Synovus Financial Corp. (NYSE:SNV) operates as a bank holding company for Synovus Bank; it was founded back in 1888 and is headquartered in Columbus, Georgia.

TradingView

Despite a slight recovery in recent weeks, the effects of the banking crises triggered by SVB’s bankruptcy are still being reflected in the price of Synovus Financial, which is definitely far from its all-time high. However, such a decline has revealed opportunities that were not there before, including a dividend yield of 4.80%.

As I will show you throughout this article, at this price Synovus Financial may be a good option, especially for those looking for high and sustainable dividends. But it is probably not for me.

Deposits Quality

In my opinion, deposits quality is the first aspect to consider when analyzing a bank, as it is the raw material on which the entire financial structure is based. I will now show you how Synovus Financial is positioned in this respect.

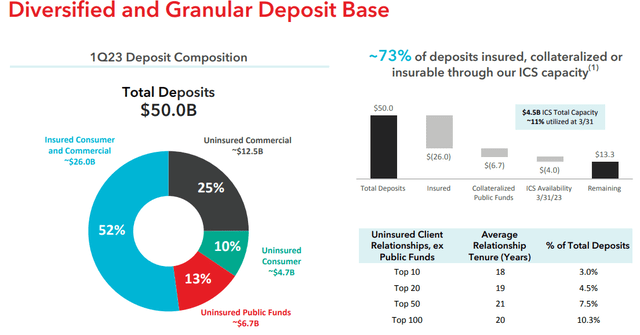

Synovus Financial Corp Q1 2023

First of all, about 73 percent of deposits are insured, collateralized or insurable. The deposit base is both diversified and not very concentrated, which is positive. In fact, the top 100 uninsured customers account for just over 10 percent of total deposits.

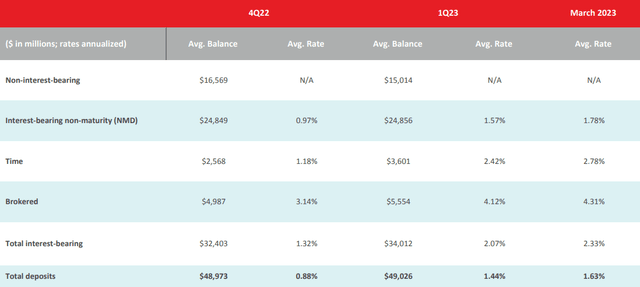

Synovus Financial Corp Q1 2023

Probably the least positive aspect concerns the cost of deposits, in fact in March 2023 the average interest paid was 1.63% when only a few months earlier it was 0.88%. In addition, it is also important to mention that non-interest-bearing deposits have decreased by $1.55 billion compared to Q4 2022, which is definitely a factor to consider. Synovus Financial has had to find other ways to replace these free funds, including time deposits and brokered CDs, both of which are significantly more expensive. Combining both deposits and loans, the overall average cost amounted to 2.33 percent in March, 101 basis points more than in Q4 2022.

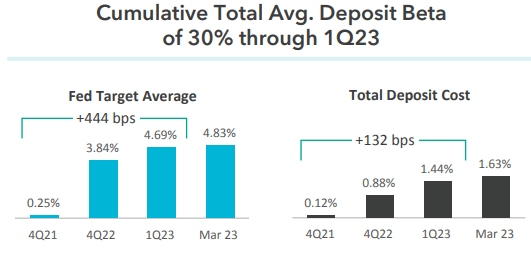

Synovus Financial Corp Q1 2023

Comparing the increase in the Fed Funds Rate and the cost of deposits, Synovus Financial was able to achieve a deposit beta of 30 percent, which is a decent result but certainly not optimal. According to the latest Fed estimates, we can expect at least two more 25 basis point hikes by the end of the year, which could mean that the deposit beta could continue to rise.

Over the past month I have been analyzing many regional banks, and Synovus Financial shows average results in terms of deposit costs; nothing worrisome but nothing exciting either. For example, there are banks like Banner that have not been affected as much by the interest rate increase; in fact, it still exhibits a deposit cost of less than 0.30 percent.

Earning Asset Composition and Net Interest Margin

The deposits cost is not the only factor that adjusts for interest rates; there is also the yield on assets.

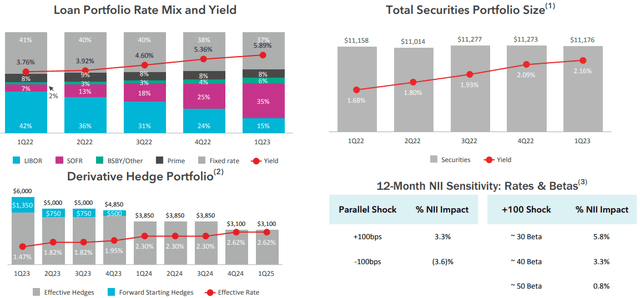

Synovus Financial Corp Q1 2023

The loan portfolio rate gradually increased each quarter and reached 5.89 percent, which makes the increase in the cost of liabilities less bitter. At the same time, the securities portfolio also presented a growth in yield, although its size remained almost unchanged from Q1 2022.

Although not featured in this slide, with regard to the securities portfolio it should be pointed out that, as of Q1 2023, it is registering an unrealized loss of as much as $1.28 billion, a significantly large figure. In fact, it represents about 27 percent of equity. Synovus Financial, as well as many other banks, made major purchases of fixed-rate securities before the Fed aggressively raised interest rates, and this led to a large unrealized loss, especially for high duration securities. If the Fed were to cut interest rates a lot, the problem would recede: the point is that before 2024 it is unlikely to happen. So, as long as the macroeconomic condition remains the same, we have to consider this large unrealized loss in Synovus Financial’s balance sheet. The latter, of course also weighs on the Book Value per share, a key metric to which each bank’s price per share follows.

Staying with interest rate risk, in the last slide we can see the expected change in net interest income (NII) as interest rates change. A 100-basis point increase would have a +3.30 percent impact on NII; a 100-basis point decrease would have a – 3.60 percent impact. In short, the bank is positioned toward a further increase in interest rates. Thus, should the Fed reduce them, on the one hand the unrealized loss of the securities portfolio would be reduced, but on the other hand the NII would suffer.

Synovus Financial Corp Q1 2023

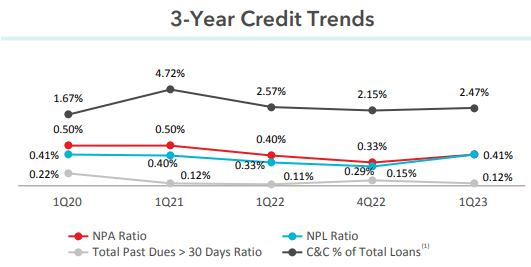

Returning briefly to the loan portfolio, we can see that at the moment the main indices used for credit risk are all in good standing. So, despite Synovus Financial’s significant exposure to the CRE segment, for the time being, there is no reason to doubt the creditworthiness of its borrowers.

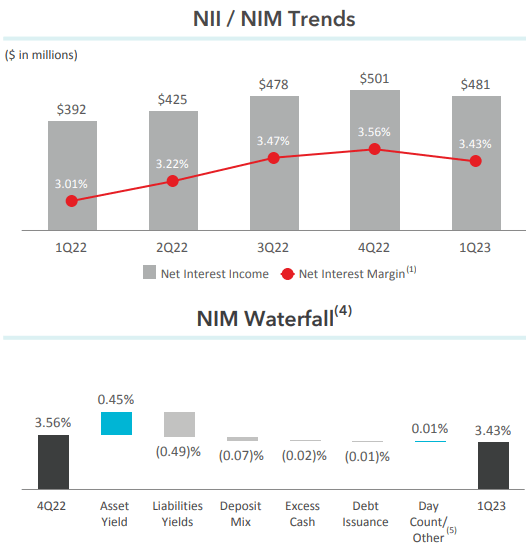

In any case, although the yield on assets has improved, it has not been able to fully cover the increase in the cost of liabilities. In fact, the net interest margin decreased by 13 basis points compared to Q4 2022.

Synovus Financial Corp Q1 2023

Asset yield affected +0.45%, but it was not enough against – 0.49%. In addition, excess cash and deposit mix also did not help Synovus Financial; – 0.02% and – 0.07% respectively.

Dividend Analysis

As anticipated at the beginning of the article, the dividend yield of Synovus Financial seems attractive for those who prefer to invest in companies with a high dividend yield; in this case, we are talking about 4.80%. But is it sustainable?

Seeking Alpha

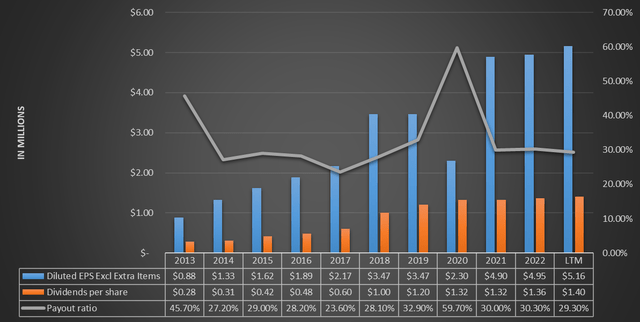

Comparing diluted EPS with dividend per share, it is evident that the former are significantly higher than the latter. In fact, the payout ratio is quite low, only 29.30 percent. So even if EPS slows down in the coming years due to the long-awaited recession, in my opinion, management will continue to issue a good dividend anyway. After all, Synovus Financial has a dividend yield of 4.80 percent with a payout ratio of 29.30 percent; if EPS dropped even 20-30 percent, the payout ratio would still be less than 50 percent.

In short, barring any sensational unforeseen events, I consider the dividend to be sustainable in the coming years.

Seeking Alpha

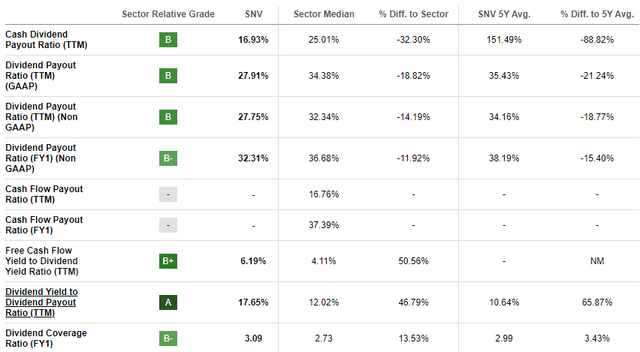

Finally, according to Seeking Alpha’s data on the dividend safety, Synovus Financial’s ratios are often better than its peers. In short, at least for the moment the situation is stable.

Valuation

To assess the fair value of Synovus Financial, I will use a weighted average among three valuation methods; the first will have a weight of 40% and will be based on book value, the second will have the same weight but will be based on EPS, and the third will be a dividend discount model with a weight of 20%. All data will be obtained from Seeking Alpha.

- The average price/book value over the last 5 years is 1.31x; multiplying this figure by the current book value per share of $28.98 results in a fair value of $37.96 per share.

- The average P/E for the past 5 years has been 10.82x; multiplying this figure by the expected EPS for 2023 of $4.73 (Street estimates), the fair value amounts to $51.17 per share.

- As for the dividend discount model, the inputs will be as follows:

- Annual Payout (FWD) of $1.52 per share.

- Annual return required from the investment 15%. We are talking about a small regional bank, and being a very risky investment, in my opinion a high return is required to take this risk.

- Dividend growth of 8% per year. Over the past 10 years the CAGR has been 17.79%, however I wanted to include a more conservative value. After all, the macroeconomic environment has definitely changed from 10 years ago.

The resulting fair value following these assumptions is $23.45 per share.

Summing it up, the first two methods show that Synovus Financial is undervalued, especially the one with earnings, while for the dividend discount model this bank is overvalued. In the last method, the required return definitely affected a lot, but I think it is unavoidable given the riskiness of the investment.

By making the weighted average of the three models according to the directions I mentioned earlier, the fair value of Synovus Financial is $40.34 per share, so the stock is undervalued.

Final Thoughts

Overall, Synovus Financial is a bank that has suffered from the rising cost of deposits and this has affected the net interest margin. Unrealized losses are another issue to monitor, but I remain optimistic because when the Fed reduces interest rates this loss will disappear. At the moment, the market is discounting these issues in the price of Synovus Financial, which is why it appears rather at a discount. So, the stock is undervalued, the dividend is high, but why don’t I invest in it?

The reason is that like Synovus Financial, many other regional banks are in a similar situation, which leads me to avoid investing in them. Rather than invest individually in all these banks with similar characteristics and problems, I prefer to buy an ETF. If I have to invest in a single bank, I want it to have peculiarities that are out of the ordinary. In this regard, I suggest you read my article on Banner Corporation, a semi-unknown bank that I believe may reflect the latter description.

Read the full article here