Headline

Lithium Americas Corp. (NYSE:LAC) is a stock I owned way back in 2015 when they were still listed on the Canadian exchange only. I remembered vividly, governments throughout the world were going to require a certain percentage of vehicles to operate fully electric by certain milestone dates. The potentially high-quality Argentina project at Cauchari-Olaroz was one attraction. The other has always been Thacker Pass Nevada on the border of Oregon. I made a profitable bet and flip without much fundamental analysis.

I became obsessed with the subject to the point where I bought a lithium battery college textbook. Not many in print, I think Amazon (AMZN) charged me about $200. I soon after put down nice-sized bets on Albemarle (ALB) who had just purchased Rockwood Lithium and now had all the rights to the Silver Peak mine, FMC corporation (FMC) who later spun off Livent (LTHM) and Sociedad Quimica y Minera de Chile (SQM).

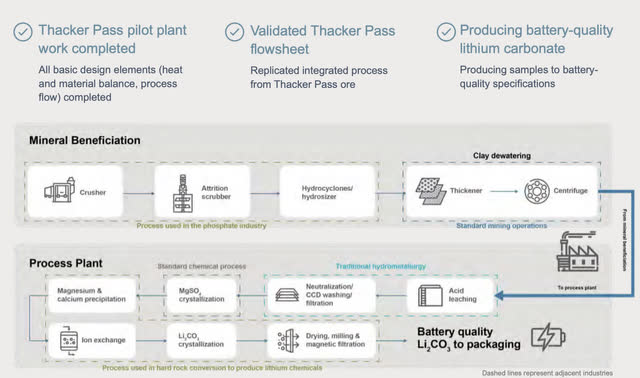

The most interesting catalyst for Lithium Americas is the production start of their Argentina project this month combined with their lithium clay project at Thacker Pass. If they can figure out a way to mine lithium from clay, that process itself may be a patentable product to sell to other operators.

That being said, the prospects of the company are largely unknown. They are currently a cash-burning, pre-revenue share diluting company. Let’s see what they might be worth based on pro-forma presentations and industry comps.

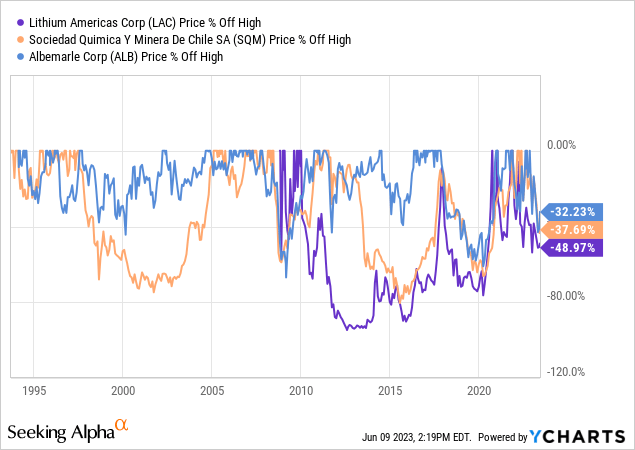

Chart

The entire lithium industry has seen quite a drop off their highs. Lithium Americas is down 10+% more than the already profitable operators.

Story

Lithium Americas Investor Relations

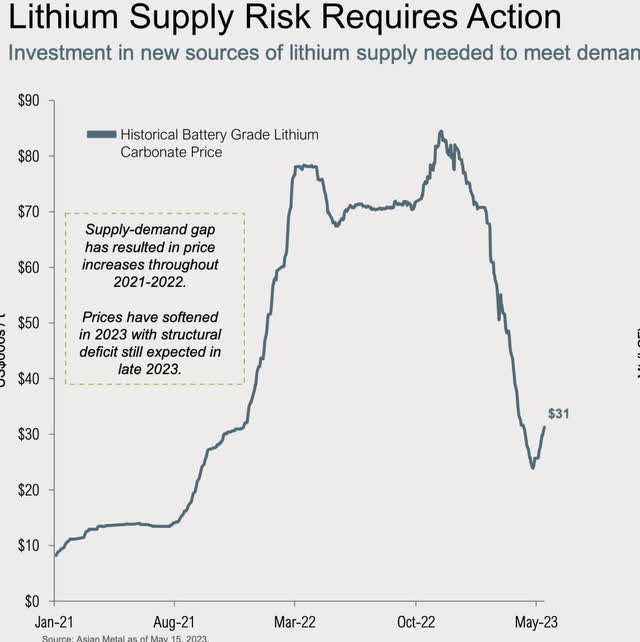

Battery-grade lithium carbonate prices have dipped significantly since 2021-2022. The spike in prices during the Covid era run-up of lithium stocks which attached themselves to the EV momentum have also fallen hard with the price movement of the commodity. I sold my stake in Albemarle right when Covid hit and the P/E exceeded 100X for a long period. They have done a great job of compressing the multiple through execution since then.

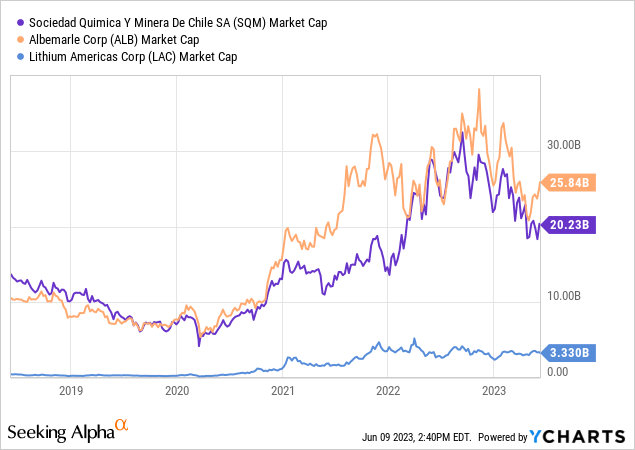

Market caps

One of the main attractions to Lithium Americas is their market cap being only a bit more than a tenth of Albemarle. Per Wikipedia:

The Thacker Pass lithium deposit has measured and indicated resources of 13.7 million tonnes of lithium carbonate equivalent, at an average ore grade of 2,231 ppm (0.22%) lithium. The Thacker Pass volcano-sedimentary deposit is the largest known sedimentary lithium resource in the U.S.[5]

Lithium Americas estimates that the site contains recoverable lithium worth $3.9 billion. It is estimated that enough for batteries for about a million electric vehicles a year could be mined.

If $3.9 billion in lithium could be extracted today, the market is there to snatch it up. That would mean we’d be paying less than 1 X sales for the stock if we project that forward. We have no idea the end cost it will take to set up this refinery, and lithium takes a long time to get to the refining stage in current projects. We also have to consider the cost and conversion of revenue and what kind of margins are possible in a U.S.-based project.

Thacker Pass holdups

Being close to this area, I’ve seen the protests at the Federal building in downtown Reno, demanding the project not go forward due to the desecration of Native American land. It seems like ages ago since those first protests and lawsuits started. Since this project moves and disintegrates earth as part of the mining process versus extracting subterranean brine into evaporation pools, this will be contentious going forward to protect Native American artifacts and local vegetation.

Lithium Americas Investor Relations

I had a friend years ago that was a surveyor for gold miners starting projects in rural Nevada. He had to map out areas of known artifacts plus protected plants and wildlife habitats, certifying a digging approval plan before the projects could even begin to use their mineral rights. Nevada protects the desert more than anyone realizes. This project is going to be difficult to execute regardless of Federal Approvals.

Some roadblocks removed

As per Reuters, some roadblocks for Thacker Pass have been cleared in May 2023:

A federal judge in February rejected claims that the Thacker Pass project would cause unnecessary harm to the environment, but ordered officials to study whether roughly 1,300 acres (530 hectares) at the site where Lithium Americas hopes to store waste rock – a byproduct of the mining process – contained the metal. The ruling is being appealed, although the court has allowed construction to begin.

The judge’s order was linked to an unrelated appeals court ruling that found mining companies do not necessarily have the right under U.S. law to store waste rock on federal land that does not contain valuable minerals.

Of the dozens of mining claims at the Thacker Pass site held by the company, the government found fewer than 10 did not contain lithium mineralization, an Interior Department official told Reuters.

The project, which now has backing from General Motors (GM), will still run into issues of where to put waste and tailings. Even after the process of mining starts, there will be complaints and lawsuits. For those not familiar with the Nevada landscape, Albemarle’s Silver Peak mine is in the south near Las Vegas and Death Valley. Not much-protected anything down there. The North and East of Nevada have indigenous tribes, wildlife, and plants that are protected. This is a whole other ballgame than what Albemarle has to deal with. Not to mention the Albemarle Nevada lobbyist team that has already been established.

Argentina

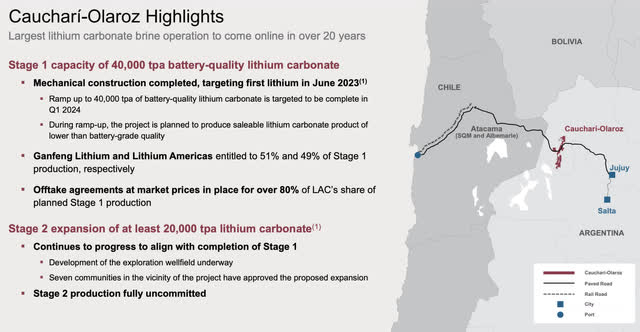

Thacker Pass is both an unproven yet very innovative mining technology and the project’s suboptimal location. Let’s drill down on the Argentina project which should come on line soon:

Lithium Americas Investor Relations

Projections:

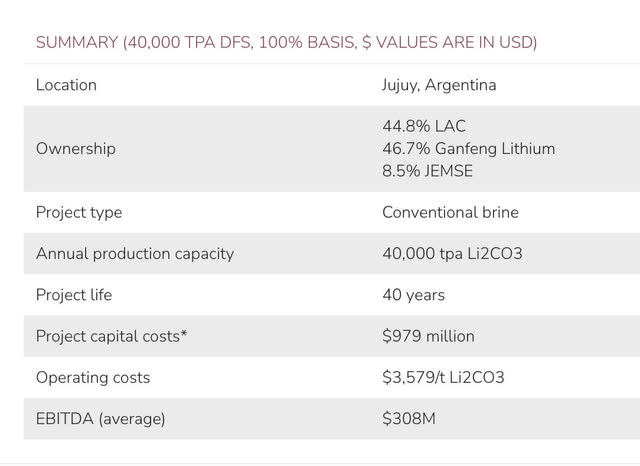

Lithium Americas Investor Relations

With an annual EBITDA average of USD 308 Million and 44% of the project EBITDA being allocated to Lithium Americas, our first EBITDA numbers to draw value from look like USD 135.52 million. This would get us to a price-to-EBIDTA of 24.35 X in the first full year of operation.

If Thacker Pass works

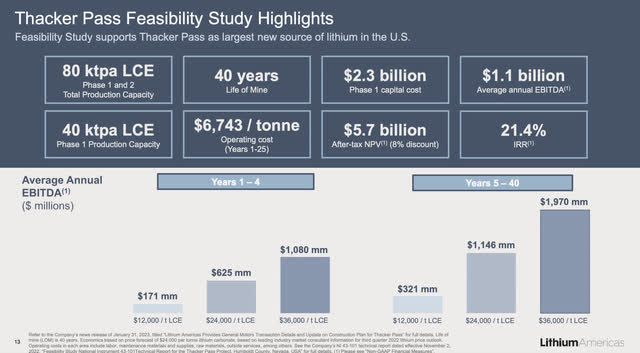

Lithium Americas Investor Relations

Lithium Americas is projecting an average annual EBITDA of $1.1 billion a year based on its own feasibility studies. With these first two projects running at full capacity, that would provide around $1.23 Billion in EBITDA per annum at around year 5 of operation. When year one starts is the main question. If true, we’d be paying about 3 X EBITDA if humming on all cylinders 5 years from now.

EBITDA conversion comps

Let’s take a look at the EBITDA to net income comps for SQM and Albemarle to see what we can expect for net earnings on the bottom line:

Data courtesy of Seeking Alpha:

Numbers in millions

| Company | TTM EBITDA | TTM Net Income | TTM EBITDA Conversion rate |

| SQM | $5,717 | $3,860 | 67.5% |

| Albemarle | $3,667 | $3,675 | 100% |

Average EBITDA to net income conversion of 83.75%

Valuation

Using an owner earnings model popularized in The Warren Buffett Way to find a fair price “if” Lithium Americas executes, we will make the following assumptions:

EBITDA is USD 1.23 Billion, EBITDA to net income conversion average of 83.75% equals $1.030 Billion Net Income.

Lithium Americas also dilutes shares on an annual basis of 12.55% compounded. We will divide our final market cap by 5 years of share compounding assumptions. Shares outstanding today are 159 million, 5 years from now they would be 287 million shares outstanding in this thesis.

Let’s also comp capex and depreciation and amortization as a percentage of net income on our two comps to get our next two variables:

| Company | TTM Net Income | TTM CAPEX | TTM D&A |

| Albemarle | $3,675 | $1445=39.3% | $289 M= 7.8% |

| SQM | $3,860 | $971=25.1% | $227 M=5.8% |

- Average Capex percentage of net income= 32.2%

- Average D&A percentage of net income= 6.8%.

Lithium Americas assumptions based on $1.03 Billion Net Income:

- Capex $329.6 Million

- D&A $70.04 Million.

Owner earnings model all inclusive:

- Net income $1.03 Billion

- Plus D&A $70.04 Million

- Minus $329.6 CAPEX

- Equals owner earnings of $770.44 million

- Discounted at short Risk Free Rate 5.2% = $14.816 Billion Market Cap

- Divided by shares 287 million projected shares outstanding = $51.62/share.

Without Thacker Pass:

- $135.52 Million X EBITDA conversion rate of 83.75%=$113 million net income

- Plus D&A $7.17 Million

- Minus $36.38 Million

- Equals owner earnings of $83.79 million

- Discounted at short Risk Free Rate 5.2% = $1.61 Billion fair market cap

- Divided by 287 million projected shares outstanding = $5.6/share.

Growth outlook

This whole investment is based on the success of Thacker Pass. I want it to work, but I am a skeptic having seen what the Nevada bureaucracies put mining companies through. I wouldn’t expect this clay mining extraction to get up and running as quickly as the Pro-forma assumes. If it does, I would expect the market to overshoot my bull case of $51. I wouldn’t expect it to get to $5.5 if Thacker gets caught up in red tape longer. The asset has plenty of value, even oil companies like Exxon Mobil (XOM) are now buying up lithium projects.

However, if only Argentina works out, I would assume a flat to down share price for the foreseeable future.

Summary

Place your bets on Thacker Pass. To me, investing in SQM or Albemarle make more sense, as they have already gone through a lot of hardship to get where they are. I feel the difficulty of the lithium mining process is far under-appreciated. Lithium Americas Corp. is a hold unless a breakthrough occurs at Thacker Pass.

Read the full article here