Introduction

BW LPG (OTCPK:BWLLF) (OTCPK:BWLLY) posted excellent Q1 results which wasn’t a surprise as I clearly was expecting that when I wrote the previous article on the company. Q1 definitely didn’t disappoint, but the second quarter will likely also be pretty strong as charter rates remain robust. While we should expect the Q2 results to be ‘worse’ than the Q1 results, BW LPG’s performance remains stronger for a longer period than I had initially expected despite a few dozen new VLGC vessels hitting the waters this year. And BW LPG isn’t alone. In a recent article, I explained how peer and competitor Avance Gas (OTCPK:AVACF) is also still performing very well.

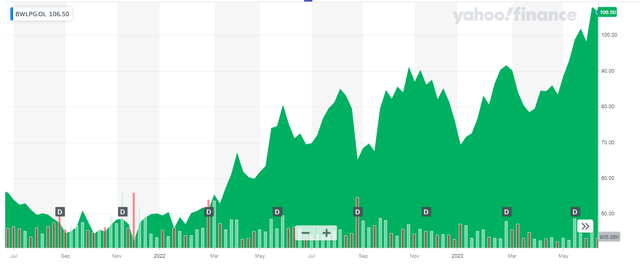

Yahoo Finance

BW LPG has its main listing on the Oslo Stock Exchange where it’s trading with BWLPG as its ticker symbol. The average daily volume in Norway is currently approximately 250,000 shares and this makes Oslo by far the most liquid exchange to trade in the company’s shares. BW LPG is currently trading at 107 NOK per share which translates into $10 based on the current exchange rate (10.7 NOK per 1 USD).

You can find all relevant financial documentation I will refer to here.

Stronger than expected charter rates boosted the Q1 results

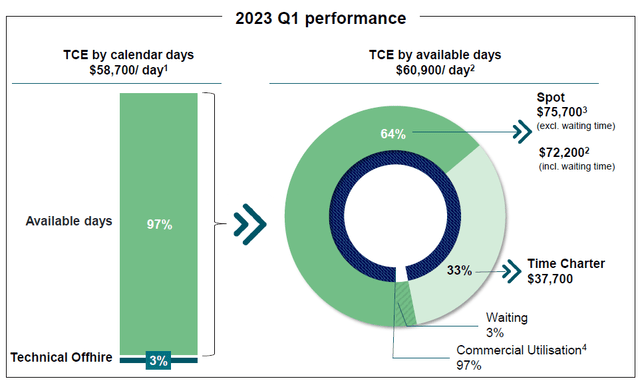

As explained in the introduction, the charter rates remained strong in the first quarter of the current financial year. Competitor Avance Gas was able to secure an average daily charter rate of in excess of $58,000 and BW LPG was able to post a very similar charter rate. During the first quarter, BW LPG recorded an average freight rate of US$58,700 per calendar day.

BW LPG Investor Relations

As you can see above, about 1/3rd of the available days were locked in at a fixed rate time charter with an average revenue of $37,700 per day. BW LPG took advantage of the strong spot market with charter rates of just over $75,000/day and even if you’d include the waiting time, the average daily rate still exceeded $72,000/day. This resulted in an average time charter equivalent rate of $60,000 per available day and just under $59,000 per calendar day (as about 3% of the calendar days were used as waiting time).

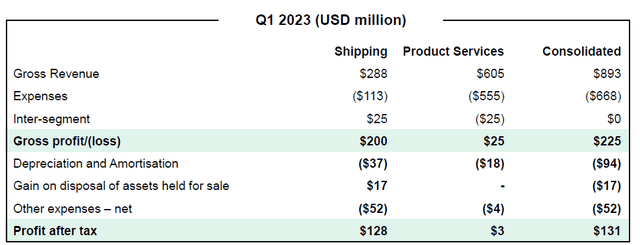

The total gross profit in the first quarter came in at $225M (the official revenue is approximately $900M but this includes the revenue generated from the ‘product services’ division, where the margins are relatively thin). As you can see below, the product services segment accounts for almost 70% of the consolidated revenue but represents just over 10% of the gross profit.

BW LPG Investor Relations

Fortunately BW LPG’s other operating expenses are relatively low: the operating expenses are just over $22M and the strong charter rates in combination with the very reasonable operating expenses resulted in a reported EBITDA of $176.1M. That’s almost double the EBITDA the company generated in the first quarter of 2022.

The pre-tax income more than doubled as the company also reported a $16.6M gain on vessels held for sale (versus a total of less than $14M in gain on disposals in the first quarter of last year). The net income during the first quarter was $130.7M which represents an EPS of $0.95 per share.

BW LPG Investor Relations

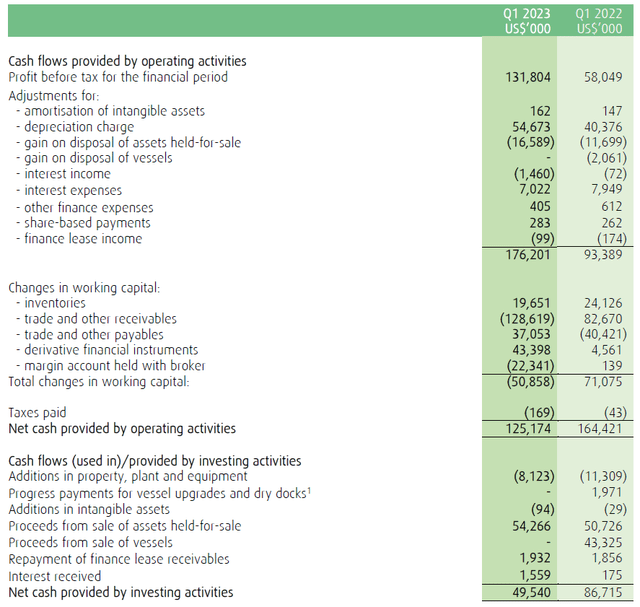

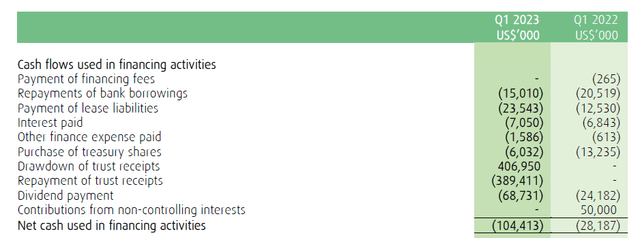

It shouldn’t be a surprise to see the cash flow result was equally strong. As you can see below, the reported operating cash flow was approximately $176M, and this obviously excludes the impact of the gain on the two vessels that were sold. We should add the $1.9M in received lease payments and the $1.6M in interest received but we should subsequently obviously also deduct the $23.5M in lease payments and the $8.5M in interest payments and other finance payments.

BW LPG Investor Relations

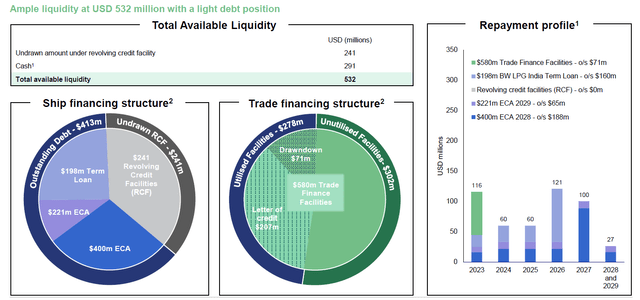

On an adjusted basis, the operating cash flow was approximately $147.5M before changes in the working capital position. The total capex was just over $8M resulting in a net free cash flow of just under $140M. That’s of course thanks to the lack of investments in newbuild vessels during the first quarter and thanks to the robust balance sheet with access to in excess of half a billion dollars in available liquidity.

BW LPG Investor Relations

Very strong results in the first quarter but just like we saw at Avance Gas, the company will likely have to take a step back in the current quarter. As per the company’s most recent update, about 90% of the available fleet days have been fixed at an average rate of approximately $50,000 per day. So while the financial results will likely (have to) take a step back, BW LPG should still be strongly profitable and strongly free cash flowing.

Subsequent to the end of the first quarter, BW LPG also completed the sale of two vessels. The BW Odin and BW Austria were sold at a $26M profit compared to their respective book values. And the total sales proceeds of in excess of $100M are helpful to keep the balance sheet in good shape and further increase the access to liquidity.

Investment thesis

I have no position in BW LPG (nor in Avance Gas, for that matter), but I am pleasantly surprised to see BW LPG’s operating and financial performance is still very strong. The share price has more than doubled since my very first article was published, less than 2 years ago. And as BW LPG has continued to pay outsized dividends (the shareholders are benefiting from the very strong performance) the total return is approximately 150% (in USD) during those 22 months.

Perhaps my fear of the impact of the fleet expansion is/was unfounded and we will find out in the next few months and quarters if I perhaps was too conservative. I currently have no position in BW LPG but I am keeping track of the company’s performance. With recent VLGC charter rates surging to $3M per month ($100,000/day), BW LPG may actually start the third quarter on a much stronger note than I had anticipated.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here