By James Smith

UK retail sales rose fractionally in May, suggesting the additional bank holiday for the King’s Coronation had only a modest impact on the economy. Sales were up by 0.3% on the month, including fuel, and that saw weaker food sales around the bank holiday offset by stronger online spending, which the ONS puts down to the warmer weather. Indeed, weather seems to have been a key driver of recent month-on-month sales volumes, which otherwise have essentially flatlined in real terms for a number of months now.

None of this necessarily means UK GDP won’t temporarily contract during May, and evidence from last year’s two additional bank holidays points to a hit of roughly half a percent of monthly output, with the impact concentrated in various services industries.

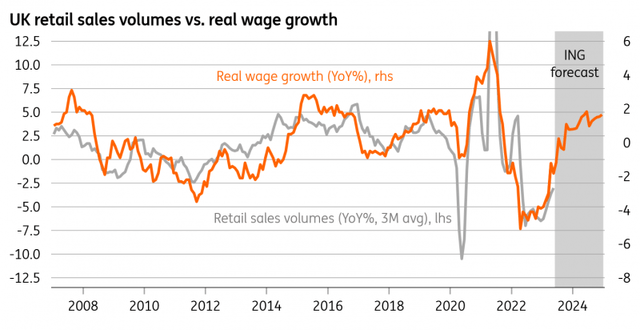

But the recent trend in retail activity suggests the worst is behind us for UK retailers, at least for now. A simple mapping of real wage growth against sales points to a very modest rebound in volumes over the coming months. The recent recovery in consumer confidence points this way too.

Improving Real Wage Growth Points To Modest Retail Sales Growth (Macrobond, ING calculations)

None of this is particularly consequential for the Bank of England, where this week’s meeting made it abundantly clear that policymakers are focused on actual inflation and wage data, and probably not a lot else. We felt Thursday’s statement marked a subtle but important sea-change in the Bank’s thinking.

So far this year, it felt like the Bank wanted to tread more carefully, having tightened a lot in a short period of time, and would watch a broad range of leading indicators, not just CPI itself, to guide policy. That’s still probably true, but June’s meeting – and the fact that seven members voted for a 50bp rate hike – signalled that the BoE is running out of confidence and patience in both its models, as well as surveys and other leading inflation metrics, both of which have pointed to improving inflation outcomes for a little while now.

While we aren’t convinced the Bank will do another 50bp rate hike in August, we suspect it’s unlikely to be satisfied with only one more 25bp move. That suggests we should expect at least one 25bp hike in both August and September.

But that would suggest the risk of recession is growing. Mortgage rates at 6% roughly equate to repayments of close to 40% of disposable income for the average consumer. The feed-through is gradual given that a relatively small share of mortgages refinance each quarter, but assuming rate cuts don’t come until the middle of next year, then that still translates into a large hit to household incomes over time. We’re also becoming more nervous about corporates – particularly small businesses – which are more commonly on variable-rate debt and will have seen rate hikes pass through more rapidly.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here