General Dynamics (NYSE:GD) is a proven compounder. This is a stock that you can feel comfortable owning for the long haul, and you can sleep well knowing that your money is safe. The firm had a rough earnings report on aerospace concerns and lackluster profit growth. However, those who own a stock for dividends know that such short-term price weakness is an opportunity to accumulate compounders like this name.

Company Reports

I always like long-term compounders that have fundamental drivers detached from economic cyclicality. Of course, General Dynamics is primarily dependent on US defense spending as a profit driver. The firm has a unique place in the defense industrial complex, and it is one of the most important firms for ammunition production, which has been prioritized in the 2024 Defense Budget.

The company produces the artillery shells that Ukrainians are burning through with ferocity. Global governments have surely realized they’ll need much bigger stockpiles, which will benefit the firm.

If you’re not already a long-term owner of this underappreciated stock, then let me give you a few reasons to join a club that includes many very wealthy folks who have wisely sat idle as owners and let this extraordinary company and their extraordinary employees deliver consistently over the past decades.

- General Dynamics is “the littlest big guy” in the very competitively entrenched US Defense & Aerospace Industry.

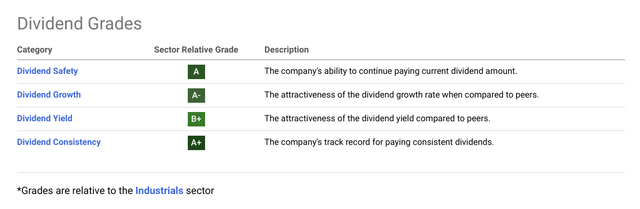

- The firm is an established dividend aristocrat and has proven it will prioritize rewarding shareholders through thick and thin.

- As I mentioned in my last piece on the defense stalwart, the firm has impeccable management and a CEO who has run the Defense Budget for a US President.

- Supply chain issues have been acute over the past years, but there are indications that these will be alleviated in the coming quarters.

- Uncle Sam is accommodating the industry in many ways, making it easier for them to achieve certainty in contracts and surmount obstacles.

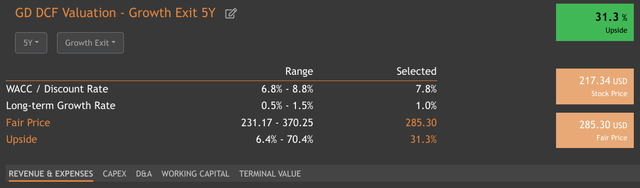

It is one thing to buy a company with these tailwinds that haven’t proven themselves, but General Dynamics has been an exceptional steward of shareholder interests by any measure. It also has delivered essential products to defend the free world. It is currently the most vital company for the future of perhaps the most vital leg of the nuclear triad, the Columbia Class Ballistic Missile Submarine. It’s also looking attractive from a valuation standpoint.

valueinvesting.io

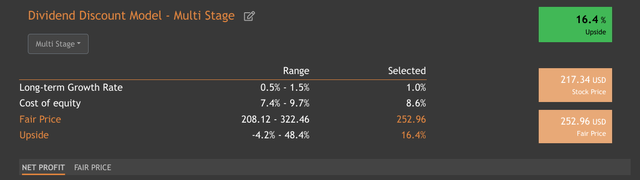

Of course, this stock is a dividend aristocrat. When a name like this is so undervalued on a DCF basis, it creates a lot of opportunity for compounding and a superior total return if you have the time to let the benefits accrue. The multi-stage Dividend Discount Model shows some tasty potential upside as well.

valueinvesting.io

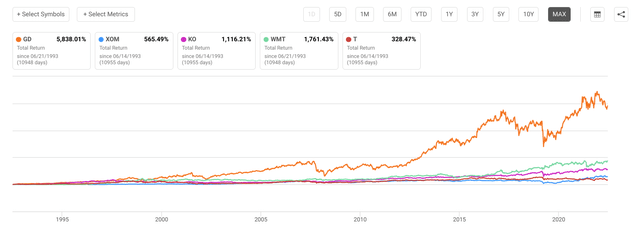

You might be surprised that the long-term returns of the name are on par with some of the most revered stocks on the market. The amazing thing about the returns over the past thirty years is that they were during a period of declining defense spending. General Dynamics has smoked the Total Return of stocks you might think of as dividend stalwarts like Exxon Mobil (XOM), Coca-Cola (KO), Walmart (WMT), and AT&T (T).

So, if you’re a dividend maven, and you have seen this company deliver through thick and thin, imagine what they’ll do with a generational tailwind of defense spending at their back.

Seeking Alpha

Given the unfortunate inertia of geopolitical events, I think that US defense spending is more likely than at any time in recent history to return to levels of spending (in terms of GDP) that haven’t been seen in four or even five decades.

Rising Demand Should Keep The Dividend Safe

The high-intensity conflict in Ukraine is stretching the global arms industry very thin. For years since the Second World War, militaries had planned for quick lightning offensives that would be so overwhelming they would quickly force the enemy into submission. In some cases, this rationale played out before our very eyes, like in 1991 when the United States defeated Iraq in the First Persian Gulf War.

That shock-and-awe victory that proved the academic whiz kids in the US Air Force correct, among other forward-thinking folks in the military, established United States military dominance until the Second Gulf War. Despite the grisly toll of that conflict and another similar counterinsurgency campaign in Afghanistan, those were low-intensity conflicts where there was very low demand for ammunition. Indeed, the armed social work of counterinsurgency discourages kinetic engagement.

In a counterinsurgency war like Iraq and Afghanistan, the conflict is two-dimensional over the hearts and minds of the people. This results in the prevalence and intensity of kinetic conflict being subdued. What this meant is that US supply structures got used to having the need for very little ammunition. One of the biggest problems was getting protected vehicles from roadside bombs, which was a problem for the defense structure.

Seeking Alpha

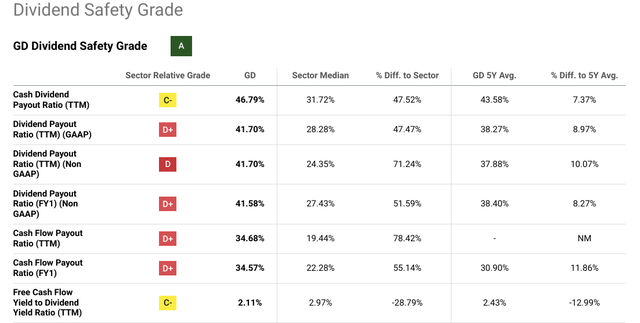

There has been some price weakness and also some negative developments around the dividend. For instance, the payout ratio has risen to pretty high levels. I am convinced, though, that many of the risks that have pressured margins are moving in the right direction. This, in addition to the transformational changes in the defense demand, make me thing this recent weakness is an opportunity to buy for dividend investors.

Risks and Where I Could Be Wrong

The Defense Industry is very mature and very industrial. Of course, the stringent regulations and exacting standards required to provide arms to the world’s strongest country are fraught with many risks. Building a nuclear submarine is obviously a very tough thing to do, and a lot of things can go wrong. In the Defense & Aerospace Industry, there are currently three major risks.

- Inflation: the nature of defense contracts and the difference in how they are accounted for and what can affect payment makes inflation a particularly pernicious risk that is amplified by the near-monopsony status of the industry. Inflation can very easily pressure margins, but the recent CPI report suggests that inflation is coming back down to more historically normal levels.

- Labor: this is one area in particular that can affect General Dynamics acutely. The shipbuilding industry is a highly fickle and highly specialized one. Furthermore, some of the biggest ticket items that General Dynamics is working on, like the Columbia Class Submarine, are also amongst the most closely guarded secrets of the United States government, which complicates production.

- Supply Chain: COVID and a deteriorating environment of cooperation for global trade have provided a double whammy to highly complex defense supply chains, often involving hundreds or even thousands of suppliers. Chips were a major concern, but some of that has been alleviated. However, because of the intense specifications and labor requirements, even minor components you wouldn’t expect can significantly hold up production. This proved a drag on the last earnings report.

One of the biggest risks to General Dynamics when I last covered the stock was that House Republicans were murmuring about defense spending cuts. Now that issue is definitively in the rearview. It has gone from a risk to an asset, and the recent debt ceiling deal has shown that both sides of the aisle consider Defense Spending sacrosanct.

This is incredibly supportive of future dividend growth, given that the 2008 Financial Crisis and COVID-19 couldn’t stop this company from prioritizing shareholder disbursements.

Conclusion

I have no reservations about recommending General Dynamics to investors. This is a company that has done credit to the equity class and demonstrates how it can be used to consistently deliver to shareholders through the worst events history can throw at management. This company has proven itself and adapted through two major crises over the past two decades.

Seeking Alpha

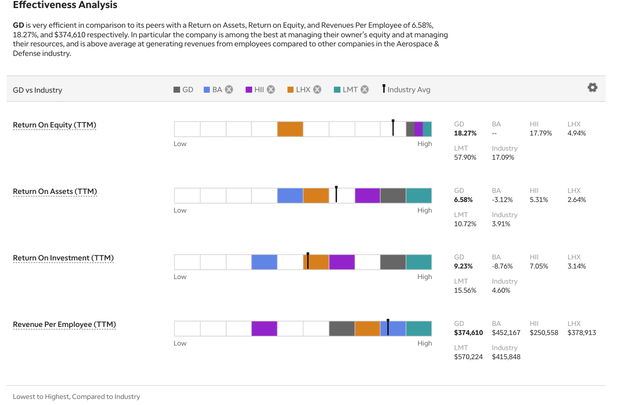

The firm is consistently ahead of its peers on key metrics that are important to me as an investor. If you’re chasing outsized returns in a short period of time, this is not the stock for you. Suppose you’re a long-term investor who knows the value of compounding and wealth preservation. In that case, I think the recent price weakness is an opportunity to either accumulate more or start building a position.

I have some close friends having kids, and I will always recommend this one as a long-term buy to hold in a new child’s name, particularly given the transformational changes in the underlying drivers of this stock’s revenue and profitability to the benefit of shareholders. General Dynamics has proven itself a more effective manager of capital than peers on many planes.

TD Ameritrade

I suspect that this trial by fire will result in returns that exceed consensus expectations going forward, given the tailwind of a generational boom in defense spending and a dual front Cold War with Russia and China. The payout ratio might concern some dividend investors, but upon examining the fundamentals, I suspect it will improve in the coming quarters and years.

This recent run-up in Technology and others is great, but if you don’t want to chase it, I think it is an excellent time to buy a proven compounder like General Dynamics. Own this stock and let it work for you, don’t trade it.

Read the full article here