Innovative Industrial Properties, Inc. (NYSE:IIPR) is the largest publicly traded provider of real estate capital to the U.S. cannabis sector. The stock prices of its tenants have plunged over the last few years, leading to its own price to plunge as well. While IIPR did indeed trade at bubbly valuations in the past, the current valuation is not giving enough credit to the company’s higher position on the capital stack.

IIPR continues to offer exposure to the long-term growth opportunity of cannabis without the excessive tax rates and direct exposure to price fluctuations. IIPR is working through a handful of troubled tenants, but I am confident that the company will be able to reach a satisfactory recovery in the near future. With the stock trading at around a double-digit dividend yield in spite of one of the least-levered balance sheets in the real estate investment trust, or REIT, sector, I reiterate my strong buy rating for both cannabis investors and income investors alike.

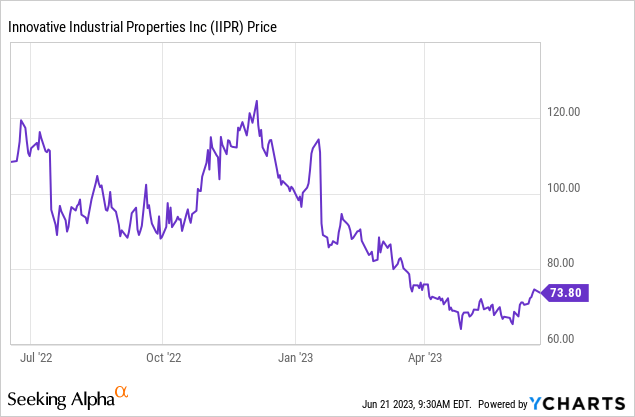

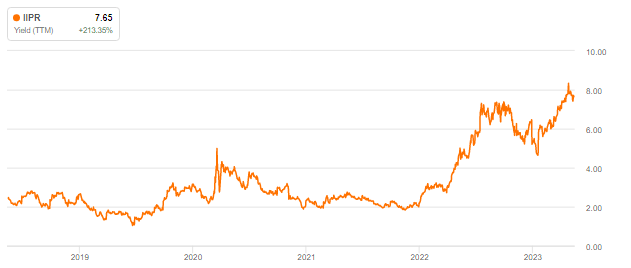

IIPR Stock Price

After plunging to around $90 per share in late 2022, IIPR attempted to recover some of its losses, rallying to as high as around $120 per share, but issues around rent collection have sent the stock crashing yet again to current levels.

I last covered IIPR in April, where I called it a deeply undervalued cannabis REIT. While the company has not yet reached a resolution on its rent collection issues, the price is right for what remains a long-term growth compounder.

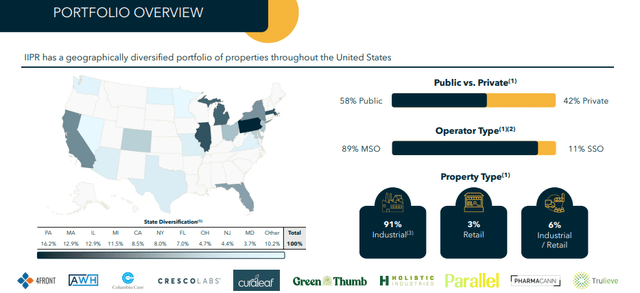

IIPR Stock Key Metrics

IIPR is the largest, publicly traded cannabis REIT in the United States. 58% of its revenues come from public tenants, with the vast majority of its properties being cultivation facilities.

May Presentation

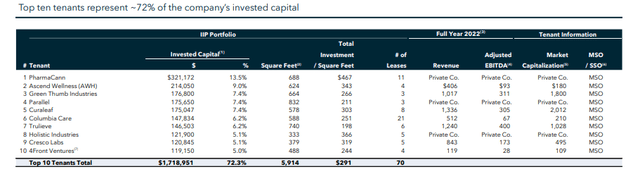

Due to cannabis still being in its early stages (it is not yet legal on the federal level but has been legalized in some states), IIPR’s tenant roster is very concentrated. Its top ten tenants make up over 70% of invested capital.

May Presentation

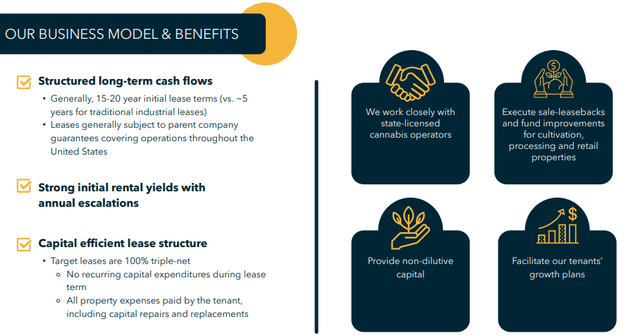

IIPR uses “triple net leases” which mean that the tenant is responsible for real estate taxes, insurance, and maintenance capital expenditures. This makes IIPR very similar to income investing favorite Realty Income Corporation (O). Because cannabis is illegal on the federal level, U.S. cannabis operators have limited access to capital, leading to attractive financing terms for capital providers like IIPR. IIPR has benefited from acquisition cap rates around 13% (compare with the 6% typical cap rate for Realty Income) and annual lease escalators around 3% (compare with the 1% annual lease escalator for Realty Income).

May Presentation

These attractive leasing terms have likely only improved given the higher interest rate environment, and one can make an argument that the faster growth prospects warrant a rich premium to O despite the higher risk. Yet the opposite is true today, with IIPR trading at a deep discount, which is likely due to the dramatic slowdown in its growth profile.

May Presentation

In its most recent quarter, IIPR generated $2.25 in AFFO per share, representing 10% YOY growth. With most REITs showing stagnating growth (in no small part due to rising costs of capital), that number is still best-in-class in the NNN REIT sector, but investors may be comparing that result with the 20% to 100% growth of prior years. IIPR declared a $1.80 per share common dividend, representing an AFFO payout ratio of 80% and growth of 16% YOY.

IIPR trades at low valuations due to both steep pessimism in the U.S. cannabis sector as well as a handful of troubled tenants. IIPR noted that rent collection improved to 98% from 92% in the fourth quarter, but that was due to the company applying security deposits towards unpaid rent. On the conference call, management noted that it had reached an agreement with tenant Holistic Industries, which operates a California and Michigan property. Under the terms of the agreement, base rent will be paid through application of the security deposits until September, upon which the security deposits will be paid back over the next year. While not ideal, it makes sense for IIPR to work with its tenants as many may be working through over-investment following the steep growth during the pandemic.

IIPR is still in the process of seeking resolution with a Pennsylvania and Texas property with tenant Parallel and has applied $3.1 million of security deposits towards their unpaid rent. Finally, the company has applied security deposits towards unpaid rent for tenant Green Peak Industries’ Michigan property. Management noted that the security deposits have been fully applied – I expect the next quarter to see rent collection more similar with the fourth quarter. Ironically, California tenant King’s Garden (which had initially caused the stock’s crash in the first place) is noted to be paying rent at their four properties and continues “to explore a potential merger transaction.”

Is IIPR Stock a Buy, Sell, or Hold?

Some investors might wonder if the market reaction is overblown. They might point out that IIPR has seen strong rent collection even during the pandemic, and rent collection has only dipped slightly as of recently.

May Presentation

While I am bullish on the stock, I’d counter that the past performance must matter less than how the current deterioration in rent collection may impact future rent collection, especially considering that cannabis prices and interest rates are in a different state than they were in the past. At the same time, the current valuation is arguably too pessimistic. IIPR is trading at just around 10x funds from operations (“FFO”) estimates – and I note that FFO converts quite efficiently to free cash flow due to the net lease structure (an important point for REIT investors).

Seeking Alpha

IIPR trades at its highest dividend yield historically, though this point might not be so relevant given that it was in hypergrowth mode in the recent past.

Seeking Alpha

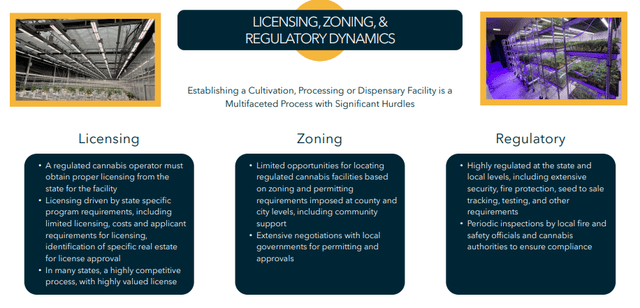

Things may look pessimistic in cannabis at present, but I remain bullish on the long-term future, especially for capital providers like IIPR. This is because even in states which have legalized cannabis, legal licenses are often limited, adding inherent value to even struggling properties. It is not so trivial for new legal competition to emerge.

May Presentation

While I am uncertain how much recovery value IIPR might get from their California properties given that California is an unlimited license state, I am confident that it should be able to drive strong recoveries from the other troubled properties like those in Pennsylvania and Texas.

Equally importantly, IIPR is under-levered relative to NNN REIT peers, with total debt at around $304 million and a debt to EBITDA ratio of just over 1x (compare to the 5x to 6x typical ratio in the sector). The double-digit dividend yield seems to imply a greater likelihood of catastrophic outcomes here, but absent a complete collapse of the U.S. cannabis business model, IIPR in theory should have less risk than the typical NNN REIT. In my analysis of other troubled REITs in the past, it is almost always debt – not a handful of troubled tenants – that leads to irreparable damage to the stock price. This is because REITs typically need to direct cash towards bringing down leverage when times get tough (and even potentially needing to issue equity), but that is not the case here due to leverage being so minimal.

With O and other NNN REITs trading at dividend yields in the 6% to 7% range, I still see IIPR trading at least in-line with that group, though a real argument can be made that IIPR should trade at a large premium due to growth rates that more closely resemble that of industrial REITs. It is possible that IIPR may have to cut its dividend if more struggling tenants emerge, but that should be priced into the double-digit yield. I note that IIPR could see revenue decline by 17% before the AFFO payout ratio reaches 100% – and due to the net lease business model, that dividend would still be self-sustaining as the company does not have material recurring capital expenditure requirements. In fact, revenues could decline by as much as 40% and the stock would still be trading at around 15x AFFO.

I view such an outcome as being overly pessimistic – due to substantial recovery prospects I already see a 20% haircut to revenue as being the worst of an apocalyptic scenario. This is a stock which I see eventually trading up to 20x-30x AFFO over time, though there are admittedly limited catalysts at the company’s disposal due to negative sentiment being the primary driver of the stock’s underperformance. In the meantime, the double-digit dividend yield gives investors plenty of reasons to wait.

What are the key risks? Some investors may mistakenly think that positive legislative reform is the biggest risk. That might have been true if IIPR was trading in the $200 level, but at these valuations, any legislative reform which improves cost of capital for its tenants is ironically a clear positive. Yes, an increase of capital availability in the sector would reduce the financing terms on new acquisitions moving forward (I expect cap rates to compress from around 13% today to around 8% to 9%) but such an event would have positive implications for the credit profile of its tenants. IIPR would undoubtedly benefit from substantial multiple expansion as the main bearish thesis facing the stock – poor credit quality of its tenants – would have been more or less addressed. In some ways, IIPR stock at these prices can be a winner with or without legislative reform. The main bearish thesis is if legislative reform takes too long, or if financial conditions continue to worsen for US cannabis operators.

I view cannabis as eventually being a household staple like Tylenol – but there are many regulatory hurdles that must take place before that becomes reality. In the meantime, legal operators face challenges from price compression and competition with the illicit market. If local governments do not find ways to limit the reach of the illicit market, or even take drastic steps like removing the limited license model, then I would expect prices to fall dramatically and for legal operators to suffer. I find such an outcome unlikely given the sizable practical challenges posed by large cultivation facilities (if anything, citizens likely will protest the smell), but it is very difficult to predict political outcomes.

While I continue to favor the smaller and cheaper peer in NewLake Capital Partners, Inc. (OTCQX:NLCP), IIPR remains buyable in its own right and should continue to benefit from its listing on major exchanges. I reiterate my strong buy rating for Innovative Industrial Properties, Inc. stock, but caution that patience is needed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here