When we make investment decisions, it’s important that we keep in mind that we should be in this for the long haul. This means that, sometimes, we will be wrong, even very wrong, for an extended period of time. One firm that quickly moved in the opposite direction compared to what I expected it to is Douglas Dynamics (NYSE:PLOW). This company focuses on the production and sale of various types of equipment such as snow and ice control equipment, sand and salt spreaders, and more. Despite having a rather robust 2022 fiscal year, the 2023 fiscal year has started off rough.

Shares of the company have taken a meaningful step lower in response to this. From a pricing perspective, the stock looks attractive. On top of this, management still has a rather rosy outlook for the business for the rest of the current fiscal year. To many investors, this uncertainty is justifiably problematic. But when you look at what the cause of the pain was, it becomes easier to focus on the longer-term picture rather than the short run. So even though the most recent data has not been appealing, and the stock has fallen significantly in response, I would argue that upside potential still exists from here.

Digesting bad results

In early January of this year, I found myself taking a rather bullish stance on Douglas Dynamics. Over the prior few months since I had written what was then my most recent article on it, shares had experienced an upside of 10.6% at a time when the S&P 500 was down 15.3%. Even with this move higher, I felt as though the stock was cheap enough to warrant additional upside. And because of that, I ended up keeping the ‘buy’ rating I previously assigned the stock. Unfortunately, the picture since then has been rather problematic. While the S&P 500 is up an impressive 11.6%, shares of Douglas Dynamics have plunged 19.7%.

Author – SEC EDGAR Data

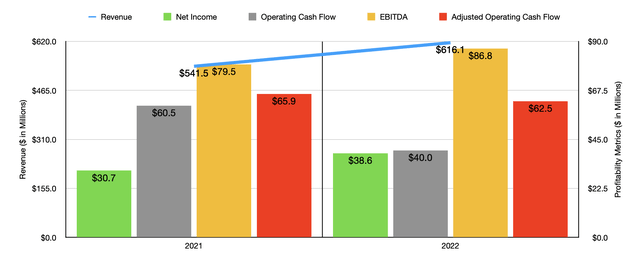

Looking at only the annual data for the company, you might be perplexed by this move lower. In 2022, for instance, revenue totaled $616.1 million. That was 13.8% above the $541.5 million the company reported one year earlier. Net income over this time grew from $30.7 million to $38.6 million. It is true that operating cash flow during this time fell from $60.5 million to $40 million, while the adjusted figure for this dipped slightly from $65.9 million to $62.5 million. However, EBITDA made up for this by growing from $79.5 million to $86.8 million.

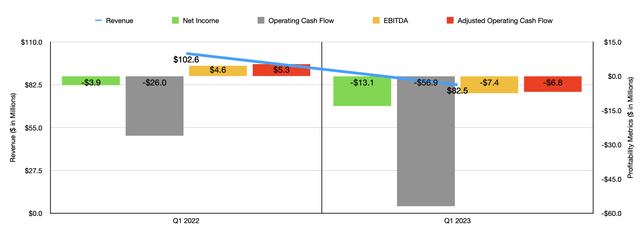

Despite the sound but mixed results, the overall picture for the company was looking up. The real pain began in early 2023. During the first quarter of the 2023 fiscal year, revenue for the company totaled $82.5 million. That’s 19.6% below the $102.6 million generated one year earlier. This decline came even as the Work Truck Solutions segment of the company, which is responsible for the production and sale of municipal snow and ice control products, storage solutions, and other related offerings, saw revenue expand from $56.8 million to $63.3 million. The pain, then, was driven by its Work Truck Attachments business. Through this segment, the company offers snow plows and sand and salt spreaders for light trucks, as well as a variety of other offerings. Revenue here plummeted from $45.8 million down to $19.2 million. This, management said, was driven largely by low snowfall in its core markets that led to lower volumes. Management even quantified this by stating that snowfall during that time was 14% lower than the 10-year average.

Author – SEC EDGAR Data

This decline in revenue brought with it an unfortunate decline in profitability as well. The firm went from generating a net loss of $3.9 million in the first quarter of 2022 to generating a loss of $13.1 million at the same time this year. Interestingly, profits for the Work Truck Solutions segment nearly doubled during this time. The real pain, then, came from the Work Truck Attachments business. EBITDA for the segment fell from $3 million to negative $10.2 million. Management did not provide specifics on why this was the case. But when you look at profits more generally, you see that the company’s gross profit was cut nearly in half, with the gross profit margin falling from 20.5% of sales to 13.7%. The vast majority of this pain was caused by a loss of economies of scale associated with the reduction in sales volume that the company experienced. Other profitability metrics also took a beating. Operating cash flow went from negative $26 million to negative $56.9 million. On an adjusted basis, it went from $5.3 million to a negative $6.8 million. And finally, EBITDA turned from $4.6 million to a negative $7.4 million.

Despite the troubled first quarter, management remains optimistic about the 2023 fiscal year. Revenue is expected to come in at between $620 million and $650 million. Earnings per share are being guided at between $1.55 and $2. At the midpoint, that would translate to net profits of $40.7 million. That’s slightly better than what was achieved in 2022. On top of this, management is forecasting an EBITDA of roughly $85-$100 million. No guidance was given when it came to other profitability metrics. But if we assume that adjusted operating cash flow should rise at the same rate that EBITDA it’s forecasted to at the midpoint, we would expect a reading this year of $66.6 million compared to the $62.5 million reported for 2022.

Author – SEC EDGAR Data

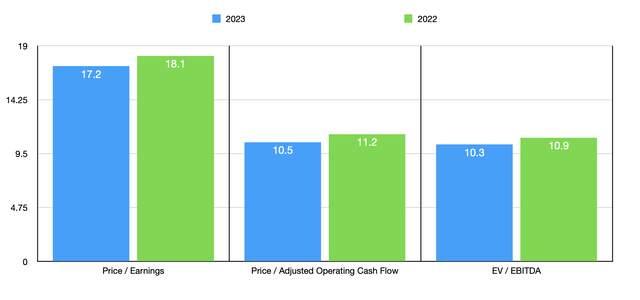

If these numbers come to fruition, shares to the company still look attractively priced. You can see what I mean by looking at the chart above that has valuation calculations for both 2022 and, using the aforementioned estimates, 2023. Relative to similar firms, the stock is closer to being fairly valued if we compare their historical data to the 2022 results. As you can see in the table below, irrespective of which of the three pricing metrics we look at, two of the companies that I compared Douglas Dynamics to ended up being cheaper than it.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Douglas Dynamics | 18.1 | 11.2 | 10.9 |

| Astec Industries (ASTE) | 125.6 | N/A | 21.7 |

| REV Group (REVG) | 40.6 | 10.6 | 12.7 |

| Wabash National (WNC) | 8.7 | 5.9 | 6.1 |

| The Shyft Group (SHYF) | 18.5 | 52.6 | 12.5 |

| Terex Corp (TEX) | 11.0 | 12.3 | 8.3 |

Takeaway

At this point in time, I remain optimistic regarding Douglas Dynamics and its potential. I can understand why investors are currently unhappy, and I would argue that the upside from here is probably less appealing than it was when I last wrote about the firm. But with the decline in price and how shares are looking from a valuation perspective, and assuming that management’s guidance comes through for the year, I would argue that some upside is warranted at this time. As such, I have decided to keep the company rated a ‘buy’ for now.

Read the full article here