A Quick Take On SelectQuote

SelectQuote, Inc. (NYSE:SLQT) reported its FQ3 2023 financial results on May 10, 2023, beating both revenue and earnings consensus estimates.

The firm operates a group of insurance exchanges of Medicare Advantage, home, auto and life insurance services.

SelectQuote, Inc. may have seen the worst of its troubles in recent periods, but I’m still not convinced the stock is a Buy yet, although it is worth putting on a watch list.

I’m therefore Neutral [Hold] for SLQT stock until the company shows that it can consistently produce profitable growth.

SelectQuote Overview

Overland Park, Kansas-based SelectQuote was founded to provide insurance companies of many types with leads for consumers interested in purchasing various types of insurance coverage.

The company generates revenue via commissions through first-year and renewal commission agreements with insurance carriers.

Management is headed by Chief Executive Officer Mr. Tim Danker, who has been with the firm since 2012 and was previously founder and CEO of Spring Venture Group, a senior healthcare insurance distribution site.

The company markets its online service via online and offline marketing channels primarily in a direct-to-consumer [DTC] approach.

Its primary channels include television, radio, third-party marketing services and search engine placement.

According to a 2018 market research report by IBISWorld, the market for online insurance brokering in the U.S. is estimated to rise to $18.1 billion by 2024.

This represents a forecast 9.3% from 2019 to 2024.

The main drivers for this expected growth are improvement in online-based lead generation, capitalization and risk management technologies.

Additionally, disposable income growth will also add to consumer demand as will increased awareness of efficiencies to be gained by buyers and sellers operating in an online environment.

SLQT’s Recent Financial Trends

-

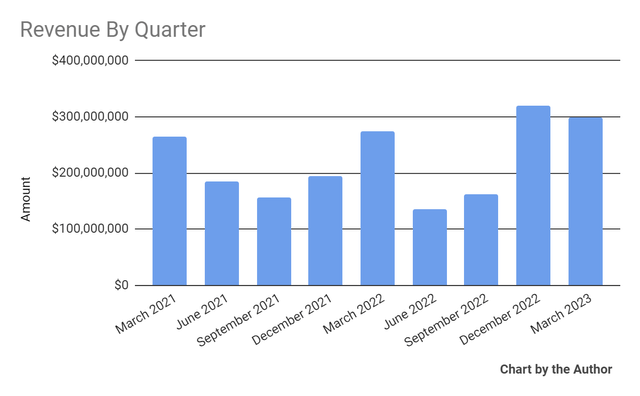

Total revenue by quarter has begun growing more robustly again recently:

Total Revenue (Seeking Alpha)

-

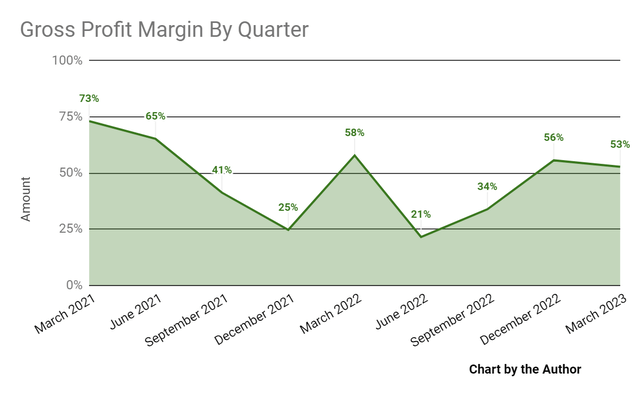

Gross profit margin by quarter has produced no discernible trend:

Gross Profit Margin (Seeking Alpha)

-

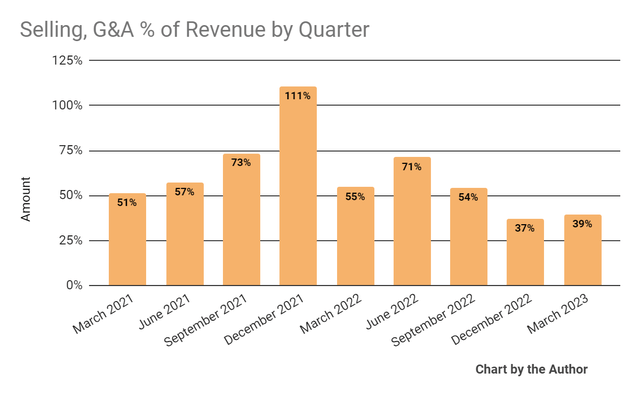

Selling, G&A expenses as a percentage of total revenue by quarter have trended materially lower in recent quarters:

Selling, G&A % Of Revenue (Seeking Alpha)

-

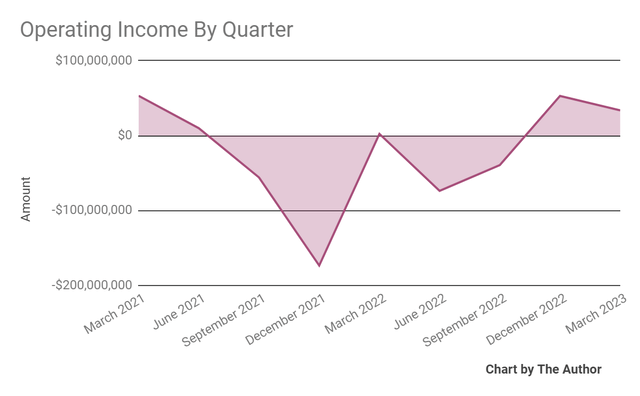

Operating income by quarter has turned positive recently:

Operating Income (Seeking Alpha)

-

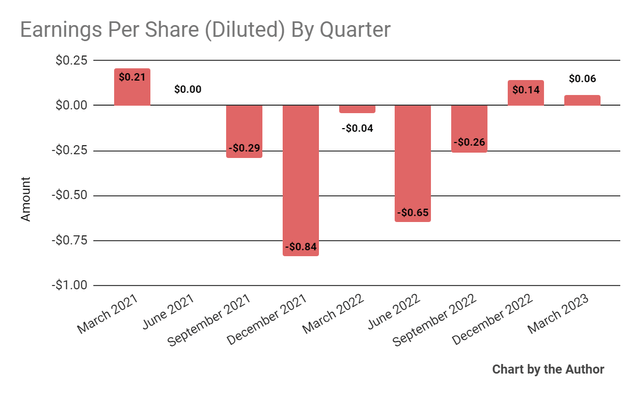

Earnings per share (Diluted) have also remained positive in the last two quarters:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

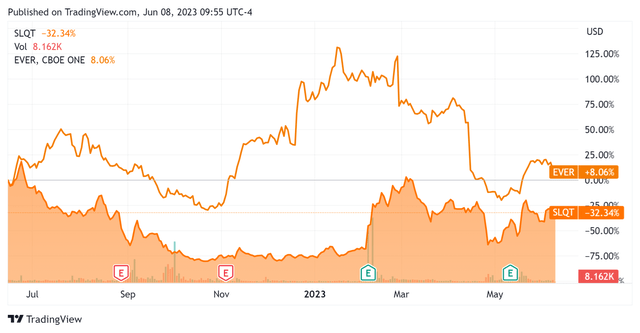

In the past 12 months, SLQT’s stock price has fallen 32.34% vs. that of EverQuote, Inc.’s (EVER) rise of 8.06%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $92.0 million in cash and equivalents and $692.7 million in total debt, of which $25.4 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was ($68.1 million), of which capital expenditures accounted for $1.3 million. The company paid $9.3 million in stock-based compensation (“SBC”) in the last four quarters, the highest trailing twelve-month figure in the last ten-quarter period.

Valuation And Other Metrics For SLQT

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.0 |

|

Enterprise Value / EBITDA |

NM |

|

Price / Sales |

0.4 |

|

Revenue Growth Rate |

13.8% |

|

Net Income Margin |

-12.5% |

|

EBITDA % |

-0.4% |

|

Net Debt To Annual EBITDA |

-171.6 |

|

Market Capitalization |

$321,650,000 |

|

Enterprise Value |

$958,870,000 |

|

Operating Cash Flow |

-$66,790,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.71 |

(Source – Seeking Alpha.)

As a reference, a relevant partial public comparable would be EverQuote; shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

EverQuote |

SelectQuote |

Variance |

|

Enterprise Value / Sales |

0.7 |

1.0 |

48.6% |

|

Enterprise Value / EBITDA |

NM |

NM |

–% |

|

Revenue Growth Rate |

-5.3% |

13.8% |

–% |

|

Net Income Margin |

-5.3% |

-12.5% |

138.0% |

|

Operating Cash Flow |

-$13,180,000 |

-$66,790,000 |

406.8% |

(Source – Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

SLQT’s most recent Rule of 40 calculation was 13.4% as of FQ3 2023’s results, so the firm is in need of improvement in this regard, per the table below:

|

Rule of 40 Performance |

Calculation |

|

Recent Rev. Growth % |

13.8% |

|

EBITDA % |

-0.4% |

|

Total |

13.4% |

(Source – Seeking Alpha.)

Commentary On SelectQuote

In its last earnings call (Source – Seeking Alpha), covering FQ3 2023’s results, management highlighted the growth in its Medicare Advantage lifetime value and a reduction in both the operating and marketing expenses per policy.

Its Life, Auto & Home segments produced adjusted EBITDA, though revenue was largely unchanged and still a small part of the total.

The firm’s SelectRx membership continued to grow along with revenue growth and a reduction in adjusted EBITDA loss for this segment.

Total revenue for FQ3 2023 rose 9.2% YoY but gross profit margin declined by 5.1%.

Selling, G&A expenses as a percentage of revenue dropped by 15.3 percentage points YoY, a very positive signal, and operating income remained substantially positive.

Looking ahead, management raised its full-year topline revenue guidance, which, if achieved, would generate revenue growth of approximately 25.5% at the midpoint of the guidance range.

The company’s financial position needs improvement, with limited liquidity, material debt and free cash use.

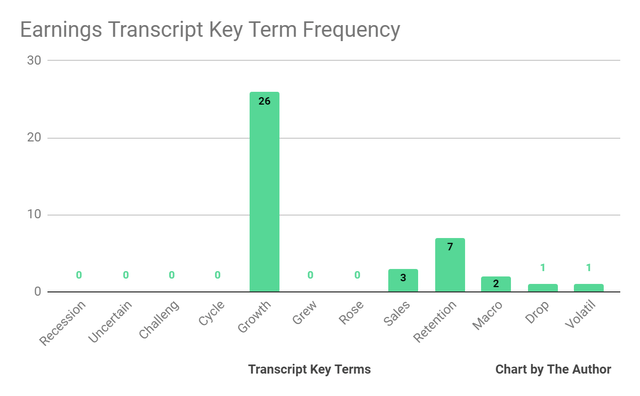

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited “Macro” two times, “Drop” once and “Volatil[e][ity]” once.

The negative terms refer to the volatility of the firm’s financials in recent periods and management’s work to smooth out those fluctuations.

In May, a number of company Directors purchased stock in what appeared to be a coordinated effort to show their support.

In the past twelve months, the firm’s EV/Sales valuation multiple has dropped approximately 19.5%, as the chart from Seeking Alpha shows below:

EV/Sales Multiple History (Seeking Alpha)

A potential upside catalyst to the stock could include the company’s improved unit economics and a period of negative results.

Management has changed its focus from growth to profitability, and those efforts have started to show results.

The primary risks to the company’s outlook would be a negative calendar Q4 enrollment period or poor agent productivity, but management doesn’t seem overly concerned about those risks.

SLQT may have seen the worst of its troubles in recent periods, but I’m still not convinced the stock is a Buy yet.

I’m therefore Neutral [Hold] for SelectQuote, Inc. stock until the company shows that it can consistently produce profitable growth.

Read the full article here