Danimer Scientific’s (NYSE:DNMR) biodegradable plastics dream didn’t turn into a nightmare overnight. The market was somewhat patient but eventually gave way to what’s become a chain of poor quarterly earnings. Danimer went public just before the unfettered SPAC euphoria of 2021’s winter with the market embracing the promise behind its Nodax PHA to form a part of the solution to the proliferation of fossil-based plastics in our oceans and waterways. Nodax is a fully biodegradable, sustainable, and renewable plastic that uses canola oil as its primary feedstock. The bull case here is built around consumer shopping habits increasingly taking into account environmental factors. Millennials and Gen Z are creating a new category of green consumers who want their brands to embrace sustainability and purpose.

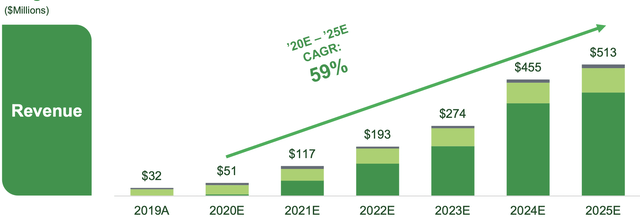

This growing environmental conscientiousness was meant to drive consumer product companies to embrace PHA en masse and drive revenue for Danimer to ever-growing highs. However, whilst around 65% of consumers state they want to buy sustainable brands only around 26% actually do. Demand for Nodax has been poor especially when set against now abandoned guidance Danimer provided when it went public via a special purpose acquisition company. Management initially penciled in a 59% compound annual growth rate from 2020 to 2025 with 2023 originally set to see quarterly revenues of $68.5 million.

Danimer Scientific October 2020 SPAC Presentation

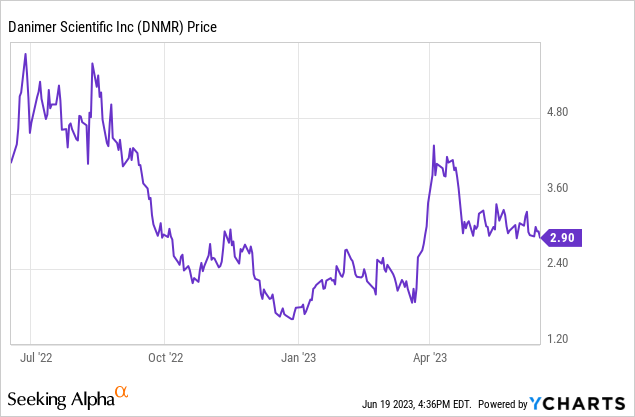

What’s the trade here? To avoid the commons. Indeed, the company’s price to trailing 12-month earnings multiple at 5.83x is significantly above its peer group median of 1.09x. It’s also at odds with a plethora of deSPACs from the same 2020 – 2021 class who in chasing various shades of ESG dreams have reverted to a sub 1x price to sales multiple. To be clear here, there is still a lot of latent optimism within Danimer’s common shares as the market continues to price in a near-term ramp in revenue.

Falling Revenues And Negative Gross Margins

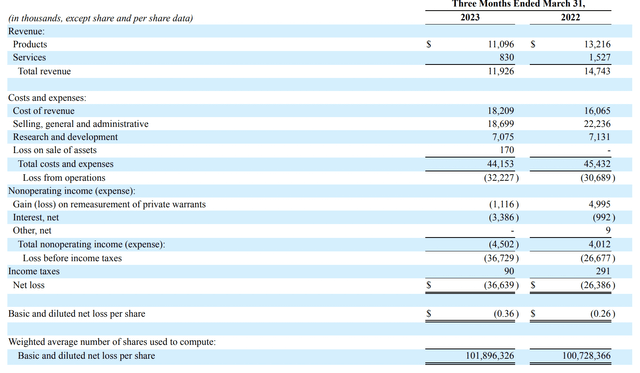

Danimer recorded fiscal 2023 first-quarter revenue of $11.9 million, a 19.3% decrease over its year-ago quarter and a miss by $2.49 million on consensus estimates. Gross profit was negative at $6.3 million and was an increase from a negative gross profit of $1.3 million in the year-ago comp. Gross profit margins were negative at 52.6% but were disrupted by a $3.4 million noncash depreciation and amortization expense. Adjusted gross profit, which strips this out, was only negative by $1 million versus a positive adjusted gross profit of $2 million in the year-ago comp.

Danimer Scientific Fiscal 2023 First Quarter Form 10-Q

Net loss was $0.36 per share, an increase of $0.10 over the year-ago period with a $3.56 million saving on SG&A expenses offset by interest expenses increasing to $3.39 million from just $992,000 in the year-ago quarter. Shareholders were expecting better results as implied by the multiple. The company also did not provide any revenue guidance, choosing instead to highlight an adjusted EBITDA loss that is expected to be in the range of $23 million to $31 million. Adjusted EBITDA did fall during the first quarter to $8.9 million from $10.6 million. This momentum is expected to continue through 2023 against an adjusted EBITDA loss of $45 million in the 2022 fiscal year.

A Struggling ESG Darling

Against these losses, the company’s liquidity position becomes one of the most critical metrics for assessing a long position. Danimer’s cash and equivalents as of the end of the quarter at $102 million increased from $62 million in the year-ago period. The company also had a restricted cash balance of $17.6 million mostly related to an interest reserve account for an IP term loan. Critically, Danimer is having to take on more debt to extend its cash runway which stands at around 6 quarters against free cash outflow of $22.3 million for the first quarter. This came in at a 37% reduction sequentially over the fourth quarter.

What’s the future here? Bears, which form the 17% short interest think the ticker will retest its March lows. Indeed, the company’s enterprise value to trailing 12-month sales multiple stands at 8.03x. This is with total debt of $405.6 million on its balance sheet as of the end of its first quarter. Bulls are betting that the environmental benefits of Danimer’s bioplastic are able to eventually be transformed into more tangible sales. Nodax under the right conditions breaks down in significantly less time than traditional fossil-based plastics and does not leave behind harmful microplastics to offer a significantly better beginning-of-life and end-of-life cycle. The company has a nameplate capacity of 32.5 million pounds of neat PHA and a capacity for 65 million pounds of finished resin. Management expects revenue could grow to as much as $190 million at full capacity utilization and against current market pricing. Hence, there is still hope that revenue could eventually ramp if the company is able to secure greater commercial partnerships and fully utilize its remaining production capacity.

Read the full article here