Gevo (NASDAQ:GEVO) stands at a critical juncture as it grapples with financial hurdles yet unveils potential avenues for growth and solidifies its position as an industry pioneer. Despite setbacks in stock performance and construction delays, Gevo’s strategic partnerships, secured revenue streams, and innovative technologies present a compelling case for long-term investment in a sustainable future.

What is happening with Gevo?

During the first quarter of fiscal 2023, Gevo delivered revenue of $4.1 million, or $3.8 million more than the Q1 of 2022. The difference primarily came from the renewable natural gas facility (or RNG), which is now fully operational, and the sale of some isooctane. However, loss from operations has widened to $20.9 million, compared to $16 million in Q1 of 2022.

This resulted in a net loss per share of $0.07. The company has burned through $30 million, as the cash and cash equivalents have dropped from $482.8 million at the end of Q4 2022 to $452.9 million this quarter.

However, the company shared two pieces of information with its investors, which may bring more light to its potential future income sources and what could change investors’ sentiment toward the stock.

What did you miss?

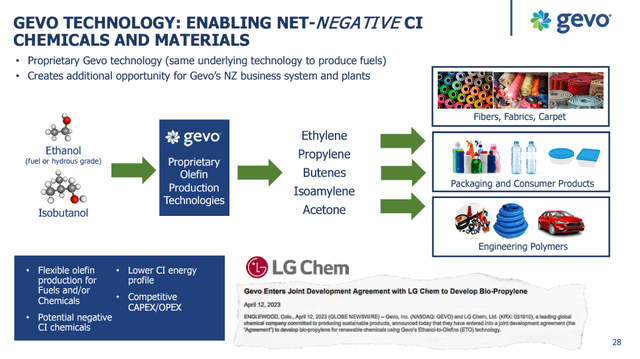

The first piece of information was that on the 10th of April 2023, Gevo and LG Chem, Ltd. entered into a joint development agreement to develop bio-propylene using Gevo’s Ethanol-to-Olefins (“ETO”) technology.

Hydrocarbons to Plastic (Gevo June Presentation)

Gevo has several technologies to convert alcohol to hydrocarbons, primarily for producing SAF, diesel, or gasoline. However, these technologies can also create materials such as polymers and plastics. Besides, this is where a massive opportunity for Gevo can arise.

According to the European Bioplastics website, global bioplastic production is expected to increase from around 2.2 million tonnes in 2022 to 6.3 million in 2027. Despite impressive growth, global plastic production is more than 390 million tonnes, giving bioplastics a market share of less than 1% and much room to grow.

Once the technology is developed, many products based on fossil fuel, such as the plastic interior in cars, flooring, etc., can be replaced and produced with bio-based raw materials.

The second piece of information was that on the 5th of May 2023, Gevo entered into a Technology Access Agreement with Phillips 66 (PSX) and Archer-Daniels-Midland(ADM), which has the potential to provide $125 million in a mix of milestones and royalty payments given certain conditions are met. This demonstrates that Gevo’s technology is well-developed and potentially ready for commercialization.

However, none of them seem more important right now to investors than the construction of the Net-Zero 1 plant, which is the key to the future success of Gevo as a company and the main reason investors are purchasing the stock.

What is happening with Net-Zero 1?

In the first quarter report for fiscal 2023, the management addressed the need for multiple Net-Zero production facilities to satisfy the existing supply agreements. According to the Q3 report of fiscal 2022, the company still has more than 375 million gallons per year (“MGPY”) of SAF supply agreements, which are expected to deliver $2.3 billion in revenue and $1.5 billion of EBITDA annually. With each NZ1 having the capacity to produce about 55 MGPY, this equals as many as seven facilities needed to be built.

As a result, they have shifted their focus towards maximizing the modularization of the production plants, which can be made in one place and transported to the final production site. However, this will take additional time and some rigorous up-front engineering and design, but it will eventually pay back in the long run.

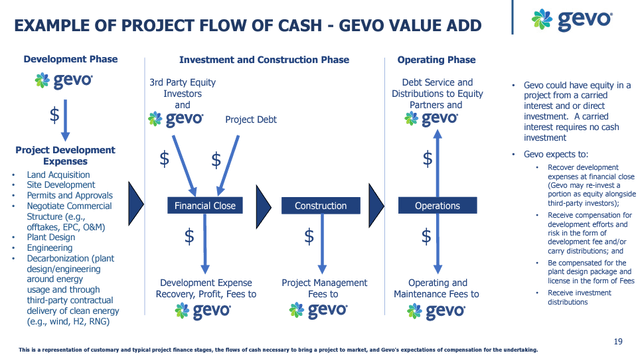

Meanwhile, Net-Zero 1 is approaching maturity, but Gevo has two major obstacles. The firm intends to finance most of the construction, but will also require third-party equity and debt.

Gevo’s Project Flow of Cash (June 2023 Presentation)

On one side, during the Q1 press conference, management confirmed strong interest from several potential equity investors, which largely solved the problem. Contrarily, debt financing will require more detailed work and will likely hold the project back.

Due to rising interest rates, management has decided that the best decision would be to apply to the U.S. Department of Energy (“DOE”). If approved, the firm will receive lending from the Federal Financing Bank at the most attractive debt terms possible. However, the whole process has its downsides too.

The DOE-guaranteed loan may be the most attractive debt option for Gevo, but the application processing can easily carry into 2024. To make matters worse, the construction of Net-Zero 1 is expected to start 24 to 30 months after the financing is closed, pushing the project firmly into 2026 and potentially early 2027 if anything else goes wrong. The news may come as a cold shower to investors, as this is not the first time the project has been pushed in time.

In the first article I wrote about Gevo in early 2021, management was expecting the construction of Net-Zero 1 to be completed by the end of 2023. However, in the latest article, I wrote about Gevo on the 20th of December 2022, the Net-Zero 1 project was expected to be finished in 2025.

Looking at the stock price at this point, the amount of frustration accumulated over the years becomes obvious.

Is Gevo Still a Buy?

Two years ago, the company was seen as an advanced biofuel company that would revolutionize the energy business, with substantial growth perspectives ahead.

Gevo’s Share Price (Seeking Alpha)

On the 15th of February 2021, the firm was at its peak, trading at $14 a share, with a market capitalization of $2.82 billion. The renewable industry frenzy made the stock resemble a tech company from the late ’90s. A business with shy of a half million dollars in revenue for 2021 but with a hefty P/B ratio north of 12. Fast forward two years and four months, and the stock is far from its glory days.

Gevo is trading at $1.33, with a market capitalization of $308 million. The stock has been on a downward trend for quite some time, but despite the adversities, the company still offers a great investment opportunity.

Unlike more than two years ago, the firm trades at a P/B ratio of 0.51. The firm is well funded, with $452.9 million in cash and cash equivalents. The business has more money than the whole market capitalization of the company.

With that amount of fuel supply secured, the company has only one mission: to start as many net-zero projects as possible.

Construction of the NZ1 project is still on, despite the recent challenges. Management is even actively exploring sites for NZ2.

Although cash is scarce at this point and the management is very frugal on how to spend it, the CEO has highlighted that they may even explore the so-called “carry in” projects where they do not participate with cash but with technology, in exchange for equity or royalties, or a mix of both.

In addition, the potential expansion in a rapidly growing market, such as bio-plastic with the LG Chem, Ltd. agreement, could set the company up for an even bigger future than what investors have bargained for.

But bear in mind the risks.

Risks

Cash is the one thing the company does not have in abundance. The money is insufficient to finance all the projects, costing around $850 million each. The high-interest rate environment is not helping, either.

Furthermore, issuing more shares when the P/B ratio of the company is just 0.51 is not a good deal. During fiscal 2022, the company used $52.6 million for running the facilities, but with $452.9 million in cash, the balance sheet remains healthy.

As mentioned, this is not the first time the projected completion date for NZ1 has been pushed further back, and there are no guarantees that DOE will approve financing for the project.

Conclusion

Gevo’s financial performance has been underwhelming, but the company continues to present potential growth opportunities. While constructing the Net-Zero 1 plant remains a critical concern, Gevo’s strategic partnerships, secured SAF supply agreements, and exploration of bio-plastics markets promise an excellent future for the company.

Read the full article here