Introduction

In February, I wrote an article on SA about US school furniture maker Virco Mfg. Corporation (NASDAQ:VIRC) in which I said that the company seemed to be benefitting from nearshoring due to global supply chain issues and that quarterly dividends could be reinstated soon.

In my view, the Q1 FY24 financial results were decent and the high level of orders and inventories ahead of the peak season could be an indicator of strong results for the next two quarters. In view of this, I’m upgrading my rating on the stock to a strong buy. Let’s review.

Overview of the Q1 FY24 financial results

In case you’re not familiar with Virco or my earlier coverage, here’s a brief description of the business. The company is involved in the manufacturing and sale of school and office furniture, with its main products being chairs, desks, and tables. Considering Virco is the largest producer of movable furniture and equipment for the education market in the USA, it’s possible that you’ve sat in a Virco chair during your school years or eaten at a Virco table in the cafeteria. The company has so far sold more than 65 million of its 9000 Series School Chair which was released in 1965.

Virco

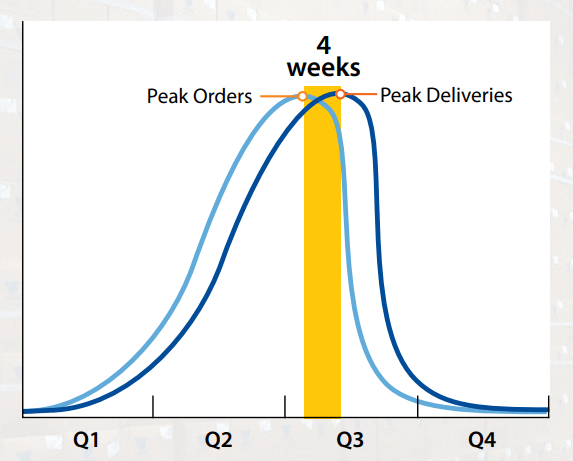

Virco generates the majority of its revenue by manufacturing and distributing products through resellers and direct-to-customers. This is a highly cyclical business, with around half of the company’s annual sales generated between June and August as educational institutions usually replace some of their furniture then. In FY23, some 47% of the company’s annual sales occurred during this period. Typically, the bulk of orders arrive about 4-6 weeks before the selling season.

Virco

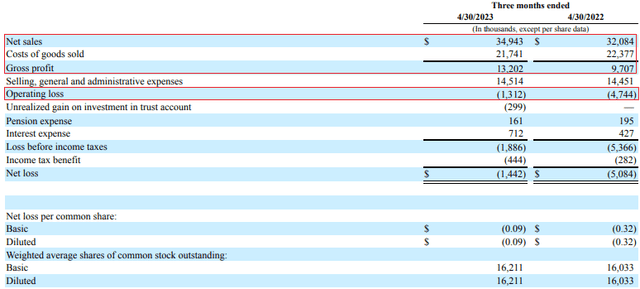

Virco usually books losses in Q1 and Q4 of its fiscal year but in Q1 FY24, the company almost managed to get in the black as net sales rose by 8.9% to $34.9 million while the operating loss shrank by 72.3% to $1.3 million. Virco started the fiscal year with a backlog of unshipped sales orders that was about $18 million higher than a year earlier and Q1 FY24 orders increased by 10.4% year on year. The main reason behind the improved profitability was a growth in the gross margin to 37.8% from 30.3% a year earlier.

Virco

During the quarter, Virco’s margins benefited from diminished international supply chain disruptions as well as price increases implemented on January 1, 2022, and July 1, 2022. The company relies on a nationwide contract to price a significant share of its orders and the price list usually determines the selling prices for goods and services for periods of a year and sometimes longer. As a result of the recent volatility in commodity and energy prices as well as high inflation rates, Virco negotiated the ability to increase prices for orders received after July 1 of each contract year. This means that the gross margin is likely to improve further over the course of FY24.

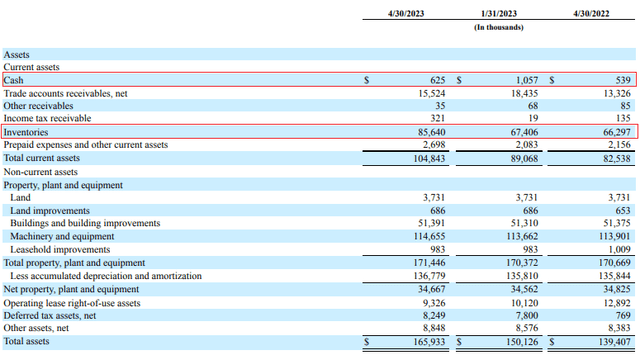

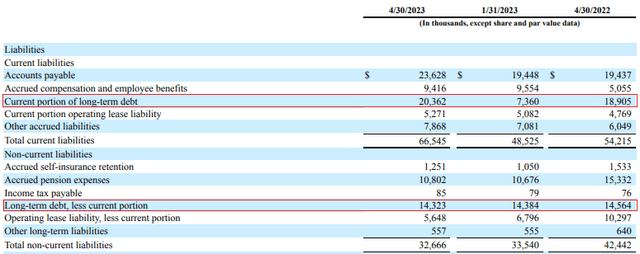

Virco still hasn’t reinstated quarterly dividends (suspended in 2018) despite its improving financial performance and I think the reason behind this could be the higher inventory levels which have pushed up debt significantly. Looking at the balance sheet, the company closed April with inventory levels of more than $18 million higher than a year earlier. This boosted the net debt by $13.4 million quarter on quarter to $34.1 million.

Virco Virco

According to Virco’s Q1 FY24 financial report, the entire increase in the inventory level was attributable to higher quantities as the cost and valuation of the inventory were stable (see page 10 here). The company typically builds and carries significant amounts of inventory ahead of the peak summer season in order to rapidly deliver products to customers in the educational market. Virco said that inventories were higher at the end of April 2023 due to the much better order backlog, the majority of which is scheduled for delivery between June through August.

As of April 30, the order backlog of unshipped sales orders stood at $104.6 million compared to $85.7 million a year earlier (see page 17 here). Considering the order backlog accounts for 44.9% of TTM revenues and financial results during the peak season should benefit from higher gross margins due to recent product price increases, it seems that operating income is likely to grow significantly in Q2 and Q3 FY24. In Q2 and Q3 FY24, Virco recorded an operating income of $19.5 million and I think this year it could surpass $25 million. And as net debt comes down significantly due to decreasing inventories after the peak season, I’m optimistic that the quarterly dividend could be reinstated in late 2023.

Looking at the valuation, Virco has an enterprise value of $102.5 million as of the time of writing, and the TTM EBITDA stands at $18.4 million. This means that the company is trading at 5.6x EV/EBITDA on a TTM basis. Considering the FY24 peak summer season is shaping up to be strong, I think that Virco should be trading at above 9x EV/EBITDA. This translates into $5.99 per share or an upside potential of 41.9%.

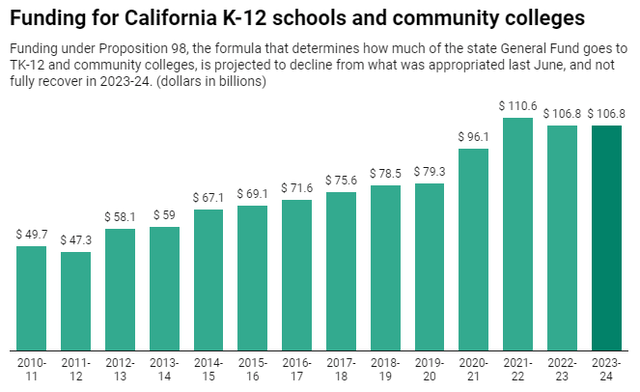

Looking at the risks for the bull case, I think that the major one is that California, Virco’s largest market in terms of revenue, is cutting funding for K-12 schools and community colleges. In May 2023, Gov. Gavin Newsom revealed that he’s budgeting $2 billion less for TK-12 and community colleges for the 2023-2024 fiscal year than he proposed five months before due to falling state revenues.

EdSource

In addition, investors should keep in mind that this is a thinly traded stock, with a daily trading volume rarely exceeding 20,000 shares. There could be significant share price volatility, and it could be challenging to exit a large position.

Investor takeaway

Price increases and diminished international supply chain disruptions enabled Virco to significantly improve its financial results in Q1 FY24 and I expect the strong backlog and high inventory levels to allow the company to book operating income of over $25 million in Q2 and Q3 FY24. This should boost the TTM EBITDA above $23 million, which I expect to become a significant catalyst for the share price. In addition, I expect quarterly dividends to be reinstated in late 2023.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here