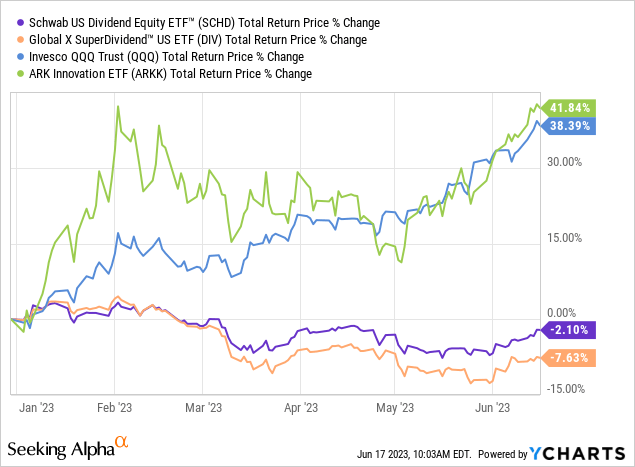

So far in 2023, high yield dividend stocks (DIV)(SCHD) have been significantly outperformed by technology stocks (QQQ)(ARKK):

The biggest reason for this massive outperformance is the advent and rapid adoption of artificial technologies like ChatGPT and the significant investments and breakthroughs being made in A.I. technologies at large tech companies like NVIDIA (NVDA), Microsoft (MSFT), Tesla (TSLA), and Alphabet (GOOG)(GOOGL). The market is largely buying the excitement over A.I. and seems to believe it will genuinely create massive long-term wealth creation.

However, one of the most successful investors in history – Berkshire Hathaway’s (BRK.A)(BRK.B) legendary Charlie Munger – is not among them.

Mr. Munger recently stated:

I’m personally skeptical of some of the hype that has gone into artificial intelligence. I think old-fashioned intelligence works pretty well.

I happen to agree with Mr. Munger on this one. As someone who has a master’s degree in engineering with focused coursework and research in artificial intelligence, I agree that there is enormous potential for this technology to disrupt and dramatically enhance our way of life. However, from an investing perspective, I think the market has gotten ahead of itself when it comes to the hype surrounding A.I.’s potential. As a result, we think that the tech sector is considerably overvalued today and therefore the high yield sector is likely to significantly outperform tech moving forward. Here are two reasons why we believe this will happen:

#1. Clear Evidences Of Bubble-Like Valuations

First and foremost, the tech sector is riddled with clear evidences of bubble-like valuations. Just like the Bitcoin (BTC-USD) mania of late 2017 fueled bubble-like valuations in blockchain-related businesses, so the A.I. mania of today is fueling bubble-like valuations in A.I.-related businesses. Yes, both are real and disruptive technologies that will likely create enormous wealth for many in the future. However, the valuations being attached to many of these businesses defy any sense of risk-reward analysis.

A classic example of this from the Bitcoin bubble was when Long Island Iced Tea – a tea and lemonade beverage maker – rebranded itself Long Blockchain Corp and the stock soared by 380% despite nothing fundamentally changing in the company. Within a few years, the stock was delisted and investors who bought the surge were left holding the bag.

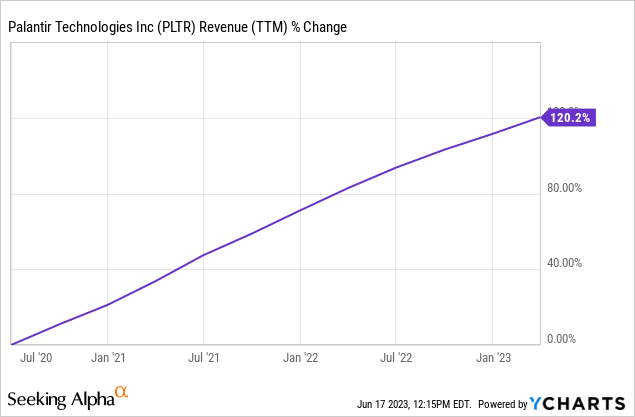

However, investors do not need to invest in such scam-like ventures today to get left holding the bag either. Take for example Palantir Technologies (PLTR), a company that is very legitimate, has been around for two decades, and creates innovative and useful data-analytics products for large organizations in both the public and private sectors. In fact, it has been growing revenue at a strong clip since its direct listing in 2020 and it just recently achieved GAAP profitability:

Management has been hyping up the A.I. potential of the company, with the company mentioning the technology 68 times in their Q1 earnings call, a sharp increase from just 17 mentions on the Q4 earnings call and a mere six mentions in the year-ago Q1 earnings call. Keep in mind that PLTR took a similar approach during the Bitcoin rally in the immediate aftermath of its direct listing, sprinkling discussions of Bitcoin and blockchain in its earnings calls in order to appeal to trend-chasing retail investor sentiment.

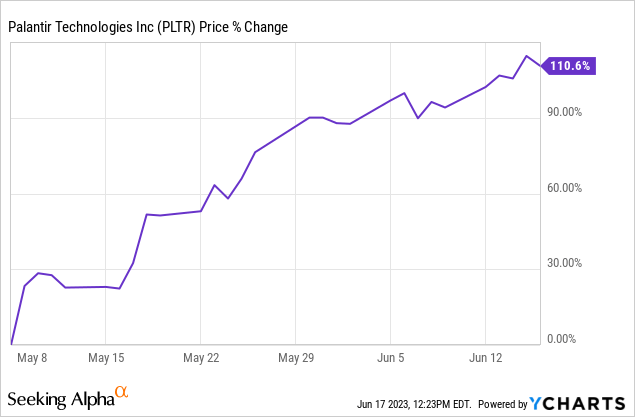

The harsh reality for PLTR, however, is that despite its stock going to the moon over the past month, largely fueled by the A.I. craze, the growth momentum for the company simply does not support its valuation.

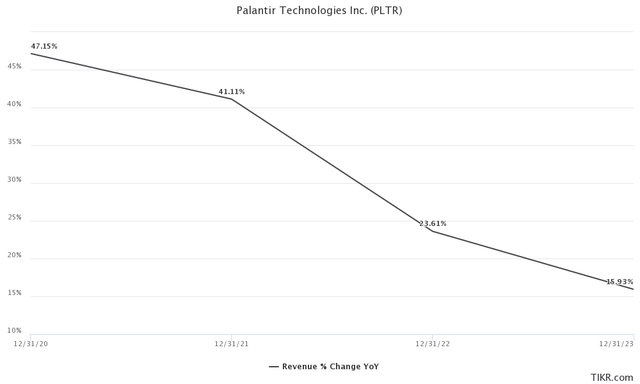

Its revenue growth has been decelerating at a rather rapid rate, despite all of the hype about A.I. and data analytics.

PLTR Revenue Growth (TIKR)

This is largely because it has already been competing for U.S. Government business for decades, making that market somewhat mature for them, and its only real commercial growth momentum has been achieved in the United States. While that is certainly large enough to fuel decent growth for years to come, their international business actually shrank in Q1. Unless they can reignite international growth – which management did not sound at all optimistic about on their latest earnings call – they are clearly miserably overvalued, trading at 72x forward earnings without much margin expansion expected (so the earnings per share CAGR is unlikely to exceed 20-25% over the next several years).

In our view, the future total return outlook for PLTR is abysmal because its growth is simply incapable of even coming close to justifying its current valuation. This situation is not isolated to PLTR either, it is spread across the technology landscape, including amongst some of the tech mega caps. This is the main reason why the S&P 500 (SPY) – which is dominated by mega cap tech stocks – is trading in very overvalued territory right now according to many of the leading market valuation models.

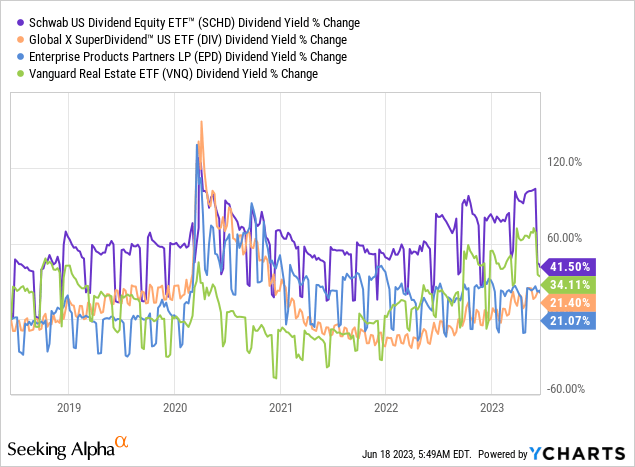

In contrast, the high yield space for the most part looks attractively valued right now. For example, yields on high yield bell-weathers such as SCHD, DIV, VNQ, and Enterprise Products Partners (EPD) are all significantly higher today than they were pre-COVID.

#2. Inflation & Interest Rates To Remain Higher For Longer

In addition to the evidence that indicates that tech stock valuations are mostly sitting in very overvalued territory, we also think that tech stocks are likely going to underperform high yield stocks moving forward because inflation and interest rates are likely going to remain higher for longer.

Given that we expect the Federal Reserve to back off its fight against inflation in the short term in order to keep the economy afloat (due to the upcoming presidential election, continued runaway deficit government spending, and the mountain of low interest rate debt maturing in the next few years), this will likely result in inflation running above the Fed’s target rate of 2% for a prolonged period of time. This in turn will prevent the Federal Reserve from returning to its previous days of easy money and ultra-low interest rates.

This will pose as a much greater headwind to high growth tech companies since their cash flows are generated much further out in the future, making their intrinsic value much more sensitive to discount rates. In contrast, high yield stocks by definition generate a much higher percentage of their future cash flows in the near-term, making them less sensitive to discount rates. Moreover, high growth tech companies in cutting edge areas like artificial intelligence generally need significant access to more capital since they have to invest aggressively in research and development and growth initiatives in order to develop their business models and capture market share. Higher interest rates makes this much more burdensome to accomplish and dilutive to existing shareholders. In contrast, high yield stocks generally have much lower capital needs given that they are able and focused on returning capital to investors rather than raising and deploying it.

Investor Takeaway

Back in December of 2020, we launched High Yield Investor precisely because we saw a major disconnect in the markets, where things had gotten too frothy for the high growth tech sector while many quality high yield names had been beaten down and left for dead by Mr. Market without good reason. As a result, we issued the warning that “High Yield Should Pummel Tech” in the coming years.

Since then, our high yield portfolio has proven us correct, beating SPY by 178%, QQQ by 136%, and ARKK has been totally left in the dust with it still at a negative 60% total return since that call was made. We share Charlie Munger’s skepticism that A.I. will deliver the immediate riches that the market seems to believe it will and also believe that high yield will resume its convincing outperformance of tech in the near future.

Read the full article here