10x Genomics (NASDAQ:TXG) has been on my Compounding Healthcare “Bio Boom” speculative portfolio watch list since its IPO back in 2019. At that time, I was enthralled with their products, services, and R&D prowess. Like a lot of healthcare and biotech investors, I turned my attention to COVID-19 opportunities for the next few years, and TXG was nearly forgotten. Recently, I was running through my watch lists and I decided to revisit TXG, and possibly update my outlook. Well, a brief look at the company’s earnings and the ticker’s daily chart was all I needed to move TXG closer to the top of the watch list. After performing some analysis, I believe the company’s growth record and prospects outweigh the risks at this point.

I intend to provide some background on 10x and the company’s recent performance. Then, I will point out some leading downside risks that investors should consider when managing a TXG position. Finally, I lay out my strategy for initiating a position in TXG.

Background On 10x Genomics

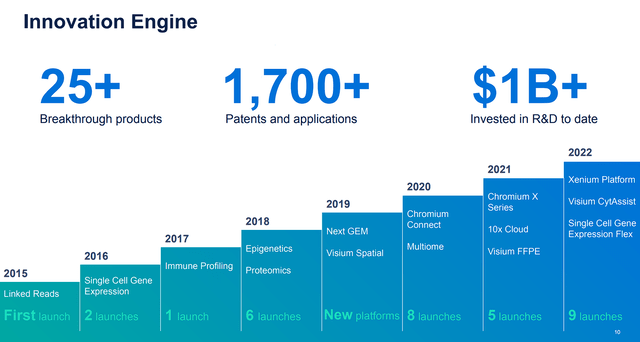

10x Genomics is a life sciences tech company developing state-of-the-art tools and products to be used in a variety of applications for customers around the world. Their business approach involves developing top-of-the-line products with a relentless effort in R&D to bolster their pipeline.

10x Genomics Innovation Efforts (10x Genomics)

Furthermore, the company has made a series of acquisitions over the years to expand their scope.

10x Genomics Acquisitions (10x Genomics)

Financials

10X Genomics reported $134.3M in revenue for Q1, up 17% from $114.5M from Q1 of 2022. OpEx came in at $150.4M for Q1, a 15% increase year-over-year. This led to an operating loss of $52M for the quarter, up from $41.7M in Q1 of 2022. However, the operating loss comprises $42.1M in stock-based compensation for the quarter versus only $26.0M in Q1 of 2022. Net loss equaled $50.7M for the first quarter of the year. The company’s gross margin was 73% in Q1, down from 78% in the same period in the prior year.

In terms of cash, the company finished Q1 with $418.3M in cash and cash equivalents and marketable securities. Make note that 10x has about $102.04M in total debt.

Portfolio and Pipeline

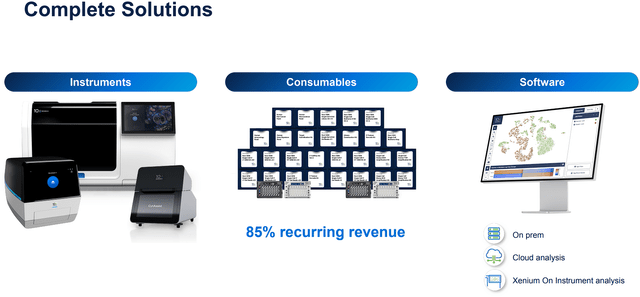

10x Genomics has a line of consumables for their chromium instruments, as well as associated software. The company’s collection of products and services provides them with recurring revenue and impressive margins. The company has developed a range of products for researchers to investigate biological systems at vital resolutions on immense scales. 10x’s offerings cover three primary segments: Instruments, Consumables, and Software.

10x Genomics Product Segments (10x Genomics)

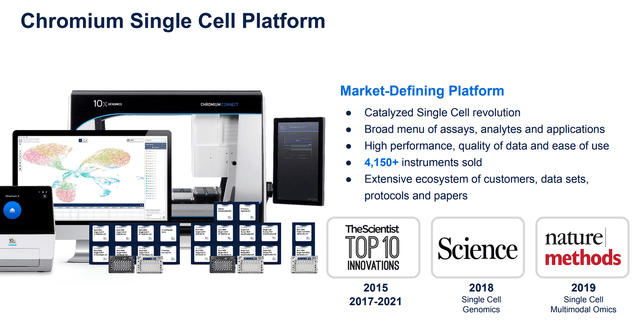

The company’s flagship platform is their Chromium Single-Cell Platform. Not only was this a huge break for the company’s business, but it was also a revolutionary platform for the industry with touted performance, scale, and versatility. The Chromium platform provides large-scale processes with high cell throughput, empowering the analysis capable of 1M cells per microfluidic chip, which boosts the likelihoods of detecting cells that are capable of causing a rare disease. Moreover, the platform reaches an extraordinary cell capture rate of about 65%, exceeding several challengers in bagging rare cells being extracted from samples. In addition, the Chromium platform diminishes the potential loss of cell data and needless sequencing. As a result, 10x has reported that over 4,150 units have been sold.

10x Genomics Chromium Single Cell Platform (10x Genomics)

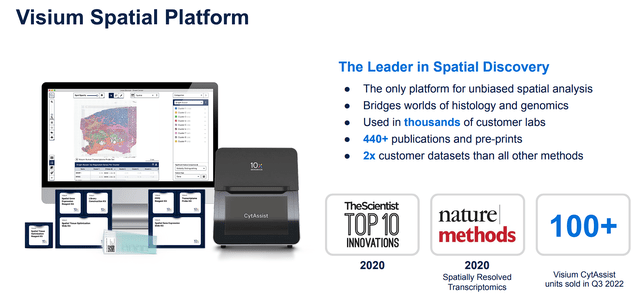

10x also has their Visium Spatial Platform used for spatial analysis with high-throughput subcellular mapping up to thousands of RNA targets on top of multiplexed protein on a tissue segment. The Visium platform examines the spatial positions of biological components in the interior tissues at high resolution. Spatial analysis is vital for comprehending tissue function in both healthy and diseased states. Visium can be used to discern cell components to help diagnose and determine a course for the treatment of a variety of diseases.

10x Genomics Visium Spatial Platform (10x Genomics)

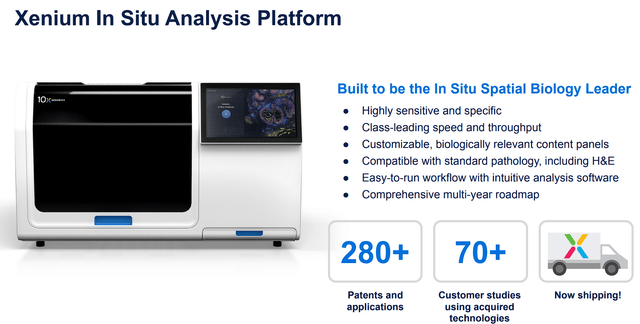

The company’s Xenium In Situ Analysis Platform which an incredibly sensitive and tunable product thanks to it utilizing a “padlock probe rolling circle amplification chemistry.” The Xenium platform empowers researchers to detect and categorize cells within their tissue environment “in situ”. In addition, the platform can identify and analyze RNA and protein molecules in situ. Additionally, the platform is capable of being fully automated without sacrificing sensitivity or throughput levels.

10x Genomics Xenium In Situ Analysis Platform (10x Genomics)

In addition, 10x has several software and applications, including cloud analysis and the Loupe Browser which is a potent visualization software. The company also has CRISPR screening, multiomic cytometry, and antigen mapping as applications. Lastly, 10x Genomics offers a variety of other instruments and technologies.

So, what are these instruments used for?

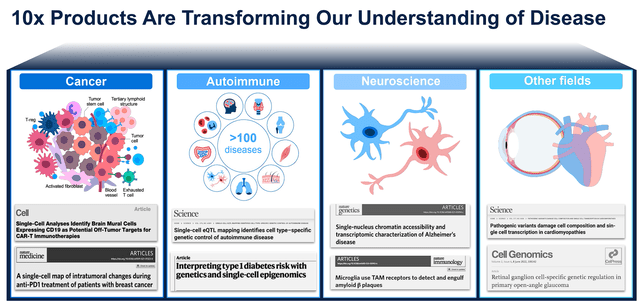

Well, the company’s instruments and technology allow them to perform single-cell analysis, which is a cherished means to cognize cellular activities and intricacy at a singular level. This method allows the study of heterogeneity between cell populations and thorough gene expression examination. Additionally, the single-cell analysis highlights cellular infrastructures and spatial framework, thus, improving our comprehension of the unique cells within the tissues in our body. Researchers use single-cell analysis for a variety of applications including disease research, personalized medicine, and drug discovery. By classifying disease-specific cellular deviations and patient-specific marks, researchers can advance bespoke therapies. Furthermore, single-cell analysis can aid drug discovery by illuminating how single cells react to treatments, in that way, ascertaining prospective drug targets and assessing drug efficacy.

10x Genomics Tech Uses In Diseases (10x Genomics)

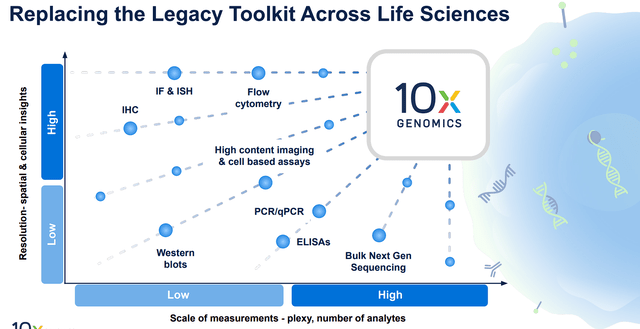

The company’s instruments, products, and software have the potential to replace a variety of older tech, due to higher performance and scale.

10x Genomics Replacing Older Tech (10x Genomics)

Some of these instruments and kits are the gold standard in certain applications. So, it is feasible that 10x’s products could ultimately replace them as the go-to instrument in their respective research fields.

What does that mean in terms of revenue?

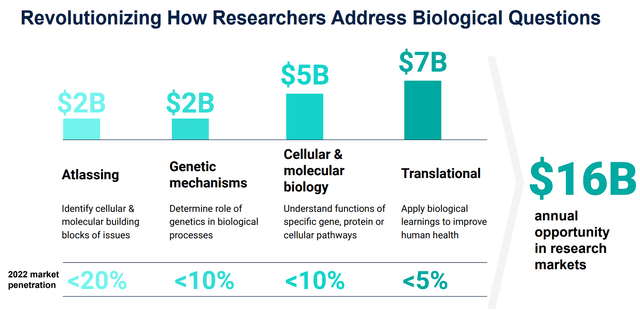

Well, the company believes that its products could allow them to be a significant player in atlassing, genetic mechanisms, cellular & molecular biology, and translational biology, which is a $16B market opportunities.

10x Genomics Estimated Market Opportunity (10x Genomics)

Being a major player in multi-billion dollar markets should yield significant revenue growth in the coming years. In fact, Street analysts believe the company is going to report strong double-digit growth into the next decade with the possibility of crossing the $1B mark in only a few years.

10x Genomics Analyst Annual Revenue Estimates (Seeking Alpha)

The company does have some competition, however, they just won a patent case against NanoString (NSTG) and Vizgen in Germany, so perhaps the road to $1B is not peppered with hurdles. Indeed, the company has numerous other competitors such as Bio-Rad (BIO), Illumina (ILMN), Becton, Dickinson, & Co. (BDX), PacBio (PACB), Fulgent Genetics (FLGT), and Mission Bio. However, it appears 10x is arguably the leader in single-cell here, so I don’t see a strong argument against the company meeting the Street’s expectations in the coming years.

Overall, 10x Genomics is becoming an entrenched name in their industry thanks to their products becoming essentially a necessity in a growing life sciences industry. A large percentage of the medicines of the future will rely upon the technology that 10x is involved in. Obviously, this could lead to a massive market opportunity in the near term and the long term. In addition, the company enjoys attractive margins and has a healthy financial position at the moment. In my view, TXG is a solid Bio Boom Portfolio candidate and is being moved closer to the top of my watch list.

Leading Risks

As with all speculative healthcare tickers, TXG has a few substantial downside risks that investors should be aware of. First, 10x Genomics is still recording losses and there is no assurance that they’ll ultimately cross the line to profitability. In addition, their industry is incredibly competitive with plenty of big players and numerous smaller outlets that could find a way to innovate a superior product in the coming years or outcompete 10x on the market. Another risk investors need to consider is the ticker’s volatility. Certainly, healthcare tickers tend to be volatile… especially companies working in genomic, healthcare tech, and life sciences tools. However, TGX went from around $200 per share to around $25 per share in just over a year, which is quite volatile considering TGX’s market cap is around $6.4B. So, TXG investors need to remain vigilant with their position and have a game plan for managing the volatility.

As a result, I would assign TGX a conviction level of 3 out of 5 in the Compounding Healthcare Bio Boom Portfolio.

Establishing a Position

In my introduction, I mentioned that TXG has been on my watch list a few years now, but I have yet to find an opportunity to establish a position. Luckily, the market took the COVID-premium out of most related tickers and brought TXG from roughly $200 a share down to about $25 a share. The stock has pulled up off the bottom and is now trading around $50 to $55 a share with a $6.5B market cap. This is still a pretty rich valuation, but I am comfortable with establishing a position at these levels due to the company’s expected long-term growth and the potential for it to be the unrivaled leader in the industry. Therefore, I’m looking to establish a laughably small starter position at these valuations and will look for opportunities to build a respectable position coming years.

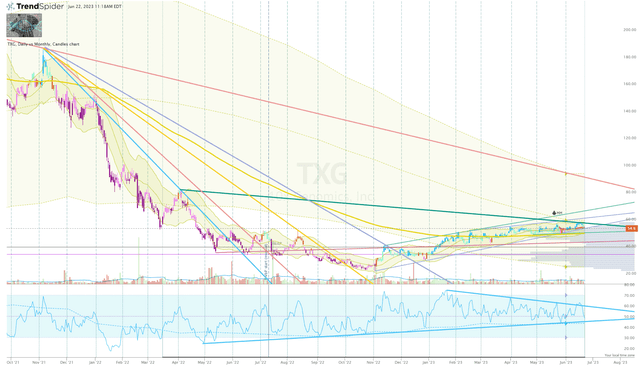

Looking at TXG’s daily chart, we can see the steep sell-off and multiple downtrend rays coming off the November 2021 high.

TXG Daily Chart (Trendspider)

TXG Daily Chart (Trendspider)

It looks as if the algorithms were in control for about a year and let up in November 2022, when the share price broke the last major downtrend ray, and it went bullish on the go-no-go indicator. We can even see a decent uptrend ray being formed and tested a few times coming from the pivot low. In addition, we can see some strength forming in the RSI with a bullish divergence. Plus, the share price has climbed above the 200-day EMA and breached the proximal aVWAP. This has set up a nice opportunity to establish a small position on a break above the current downtrend ray spawning from the April 2022 high. If the share price fails to break the trend line, I will wait to see if it drops below the uptrend ray and will wait for a solid reversal set-up before establishing a position.

Once I have established a position, I will look to make small additions to TXG over the course of the next few years. However, TXG will be a Bio Boom ticker, so the goal will be to get to the position into a “House Money” status as soon as possible through a series of trades. Thus, de-risking the position and allowing me to hold some shares for a long-term investment and possibly move TXG to my “Bioreactor” growth portfolio.

Read the full article here