Here at the Lab, we usually focus on companies with a market cap of at least $5 billion; however, today, we want to present Signify (OTCPK:PHPPY, OTCPK:SFFYF). We believe a selection of smaller European caps might protect your diversified portfolio, and thanks to the EU Green Deal part of the €1.8 trillion European Union 2021-27 budget, this could be a trend that cannot go unnoticed for our company. Indeed, Signify could transform a threat into a business opportunity. Why?

- The company is currently supporting the fight against climate thanks to various divisions dedicated to lowering electricity requirements without compromising the lights needed;

- Signify has solid governance with a capable board dedicated to ESG initiatives;

- Since 2020, the company had a straightforward net zero program with a strict supplier sustainability program. As a reminder, its raw material exposure makes its internal auditing supplier with the highest sector standing requirements, providing a long-term MACRO upside in our investment decision-making.

- In addition, green investments are not dedicated only to major utility companies such as Enel (OTCPK:ENLAY), NextEra (NEE), Canadian Solar (CSIQ), or Iberdrola (OTCPK:IBDRY) but also to companies operating in sectors that will positively influence our environment. Construction-renovation and circular economy corporations could benefit from the Green Deal initiative and help the European Union achieve its ambitious goal. In our coverage, we also highlight to check our detailed analysis of Holcim (OTCPK:HCMLF), Heidelberg Materials (OTCPK:HLBZF), Schneider Electric (OTCPK:SBGSF), and International Paper (IP).

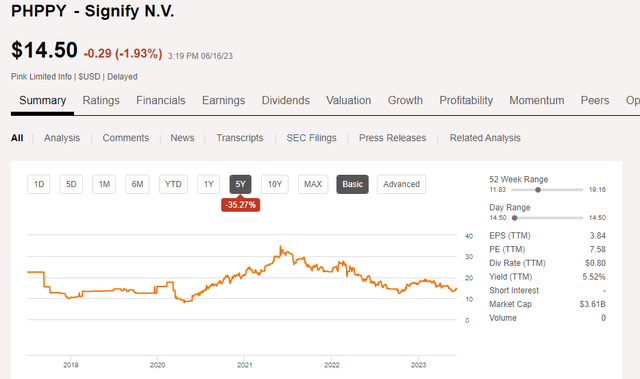

Even if we never published an article, Signify is a company we have followed since 2020. Given the last trailing twelve months of stock price depreciation, we believe it is back to a price range to initiate an investment. The company was formerly known as Philips Lighting NV. It is based in the Netherlands and engages in lighting solutions and lamps. It has a product portfolio that includes old incandescent (and halogen) lamps and LED lights with high-intensity discharge. In addition, to emphasize our supportive point 1), Signify provides integrated and customized lighting systems with value-added services with energy audits and remote monitoring for the new trend, such as vertical farming.

Signify stock price evolution

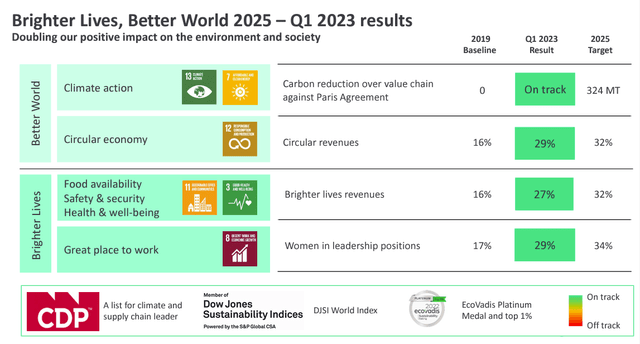

The company does not need any introduction; indeed, Signify is already the market leader in the global lighting market. In addition, the company has a higher level of product innovation and solid pricing power in a declining market for incandescent and halogen lights. However, top-line sales and margins started to be under pressure; however, here at the Lab, we are forecasting a better margin environment in H2 of 2023 and a capability of preserving margins by reducing costs. The company has always been in the Dow Jones Sustainability World Index (Fig below). It did a compelling job transforming its business under pressure from conventional lighting by anticipating energy-efficient lighting demand.

Signify ESG results

Q1 Results

Very briefly, the company reported weaker-than-expected Q1 results compared to Wall Street consensus estimates. Organic top-line sales growth was below expectation, with an adjusted EBITA margin that missed consensus by 7% and was down by almost 20% on a yearly basis. The lower sales were mainly due to consumer and professional indoor weakness, and margins were impacted by FX, which we believe will turn into a positive note for the remainder of the year. The CEO confirmed that Q1 figures were largely in-line, and they forecast a weaker Q2 before a step up in margins for the second part of the year. Looking at the latest financial figure, we are surprised to see a 300 basis point margin impact with normalizing some costs, such as logistics and energy.

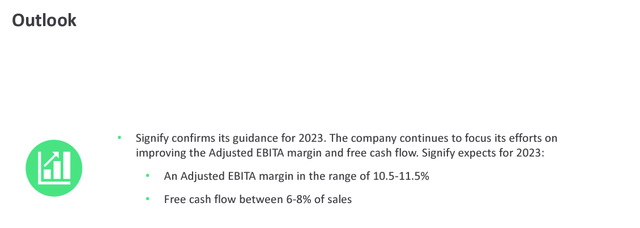

Signify 2023 outlook

Valuation and Risks

For this reason, considering a weak Q1 and a challenging economic environment, we decided to lower the 2023 and 2024 forecasts by 2%. Compared to 2022 results, we forecast a declining growth rate of 4.7% and 3% in 2023 and 2024. At the adjusted EBITA level, we are anticipating a margin of 10.1% and 10.2% for the next two years, cutting our EPS estimates by 6%. Despite that, the company is currently trading with an adj. price earning of 9x with a free cash flow yield higher than 16%. Therefore, we see valuation support combined with a solid dividend yield (higher than 5.5%). Signify’s investment case is solid, given the strong cash flow generation that covers the current dividend payment. Mare’s target price is derived from an 8.5x multiple on the 2024 estimate of the company’s core operating profit. This is in line with Signify’s historical average. Considering our lower EBIT, we still arrived at a €38 per share valuation ($20.5 in ADR) with a potential upside of 48%. Downside risks include lower sales, higher working capital requirements with a reduction in FCF generation, further commoditization of the company’s product portfolio, lower benefit from scale, higher competition with new entrants, and a longer lifetime of LED.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here