy to build and can come online quickly to meet both spikes in demand and falling supply during night-time and low wind days.

Furthermore, the Green Revolution is going very strong in Europe. The embargo on Russian gas has increased the demand for LNG from the United States. This means that U.S. natural gas producers, as well as companies that transport and store natural gas, are set to be big winners.

Today, we look at two great midstream closed-end funds (‘CEFs’) that invest in the largest and most profitable companies in the sector.

These midstream companies transport oil and natural gas through their pipelines and offer storage facilities for local consumption or overseas shipments. These midstream companies are set to be some of the biggest energy companies, and today is a great time to invest in this sector.

Another big advantage of midstream companies is that they have very high entry barriers, especially for existing pipelines. It is very hard to get new licenses for pipelines due to environmental regulations, and such pipelines are very expensive to build. Therefore current pipelines and storage facilities have an inherent advantage.

Investing in Midstream CEFs

Investing in midstream CEFs carries many advantages:

- Immediate diversification in the sector.

- Active management, with exposure to the best-run midstream companies.

- Investors do not receive K-1 tax forms. This is important because most of the largest midstream companies are set up as partnerships and issue K-1 tax forms at year-end. Having no K-1s results in less tax complications.

Let’s look at the 2 CEFs, both managed by First Trust.

Pick #1: FEN – Yield 9.4%

First Trust Energy Income and Growth Fund (NYSE:FEN) currently pays a distribution of $0.30 per share a quarter or $1.20 a year. At the current share price, this produces a yield of over 9%! Like many other CEFs, FEN reduced its distributions during the COVID crisis. Still, most of their holdings have increased their distributions since, so we fully expect that FEN increases its distribution again. The companies that increased their dividends and distributions include Enterprise Products Partners (EPD), Energy Transfer (ET), Hess Midstream (HESM), Plains All American Pipeline (PAA), Kinder Morgan (KMI), ONEOK (OKE), DTM, MPLX (MPLX), The Williams Companies (WMB), and Cheniere Energy (CQP), among others. These great midstream companies are some of the holdings of FEN.

While the distribution is mostly Return on Capital (‘ROC’), Master Limited Partnerships (‘MLPs’) distributions are the main reason for this. If we look closer, the Net Asset Value (‘NAV’) of FEN is up an average of 4.5% for each of the last three years. Clearly, the ROC isn’t destructive, and this is a big winning fund.

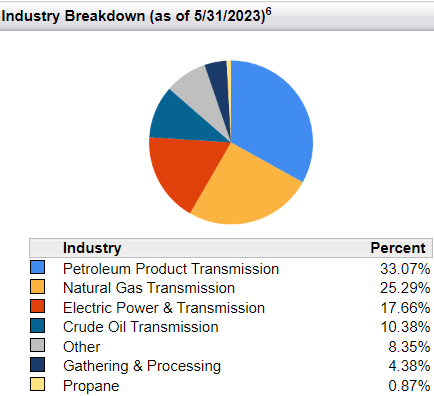

Most of FEN’s portfolio is invested in energy transmission, spread between petroleum products, natural gas, electricity, and crude oil. That diversity should allow it to take advantage of opportunities in both the short and long term (both fossil fuels and more green production methods). Source

First Trust Portfolios

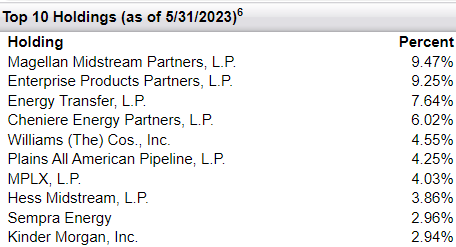

FEN’s top 10 holdings are filled with fairly familiar names. Enterprise Products is currently in the HDO portfolio. Energy Transfer and Magellan have both been in the HDO model portfolio in the past; Magellan is being bought by ONEOK. Cheniere is well known for its LNG processing facilities.

First Trust Portfolios

Pick #2: FEI – Yield 8%

First Trust MLP and Energy Income Fund (NYSE:FEI) pays a monthly distribution of 5 cents. At the current price, this produces a yield of 8%. Just like FEN, FEI reduced its distribution in response to COVID and has not yet increased it, despite the fact that many of its holdings did. Source

First Trust Portfolios

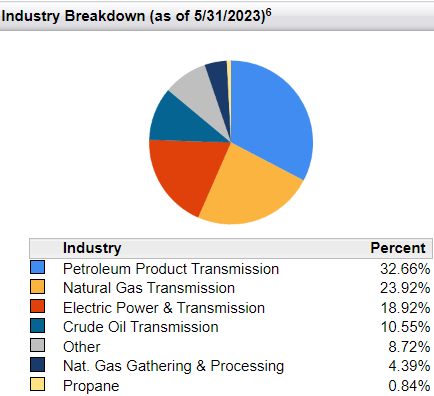

Looking at the fact sheet for FEI, we can see it has a similar industry breakdown as FEN. While the percentages are a bit different, FEI also has coverage across all energy transmission types.

First Trust Portfolios

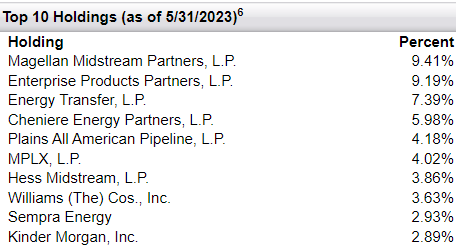

Looking at the Top 10 holdings, the list is very similar to what FEN holds.

What is the Difference Between FEN and FEI?

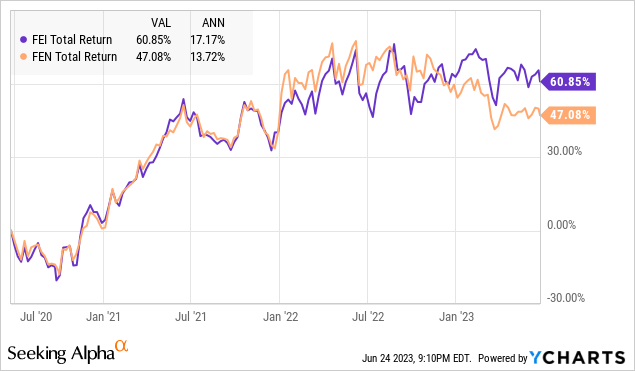

CEFs (unlike ETFs) are actively managed funds. The managers use their judgement to buy the dips where they see fit or sell stock to reduce risk. This is clearly why the vast majority of CEFs beat their ETF counterparts. For example, both FEN and FEI have higher total returns than the midstream ETF Alerian MLP (AMLP).

While there are slight differences in the holdings of FEN and FEI, their management strategy is different. One focuses on higher income, while the other focuses on total return.

Why Buy Energy Now?

So why is it now a good time to buy energy investments, particularly FEN and FEI?

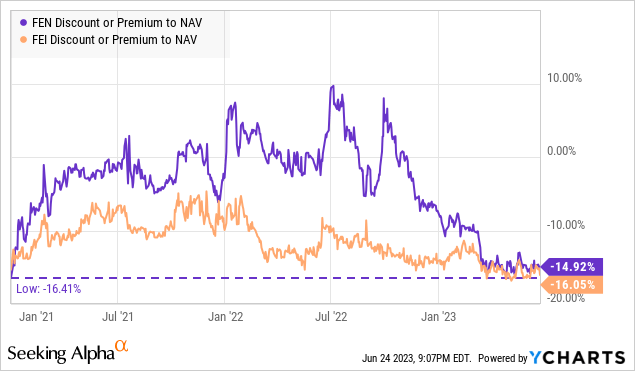

First, let’s look at the price of FEN and FEI shares compared to the net value of the assets that back each share. Looking at the graph below, we can see that currently, the share price is near its largest discount to NAV since the end of COVID. While a discount to NAV doesn’t mean that the price is a good one, a larger-than-average discount is an indication that the price offers a great bargain!

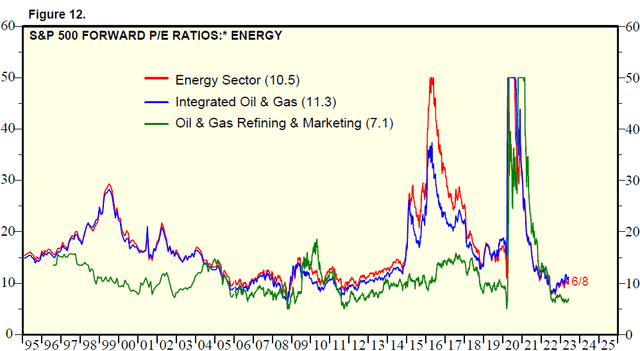

Looking at the P/E for the energy sector as a whole, we can see that it is currently near the levels seen during recessions. That makes for a good place to be buying energy stocks.

Yardeni

During the COVID crash, AMLP had to cut the dividend from $0.9750 to $0.68 a share. It has now increased the dividend for the most recent quarter to $0.86. As AMLP must pay out the dividends it receives, that means that FEN and FEI are also seeing increased dividends paid to them. This will eventually require the funds to increase the distribution they pay to their shareholders. In addition to the big discount that both FEN and FEI are currently offering, this makes now a very good time to buy shares before the funds announce such an increase.

Conclusion

The Green Revolution in energy is causing a boom in the natural gas sector because natural gas is less polluting than other fossil fuels. Most green energy sources need a reliable backup to provide base power, and natural gas is currently the “greener” energy of choice and is expected to be so for the next decade at least. We previously covered how the Green Revolution is boosting the demand for natural gas in this article.

FEN and FEI are both good picks in the energy sector; which one should you pick? Well, that depends on your priorities.

With FEN having a yield of 9.4% and an average annual total return of 13.7% over the last three years, it is a better pick if your priority places current income ahead of total return. With a yield of 8% and an average annual total return of 17.2%, FEI is the better choice if you value total return over current income. As for myself, I have been buying the dip in both for income and total return!

Read the full article here