Introduction

As a dividend growth investor, I seek new investment opportunities in income-producing assets. I often add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The sector basic materials sector has always been elusive to me. I previously owned several companies, but they all failed to be consistent dividend growth companies. They were too dependent on the cyclicality of the prices of the basic materials so that even giant like BHP Billiton (BHP) couldn’t increase their dividend steadily. A unique company in that field is Air Products and Chemicals (NYSE:APD), a dividend aristocrat in that field.

Using my methodology for analyzing dividend growth stocks, I will analyze Air Products and Chemicals. I am using the same method to make it easier to compare researched companies. I will examine the company’s fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it’s a good investment.

Seeking Alpha’s company overview shows that:

Air Products and Chemicals provide atmospheric gases, process and specialty gases, equipment, and related services in the Americas, Asia, Europe, the Middle East, India, and internationally. The company produces atmospheric gases, including oxygen, nitrogen, and argon. Process gases, such as hydrogen, helium, carbon dioxide, carbon monoxide, and syngas, specialty gases, and equipment for producing or processing gases comprising air separation units and non-cryogenic generators for customers in various industries.

Fundamentals

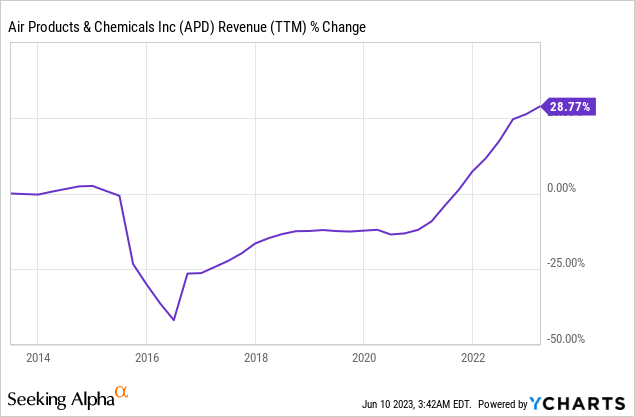

The revenues of Air Products and Chemicals have increased by 29% over the last decade. This figure translates into less than an annual 3% increase. The company constantly reshaped its portfolio by divesting assets and making smart acquisitions to supplement its offering. In the future, as seen on Seeking Alpha, the analyst consensus expects Air Products and Chemicals to keep growing sales at an annual rate of ~7% in the medium term.

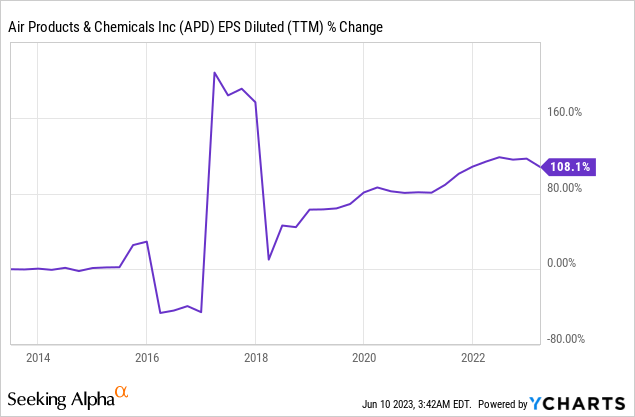

The EPS (earnings per share) has increased significantly over the same period. The company’s EPS increased by 108% over the last decade. EPS is up despite a higher share count, resulting from focusing on the most profitable assets and lowering costs. In the future, as seen on Seeking Alpha, the analyst consensus expects Air Products and Chemicals to keep growing EPS at an annual rate of ~10% in the medium term.

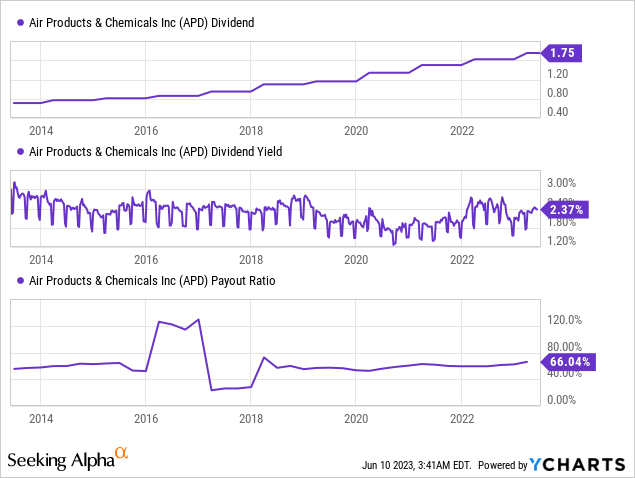

The company is unique in that, despite being a basic materials company. It maintains a healthy dividend growth. The current dividend yield is 2.4%, and the payout seems relatively safe at 66%. The company’s earnings are less volatile than other basic materials companies, making it possible to maintain that payout ratio. Investors should feel secure with a company raising the dividend annually for 40 years.

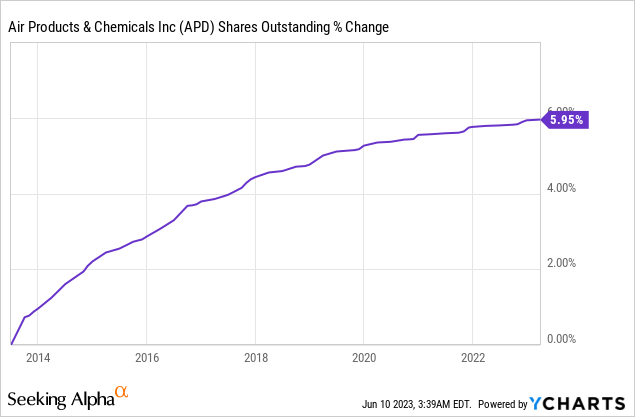

In addition to dividends, companies return capital to shareholders via buybacks. Buybacks support EPS growth as they lower the number of outstanding shares. Over the last decade, the number of shares increased by 6%, meaning that investors were diluted. Buybacks are most efficient when the share price is attractive. Therefore, it makes sense for the company not to buy back aggressively. It simply has to make sure it doesn’t dilute shareholders aggressively.

Valuation

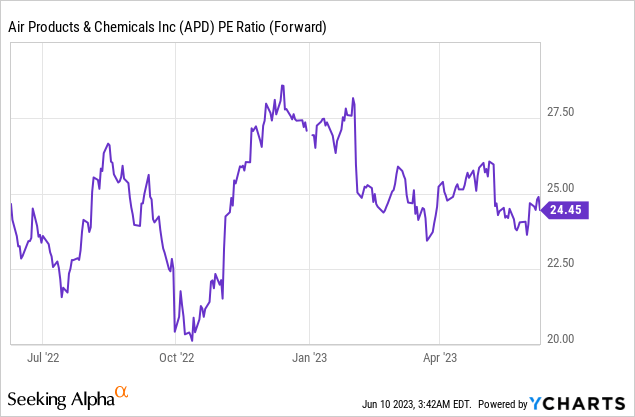

The company’s P/E (price to earnings) stands at 24.5 when considering the 2023 EPS forecast. Paying 24.5 times earnings for a company with decent 10% growth seems a bit high. The company’s valuation is not a bubble but trades for a premium. Over the last twelve months, the company has seen higher valuations, yet despite the valuation being lower than the peak, it is still a bit on the high side.

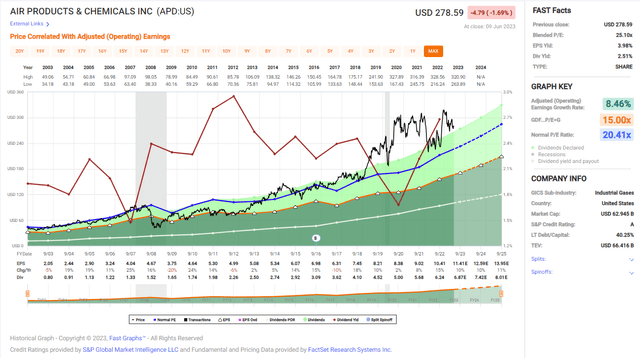

The graph below from Fast Graphs emphasizes that the company is slightly overvalued and trading for a premium. The average P/E ratio of the company over the last two decades was 20.4. The current P/E ratio is more than 20% higher. While the company’s forecasted growth rate is higher than the past growth rate, this is still a significant premium. The company must offer superb growth opportunities and limited risks to justify the current premium.

Fast Graphs

Opportunities

Hydrogen leadership is a crucial growth opportunity. The company today is leading the Gray Hydrogen realm as it produces hydrogen to the company from natural gas. It also aims to be a prominent player in Blue Hydrogen, including carbon capture. It plans to do so by executing its Canada Project & its Louisiana Project. It also plans to lead the Green Hydrogen field, hydrogen made of water and clean energy, by completing its NEOM Project in Saudi Arabia, its NY Project & its Texas Project.

When it comes to Blue Hydrogen, there is a significant need for carbon capture. As natural gas turns into CO2 and hydrogen, there is a need to capture the carbon, so the greenhouse gases won’t reach the atmosphere. The carbon capture technology can also be used as standalone tech to limit pollution. Air Products and Chemicals is a leader in that field with its facility in Port Arthur, Texas, a project described by the Department of Energy as a milestone in its industrial carbon capture and storage program.

The company can also capitalize on its LNG leadership in the medium term. As Russia cut the natural gas supply to Europe in 2022, there is a growing demand for liquified gas. The company can capitalize on it by helping build new LNG infrastructure and to sell the products used for liquefaction and regasification. Moreover, the same infrastructure can later be adapted to carry liquid hydrogen and support the hydrogen transition.

Risks

The first risk is competition. The company plans to shift heavily into hydrogen, carbon capture, and LNG. This is an excellent opportunity for the company to grow, but significant competition exists in that realm. Oil and gas supermajors are also active in hydrogen, LNG, and carbon capture. Companies such as Shell (SHEL) and Equinor (EQNR) will become direct competitors. Air Products and Chemicals is well positioned but still a long-term challenge.

The business environment is a medium-term risk. We see across the globe that interest rates are higher. While the company doesn’t have an enormous debt burden, the higher rates may decrease investments by its clients. The company is involved in massive projects costing billions of USD. With higher rates, financing these projects become more expensive, thus lowering the demand for them.

The margin of safety is the most significant short-term risk for the company. The current valuation means that the company is priced for perfection. Every failure to execute flawlessly, even if the execution is decent, may result in a drop in the share price, which will be harsh for investors who buy at these prices. Usually, buying shares with some margin of safety helps protect investors from short-term volatility.

Conclusions

Air Products and Chemicals is one of the most reliable companies in the basic materials business. The key here is that these materials require processing, giving them some pricing power and room to create uniqueness in the process and cost structure. The company enjoys solid fundamentals and a great management team with decent capital allocation capabilities. They are targeting some fast-growing industries, such as hydrogen and LNG.

However, there are several risks to the thesis. There is competition in the field and a lack of margin of safety. The company is trading for a valuation that I believe to be high, despite a more challenging business environment in terms of interest rates. Therefore, I think the company is a HOLD, which will be interesting, with a P/E ratio of ~20. I also understand investors who buy a tiny position, follow it and add on every dip.

Read the full article here