Investment Thesis

I wrote an article about MAG Silver (NYSE:MAG) recently, where I highlighted the quality asset Juanicipio, but also my dissatisfaction with the bought deals earlier in the year. I wanted to see even more downside from that point to consider going long MAG Silver.

So, given the recent decline, which has led to an even more attractive valuation combined with commercial production at Juanicipio being declared ahead of schedule, I have recently added MAG Silver to my portfolio.

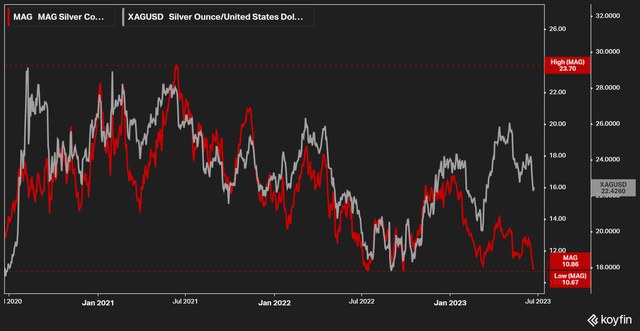

The stock price is very out of favor at the moment, trading close to the lows of the 3-year trading range, while silver has held up reasonably well lately.

Figure 1 – Source: Koyfin

This article will be about the valuation of MAG Silver and Juanicipio, as that is where the company gets most of its value from.

Recent Developments

Since my last article on MAG was published, the company has reported a solid Q1-23 result, which provided indications that Juanicipio was ramping up well.

The company did a few weeks ago confirm that by declaring commercial production as of the 1st of June 2023, where the Juanicipio mill has been operating at approximately 85% of its design capacity. So, we are now likely only a quarter or two away from consistently running at the design capacity of 4,000 tonnes per day.

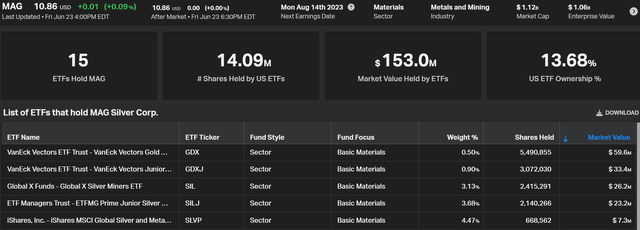

Following the announcement of commercial production, the stock was also added to the NYSE Arca Gold BUGS Index in June, which the large (GDX) ETF is tracking. The purchase of more than 5M shares by the GDX did not have the effect one would have expected, even if the stock did see a short-lived bounce on the announcement. The net effect from all the ETFs looks to have been less than 5M shares, as MAG’s weight in the (SILJ) seems to have decreased substantially during June as well.

Figure 2 – Source: Koyfin

Valuation Assumptions

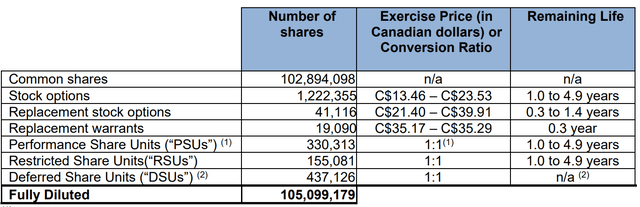

When it comes to the valuation, I have relied on the shares and share units as of Q1-23, but only included the stock options which are still in-the-money at this depressed stock price. We then have 104.0M shares. MAG has no debt and $55M in cash as of Q1-23, which gives us a market cap of $1,117M, and an enterprise value of $1,063M.

Figure 3 – Source: Q1-23 MDA Figure 4 – Source: Q1-23 FS

There is still quite a lot of uncertainty with regards the production volume and costs going forward. The preliminary economic assessment (“PEA”) that MAG Silver produced, is from 2017, so it is to a large degree obsolete at this point.

My estimates are partly based on that PEA, but also communication from Fresnillo (OTCPK:FNLPF) with regards to Juanicipio, where I will assume Juanicipio will produce 13M silver equivalent ounces per year (MAG’s 44% ownership share) and the all-in sustaining cost (“AISC”) is roughly estimated to $11/oz. Please note that the PEA estimated AISC to $5/oz, but that was a long time ago.

I have also assumed another $12M in general & administrative expenses and $15M in non-sustaining CAPEX per year, that are assumed to not be included in the AISC figure. The spot price of silver is about $22.4/oz at the moment, but I have relied on a silver price of $23/oz, which is what the future price is for silver by the time Juanicipio is running at nameplate capacity.

Conclusion

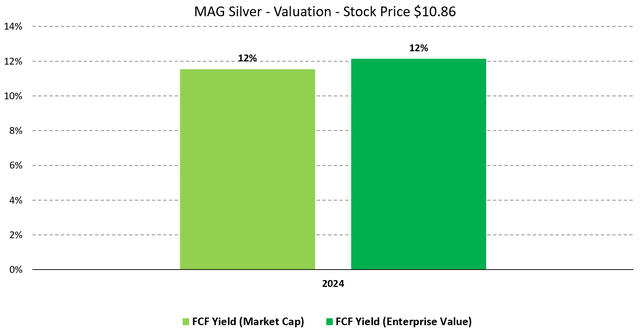

Figure 5 – Source: My Estimates

As the chart above highlights, MAG Silver is currently trading with a free cash flow yield of 12% for 2024, which is no doubt a very attractive level. There is as I earlier highlighted some uncertainty with regards to production and costs, but even if I have overestimated the capabilities of Juanicipio, the valuation would likely still be very attractive at this point. It is rare to see precious metals mining companies trade with such a high free cash flow yield.

Part of the reason for the attractive valuation is likely concerns about mining in Mexico lately. There is no doubt the risk has increased over the last few years, but I would argue the risk is more pronounced for exploration and development companies than a producer like MAG Silver.

Also, Juanicipio has Fresnillo, which is the world’s largest silver producer and a local company, as the operator, and Juanicipio is one of the lowest cost silver mines around. I do think Fresnillo should be able to navigate the Mexican mining regulation successfully.

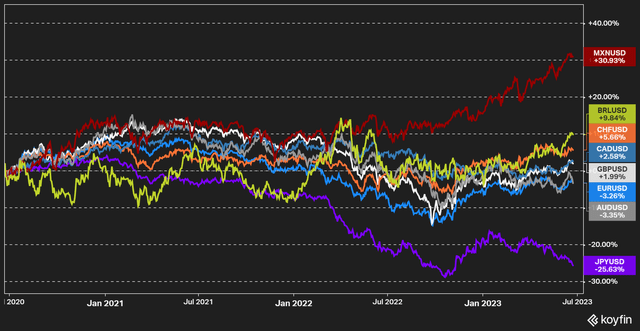

The strong Mexican Peso is likely another headwind for mining companies in the country, even if I am less concerned about this longer term, as I suspect it will either mean revert over time or partly be offset by a lower inflation rate compared to other countries.

Figure 6 – Source: Koyfin

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here