Investment Thesis

The Invesco Water Resources ETF (NASDAQ:PHO) has had lackluster returns since my previous article, spending most of the time in the red, and underperforming the S&P 500. It’s safe to say it has been a volatile ride for both bulls and bears. I believe that PHO is now approaching a turning point, where we could see it moving $2-3 higher before resuming the downward trend. While fundamentals have improved slightly, the valuation of a large number of portfolio constituents remains high. I’m still a PHO bear as the combination of expensive valuation and decelerating economic growth historically leads to unfavorable for high-multiple stocks.

About PHO

PHO offers investors exposure to companies that operate within the water resources industry. This exchange-traded fund holds a diversified portfolio of stocks related to water infrastructure, technology, treatment, and distribution.

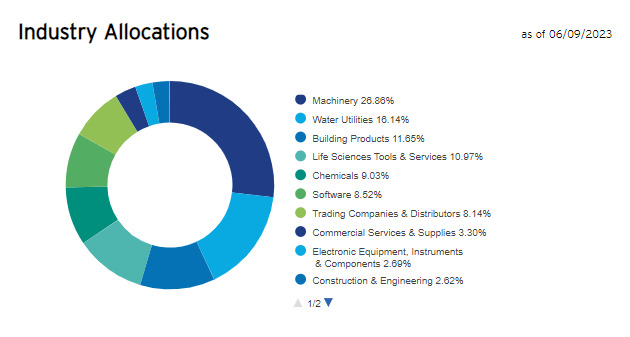

PHO’s holdings encompass various sectors within the water industry. The largest allocation is dedicated to Machinery, followed by Water Utilities and Building Products.

Invesco

The allocation within PHO’s portfolio is designed to capture the diverse aspects of the water resources industry, providing investors with exposure to both utility companies and technology-driven solutions. By investing in PHO, individuals can participate in the growth potential of the global water industry, which is driven by factors such as population growth, urbanization, increasing water scarcity, and the need for improved water infrastructure.

Morningstar

It is important to note that investing in the water resources sector comes with its own set of considerations, including regulatory factors, infrastructure challenges, and potential risks associated with water availability and quality. Therefore, investors should thoroughly research and assess the potential risks and rewards before making investment decisions related to PHO.

A Turbulent Ride For Both Bulls And Bears

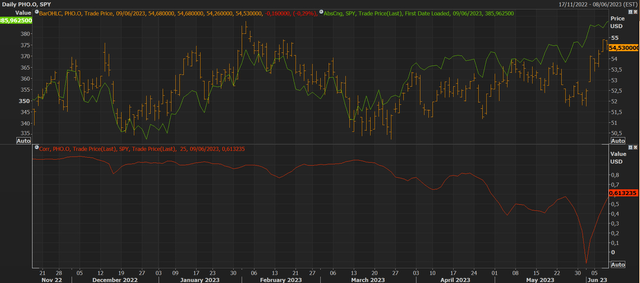

PHO delivered lackluster returns since my previous article, with its performance only up by a mere 41 basis points. Although we are now in positive territory for the bulls, PHO spent most of the time since my last article in the red, experiencing a decline of as much as 7% back in mid-March. It’s safe to say that this has been a wild ride for the bulls as well as for the bears. On a relative basis, it’s worth noting that it has also underperformed the S&P 500 during that time, despite the market being up by a total of 5.3%.

Refinitiv Eikon

Taking a look at the technical indicators, we can observe that the fund has been trading in a range since the start of the year but it’s gradually approaching a turning point, with the Relative Strength Index (RSI) in the 60s and the market price at the upper range of the Bollinger Bands. Since we are not yet in overbought territory, I could see PHO rising toward $56 per share in an attempt to revisit this year’s highs. This would present a favorable opportunity to consider shorting PHO once again.

Refinitiv Eikon

Another noteworthy observation is the breakdown in correlation between PHO and the S&P 500 since my previous article. In the past, the two have typically moved in sync, and each correlation change has been quickly resolved. This leads me to believe that we could witness PHO making an upward move alongside the S&P 500 in the short term followed by a leg down in the mid-term.

Refinitiv Eikon

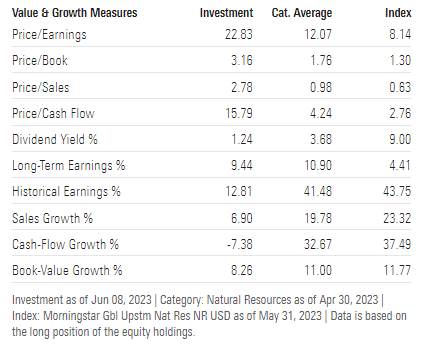

While the fundamentals have slightly improved compared to a couple of months ago, with the price-to-earnings, price-to-book, and price-to-cash flow ratios declining from elevated levels, I still believe that PHO is trading at a relatively high valuation, with a P/E ratio of over 22, a P/B ratio of 3, and a P/CF ratio of 16. In a world where interest rates are at 5%, I believe investors would be better off investing in a one-year Treasury bill rather than allocating their funds to PHO. Furthermore, the fund offers an extremely low dividend yield of 1.2%, and the long-term earnings growth rate has significantly decreased since my previous article, which aligns with expectations of slower economic growth heading into year-end and early 2024.

Morningstar

My perspective on PHO remains unchanged from my previous article, and I still believe that it is a compelling sell. The combination of expensive valuation and decelerating growth has historically yielded unfavorable outcomes for investors, and I see no reason why this time would be any different. Nevertheless, for shorts to truly benefit, we would need to see significant outflows, especially from institutional investors, which I have not observed recently but could occur during a broader market sell-off.

Key Takeaways

Since my last article, PHO has experienced lackluster returns, spending a significant portion of time in negative territory and trailing behind the S&P 500. The market ride has been turbulent for both bullish and bearish investors. In my view, PHO is reaching a critical juncture where we may witness a temporary upward move of $2-3 before the downtrend resumes. Although there has been a slight improvement in fundamentals, the valuations of many holdings remain elevated. Considering the historical pattern, I maintain my bearish stance on PHO, as the combination of lofty valuations and slowing economic growth tends to result in unfavorable outcomes for stocks with high multiples.

Read the full article here