Golden Ocean Group’s logo (Golden Ocean Group)

Investment Thesis

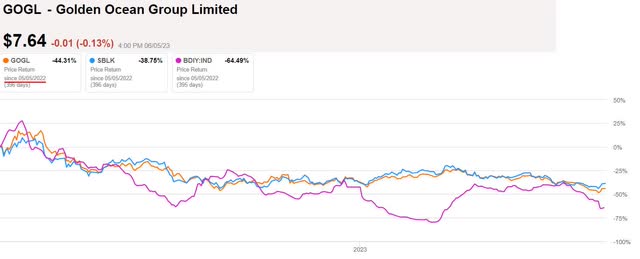

It has been a little over a year since we claimed that it did look like the stars were aligning for Golden Ocean Group (NASDAQ:GOGL). We even took the plunge and upgraded it from a Hold to a Buy.

The share price is down 43% since, which is somewhat more than the 39% that their peer Star Bulk Carriers (SBLK) share price dropped.

GOGL versus SBLK and the BDI (SA)

Our Buy call was not well-timed, as one would certainly have gotten a much better entry price if one waited. To our defense, we, nor anyone else, knows when the market peaks or bottoms.

Let us first look at their latest financial performance, followed by potential business prospects going forward. After all, we are investing for the future, not the past.

Financial Results in Q1 of 2023

GOGL achieved an average TCE rate for the fleet of $14,929 per day in Q1 of 2023. In comparison, this is quite similar to the average TCE rate for SBLK’s fleet of $14,199 per day in the same period.

In terms of net cash from the operation, GOGL made $76.5 million, whilst SBLK made a higher amount of $83.2 million. This can be explained by the fact that SBLK does have a larger fleet of 132 vessels, which is reflected in a $28 million higher revenue.

Despite GOGL having a smaller fleet, of 78 owned vessels and 9 chartered in, they still paid out more in finance costs in Q1 than GOGL had to do, as they are more leveraged.

GOGL had net interest expenses of $20.5 million, against SBLK’s $12.6 million.

GOGL does have a net long-term debt of $985.9 million on a fleet that is valued at $2,693 million. SBLK has a net long-term debt of $789.1 million on a fleet valued at $2,818 million.

Both companies do have ample cash and liquidity at this moment.

GOGL’s fleet is also very modern, with an average age of just 6.7 years old. The average age of SBLK’s fleet is 10.7 years old.

Both of these two companies do need to regularly renew their fleet. GOGL have mostly chosen to buy new vessels, while it is quite interesting to note that SBLK is going down the route of chartering in some new vessels as they want to gain more clarity around the preferred propulsion systems before they order any newbuildings.

During Q1 this year, GOGL did purchase 6 modern Newcastlemax vessels and took delivery of the first of 10 Kamsarmax newbuildings under construction.

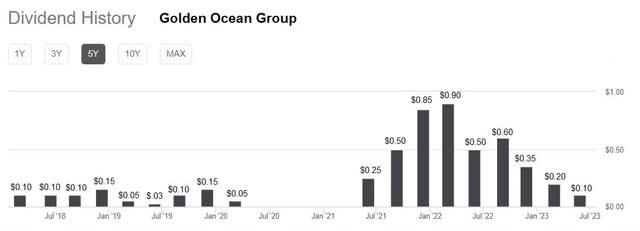

Dividend and Share Buyback

We keep reminding our readers that shipowners that rely predominantly on the spot market, such as GOGL and SBLK, have to live with gyrating earnings because it is very cyclical. This is in stark contrast to SFL Corporation (SFL) which has long-term charters on their vessels. Eight of their Capesize ships are on long-term charters to GOGL, all coming off charter in Q3 of 2025.

Both GOGL and SBLK have a policy of distributing most of their free cash flow back to shareholders as dividends. As such, this is going to vary greatly from quarter to quarter. There will be no dividend safety. There is nothing wrong with that, as long as you are aware of it and willing to take what the market gives you.

GOGL’s 5-year dividend history (SA)

Their 5-year dividend history clearly points to what we just described.

GOGL did buy back 62,085 shares under it in Q1 of 2023 at the value of approximately $0.5 million. As of the end of Q1, they have repurchased a total of 462,085 shares under its share buy-back program.

This program started on October 4, 2022, and authorized the company to buy back shares of a maximum of $100 million for a period of up to 12 months at a maximum share price of USD 10, or equivalent in NOK for shares acquired at the Oslo Stock Exchange.

Business Prospects

We just pointed out that GOGL is quite reliant upon the spot market.

However, they did have some coverage as of the end of Q1, with 26% of total days for the Capesize vessels covered at an average rate of $22,300 per day and 38% for Panamax vessels at an average rate of $19,600 per day. Typically, such coverage can be for 3 to 5 months.

As long as the Baltic Dry Index stays above 1,000 there should be no concern that GOGL will not make money.

The Baltic Dry Index 5-year chart as of 5th June 2023 (CNBC)

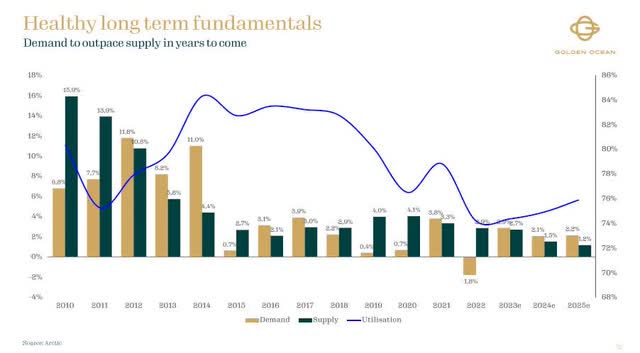

The supply and demand dynamics do look promising if we look toward the next 24 months.

Healthy long-term fundamentals for the Dry Bulk market (Golden Ocean Group’s Q1 2023 Presentation)

Risks to Thesis and Conclusion

Coal demand from China and India has been good with heatwaves hitting both countries and import of coal was high, However, demand for steel has been low and iron ore shipments are the most important commodity for Capesize vessels. There is a risk that the demand for steel in China is not going to reach its target volume in 2023. According to an article in S&P Global China’s National Development and Reform Commission has been soliciting opinions from major Chinese steel mills on details of the 2023 crude steel output cuts.

Our opinion is that the Chinese government will come out with more stimulus measures to revitalize the real estate market, as this is very important for the overall economy there.

We would like to remind you what we wrote in our previous analysis on GOGL where we stated:

Indeed, despite a possible slowdown in the world’s economies, I believe the stars are aligned, as their management said earlier, for a multi-year period of generous returns both to the company and its shareholders.”

Herein lies the conundrum. Things can get worse before it gets better. Is the share price of GOGL going to continue to go down, or is it now just an even better time to buy than when we last had a Buy stance?

We can only look at the present fundamentals and future expected supply and demand. From this, we continue to stick our neck out with a Buy stance for both GOGL and SBLK.

Read the full article here