There’s nothing in Keynesian economics that would allow you to solve stagflation. But there’s nothing in neoclassical economics that would allow you to solve stagflation, either. – Paul Samuelson

Stagflation is an economic state characterized by a sluggish economy, high inflation, and typically, high unemployment. In such a scenario, the economy experiences a paradoxical situation where the prices of goods and services increase, even as economic output slows down and unemployment rises.

These economic conditions are particularly difficult for policymakers to manage. Measures to stimulate economic growth often exacerbate inflation, and steps to control inflation can further hinder growth and increase unemployment.

The Fed seems to be confident that it can break inflation sustainably with higher rates, but the problem ultimately is hard to solve long-term in the absence of competition. Increasingly we find ourselves in a world where nearly every industry is an oligopoly.

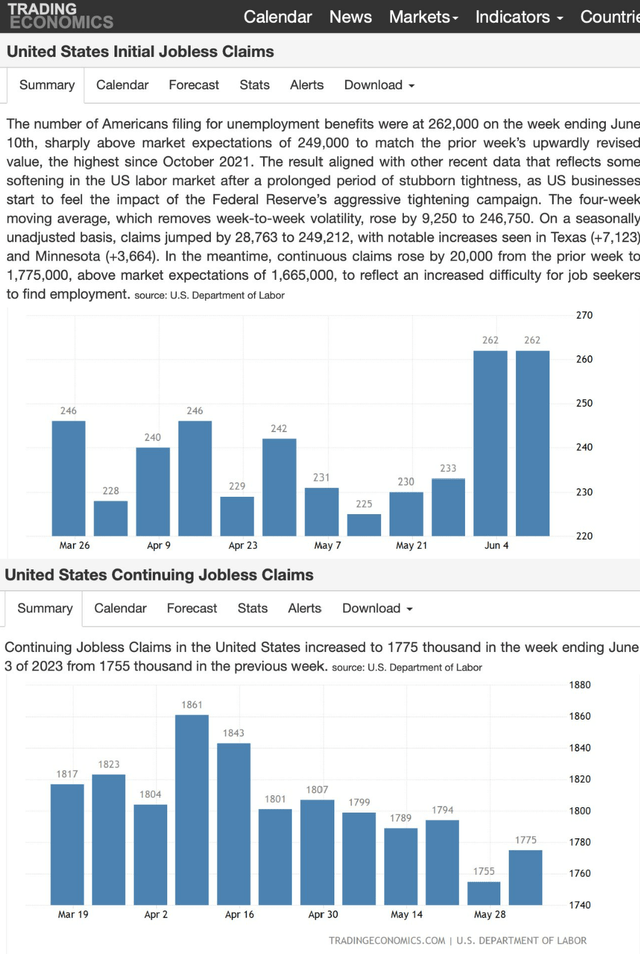

Competition ultimately solves inflation while keeping unemployment low. It doesn’t look like that’s going to happen for now, all while jobless claims are just starting to pick up.

TradingEconomics.com

Historical Context of Stagflation

Stagflation was once considered an impossibility by economists. The economic theories of the 20th century, particularly the Phillips Curve within Keynesian economics, described macroeconomic policy as a trade-off between unemployment and inflation.

However, the phenomenon of stagflation in the 1970s debunked these theories. The 1970s stagflation was primarily driven by three factors: a dovish Federal Reserve policy that accepted inflation for reduced unemployment; increased government spending on social programs and the Vietnam War; and cost-push inflation triggered by the oil embargo and rising commodity prices.

Stagflation in the Modern Context

While the phenomenon of stagflation hasn’t repeated itself since the 1970s, the threat of its reoccurrence remains. The global economy today exhibits certain characteristics similar to the 1970s. The Fed’s efforts to stimulate the economy through monetary policy, increased government spending due to the COVID-19 pandemic, and the rising prices of commodities due to supply-chain disruptions could potentially set the stage for longer-term stagflation.

Moreover, recent data indicating slowing economic growth and elevated inflation have raised concerns about the likelihood of stagflation. Although unemployment rates are currently low, they could potentially rise if economic growth continues to slow, and at a much faster rate of change than inflation dropping

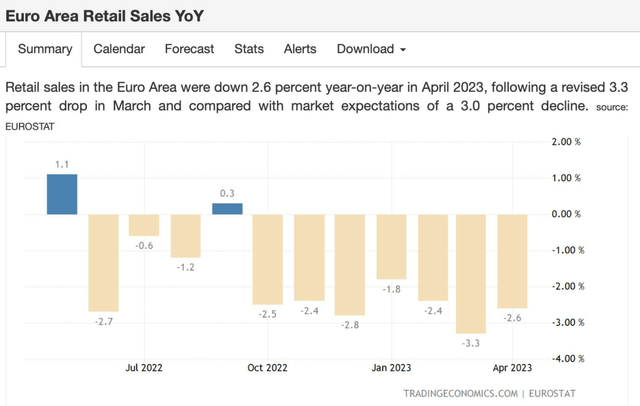

Europe (VEA) seems to be at most risk for this from a prolonged cycle perspective as Lagarde continuously references the need to raise rates despite the Eurozone being in recession now. Retail sales continue to be weak, yet there’s no policy reversal imminent by the European Central Bank.

TradingEconomics.com

The Merk Stagflation ETF (STGF)

Are there ways of investing in stagflationary periods? Yes – largely through Treasury Inflation Protected Securities (TIP), Real Estate (IYR), Gold (GLD), Oil, and the Dollar (UUP). While TIPS were not around during the stagflation of the 1970s, it makes sense that they serve as a good hedge. One good all-encompassing asset allocation portfolio I’m a fan of is the Merk Stagflation ETF (STGF), which tracks a portfolio divided between 55%-85% U.S. Treasury Inflation-Protected Securities (TIPS) and between 5%-15% real estate, gold, and oil. The fund is designed to rebalance as needed to maintain these allocations.

Conclusion

The risk of stagflation remains a contentious topic. While some indicators suggest an increasing likelihood of stagflation, others argue that these signals may be misleading. I have gone on record before arguing that I tend to be more of a disinflation/deflationist given demographics, the wealth gap, and technology, but stagflation is a very real longer term risk. And if that indeed is the direction we are headed, the “new bull market” won’t be in the S&P 500 (SPY), but rather parts of the marketplace that tend to get much less media coverage than stocks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Anticipate Crashes, Corrections, and Bear Markets

Anticipate Crashes, Corrections, and Bear Markets

Are you tired of being a passive investor and ready to take control of your financial future? Introducing The Lead-Lag Report, an award-winning research tool designed to give you a competitive edge.

The Lead-Lag Report is your daily source for identifying risk triggers, uncovering high yield ideas, and gaining valuable macro observations. Stay ahead of the game with crucial insights into leaders, laggards, and everything in between.

Go from risk-on to risk-off with ease and confidence. Subscribe to The Lead-Lag Report today.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Read the full article here