Summary of revised investment thesis

Six months after its sharp selloff following the BeAT-HF trial readouts, investors have shown conviction in CVRx Inc (NASDAQ:CVRX) once again. Shares are up 38% since my last publication, with all of the post-mortem of the Barostim data now fully priced in my view.

Shares have now broken out above previous highs, with multiple catalysts emerging on fundamental grounds, including Barostim, plus on sentimental factors. The stock is priced at a premium given the revised expectations, but there is a reasonable price to be paid given the growth prospects on offer. I am looking to c.$40mm in turnover from CVRX this year, and look to a $20 share price target with the catalysts mentioned here. Net-net, reiterate buy.

Figure 1.

Data: Updata

Latest BeAT-HF/Barostim updates

The major talking points are around the company’s BeAT-HF and Barostim story. As noted, last quarter was a difficult one as the market reacted (arguably over-reacted)to the company’s BeAT-HF trial readouts. I covered this extensively in the last publication. Turning to the latest updates, I would advise the following to investors:

- Interactive discussions with FDA: The company has started discussions with the FDA to get its BeAT-HF submission rolling. CVRX aims to present information that is most useful for the regulatory authorities to get Barostim’s label expansion, which may or may not expedite the process. Whatever is chosen to be presented will be crucial in demonstrating Barostim’s efficacy and safety holds up well.

- Labeling: CVRX is seeking treatment-effect labeling for Barostim. There are two ways to file a PMA supplement, and CVRX has opted to choose the interactive route to achieve it. This will be more effective in my view, as it gets the company in front of the FDA, where it can demonstrate the case for label expansion, on the evidence from BeAT-HF is supported as therapy for patients with heart failure.

The outcome of these discussions, and the potential augmentation or decrease of labeling, are yet to be determined. From an investment perspective, intelligent investors will be watching the FDA’s language very closely when it makes the next decisions on BeAT-HF. The point being that, if CVRX gets the result it is chasing (that is, to expand the Barostim label to support the treatment of heart failure) this could be a huge catalyst for the stock price in my view.

The risk is if the company doesn’t get what it wants. We saw the market’s reaction to this last time, highlighting the value it is placing on Barostim in CVRX’s valuation.

Alas, the critical factor which could turn CVRX’s market value in either direction is the next moves surrounding BeAT-HF.

Run-down of Q1 financials

CVRX clipped Q1 FY’23 sales of $8mm, another 96% upside on last year. The U.S. heart failure business contributed $6.8mm to the top line, up ~132% YoY. Notably, March was the company’s best-performing month on record, underscoring the accelerating top-line sales ramp in the U.S..

Critically, according to the CEO on the call:

While we don’t know how much of the revenue performance in March is attributable to the announced unblinding of the BeAT-HF study in February or to our commercial execution over recent quarters, we can definitely say our strategy is working.”

The company also expanded its reach by adding 3 new territories, bringing its total to 29. By capturing new territories, securing new accounts, and raising awareness among physicians about Barostim, CVRX looks to have achieved a reasonable return on this, as seen in U.S. heart failure revenue totaling $6.8mm in Q1. Despite all the calamity in CVRX’s financial markets, in its end-markets, adoption is accelerating at pace.

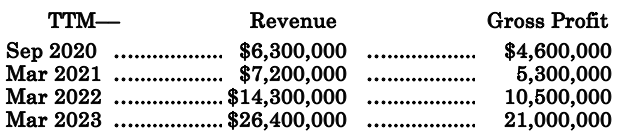

“Growth company” is a term that is spread loosely amongst modern investment markets. There simply isn’t the amount of qualified growth companies that investors seem to think there are. CVRX on the other hand, does in fact qualify as an authentic purveyor of growth, as observed below:

Table 1. CVRX revenue growth

Data: Author, CVRX SEC Filings

Revenues are near doubling each quarter (TTM basis) with tremendous gross profit margins clipped on this. With clarity on Barostim, this could extend this performance even further in my view.

Adding to the above point, CVRX’s had 122 active implanting centers on its books at the end of Q1 FY’23, compared to 56 centers in March FY’22, and 106 centers in December last year. Again, this is further evidence of the rapid uptake of its core offerings.

Peeling back the superficial layers, my additional quarterly take outs include:

- The company’s market expansion: CVRX’s expansion into new sales territories and accounts presents a compelling investment implication in my view. You’ve got 66 new centers from Q1 last year, and another 16 in 1 quarter. That is an average of 16 new sites per quarter, with each site contributing an average $216,400 per center in Q1. Like-for-like, this is down off $255,250 the year prior, indicating that each center needs less average revenue per year in order to hit its future growth targets, taking the pressure off each individual site.

- Growing physician awareness: Management notes that a bulk of Q1 growth came from enhanced awareness among physicians on Barostim. This is critical to the success, so it is good to see management still heavily pushing its core sales routes.

Both points are conducive to the revised thesis, along with the other points raised so far.

Sentiment changes

Chief to my view that CVRX will trade higher into the coming months is the recent changes in sentiment. We see this in a number of ways.

One, there have been 5 upward revisions from analysts over the coming 3-months, with no revisions to the downside. Consensus expects another 63% YoY growth in revenue this year, with another c.50% in FY’24. These changes are welcomed and absolutely essential to CVRX rating higher in my view. It is corroboration from other sophisticated investor circles that prospects on the company’s outlook deserve to be revised higher. This adds some confidence to my own assumptions too.

Figure 2.

Data: Seeking Alpha

Very interesting data is observed in the options chain for July 2023 expiry. For those contracts currently in the money, there is heavy demand centered around the $20 strike mark on the call ladder, suggesting that investors are heavily bullish at that mark. This means that investors are projecting CVRX to trade higher than this, where they can exercise their calls and buy CVRX stock at a discounted market price. Key point is, they believe it will go higher than $20,, another 42% upside potential as I write.

Together, this analysis shows the sentiment on CVRX is turning more bullish, based on the actions of actual market participants who are assuming actual risk and putting actual money to work. Hence, I form the view that there are sentimental catalysts that could drive the company’s valuation higher too.

Valuation factors

Investors aren’t parting with their CVRX stock with ease, asking 8x sales to sell their position to you. Or you’d pay 4x book value, take your pick. That’s quite the premium on both multiples, but CVRX’s valuation is reflected in both forward sales growth and equity factors, which are both represented in these multiples. Further, investors are paying these prices with no objection, as seen in the price action and momentum factors.

Hence, the market is expecting CVRX to trade at 8x its projected sales, a tremendous projection that tells me of the growth potential. Second, the market is expecting its net asset value to increase by a factor of 4x, further indication of these growth percentages.

Hence, whilst these might look pricey on face value, think a little further as to what it might be getting you:

- Management project $35-$38mm in FY’23 sales, calling for 68% YoY growth. Consensus expects roughly the same, and my numbers are in the same ranges.

- The Barostim potential, which simply cannot be ignored.

- Management demonstrated their unwavering commitment to getting the right result from BeAT-HF.

These are attractive features and if the growth percentages do work out over the coming 3-years, those multiples don’t seem too inappropriate at just $14.90 per share as I write. At 11x forward, I am getting to a valuation of $20 on $38mm in FY’23 revenue estimates (11×38/20 = $20), c.40% upside potential. This supports a buy rating.

In short

The culmination of these factors suggest that CVRX warrants a revised buy rating. The BeAT-HF data has undoubtedly been priced in, and management are working on securing the next best option, which is still a tremendous opportunity. A $35-$40 revenue clip is not unreasonable to expect for the company this year in my view, and this is supported by management and consensus estimates. Net-net, revise to buy at $20 price target.

Read the full article here