Introduction

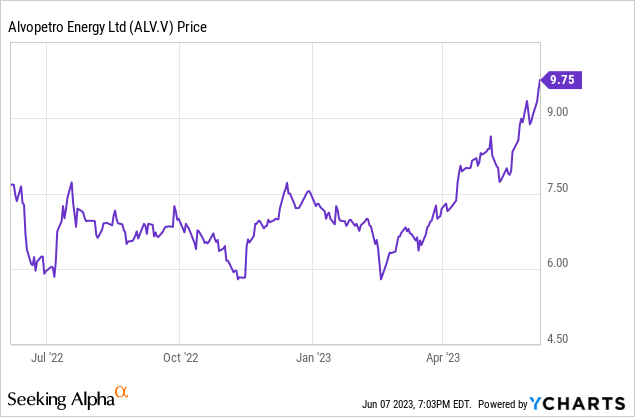

Alvopetro Energy Ltd. (OTCQX:ALVOF, TSXV:ALV:CA) has been in an enviable position, as the natural gas price it receives from Bahiagas, its offtake partner, depends on foreign natural gas and oil prices. The company has been selling its natural gas output at the contractual ceiling price, but a prolonged period of lower natural gas and oil prices on the futures market has reduced the visibility. The stock is up about 40% since my previous article was published so I wanted to check up on the company’s performance.

Q1 was again great, and the current price environment will last for two more years

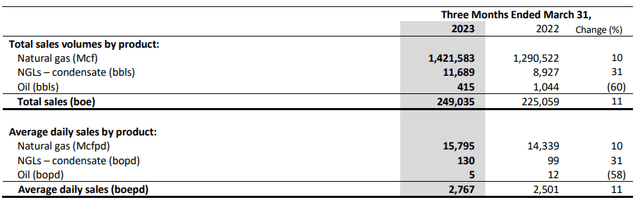

Alvopetro is a relatively small producer. In the first quarter of this year, the company produced just under 2,800 barrels of oil-equivalent per day. Although the output is measured in oil-equivalent barrels, there’s virtually no oil (as you can see below, the total oil production was less than 0.2% of the oil-equivalent production), and the majority of the output comes from the production and sale of natural gas.

Alvopetro Investor Relations

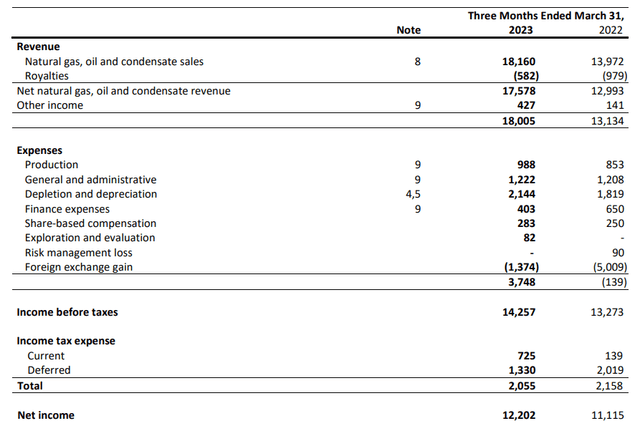

The average received price was just over US$12 per Mcf of natural gas. A very strong realized price, as the sales price is established based on a mix of the Brent oil price, the Henry Hub and the UK National Balancing gas prices with a floor and a ceiling. As I’ll explain later in this article, the current prices are above the ceiling level, so Alvopetro receives the ceiling price which is currently US$12.06/Mcf (the ceiling price increases by 3% for inflation this year, and 2% in the subsequent few years).

The decent output and strong prices resulted in a total revenue of $18.2M, and the total revenue (after deducting royalty payments and adding back the “other income” (mainly interest income and tax recoveries) was $18M.

Alvopetro Investor Relations

As you can see in the image above, the total production costs are exceptionally low: to generate north of $18M in revenue, the total production costs are just $1M. And there are virtually no transportation expenses, as the gas fields are directly connected to the pipeline system used by Bahiagas, which buys the natural gas from Alvopetro.

This means all operating expenses remain very low, and the company reported a net income of US$12.2M. With 36.5M shares outstanding, the EPS in Q1 was US$0.33, which is almost C$0.45. And that’s pretty high for a stock that is still only trading at just over C$9.

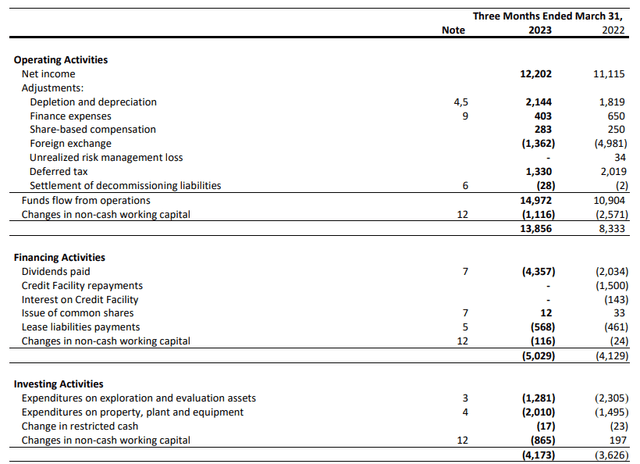

Of course, Alvopetro continues to invest in exploration and new wells. But the total capex in Q1 was pretty low. As you can see below, the total operating cash flow before changes in the working capital position was approximately $15M and roughly $14.4M after deducting the lease payments.

Alvopetro Investor Relations

The total capex was just $3.3M, resulting in a net free cash flow result of $11.1M. That’s slightly lower than the reported net income because the total capex was higher than the combined depreciation and amortization expenses.

The strong cash flow meant the company ended the first quarter with zero debt and about $25M in cash. This means the total cash pile is now approaching C$1/share again and this provides a nice cushion. And Alvopetro is obviously still paying its rather generous dividend payment. The current quarterly dividend is US$0.14 per share, which works out to $0.56 per year, and at the current exchange rate that’s approximately C$0.75 per share. The stock is now trading considerably higher compared to where it was when I published the previous article, but the dividend yield is still a very appealing 7.7%.

One of the comments on the previous article was that the oil and gas prices were decreasing and, therefore, the average received price by Alvopetro will decrease as well. While that is in theory correct, there are two important elements here.

First of all, Alvopetro firms up the price in six months, so there is some short-term visibility when it comes to the realized prices.

Secondly, the natural gas price it receives from Bahiagas (the offtaker) is determined based on a blend of the Henry Hub, UK National Balancing gas price and the Brent oil price. Unfortunately, the company does not disclose the exact formula/breakdown, so I’m not 100% sure what the recent decrease in the Henry Hub and Brent oil price means for the company.

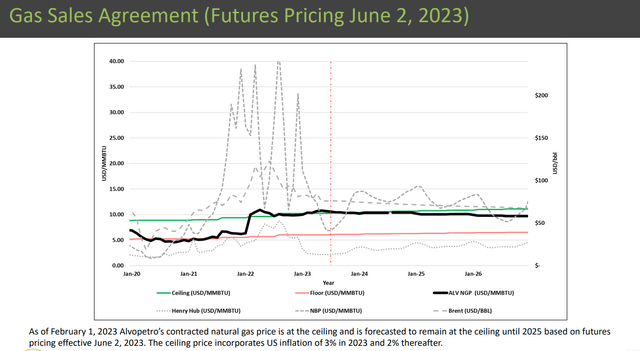

Fortunately, Alvopetro publishes an important chart where it clearly shows the minimum and maximum price, and where the footnote usually offers a little bit of guidance. Back in February, Alvopetro mentioned that based on the prices on the futures market, it expected to remain at the ceiling price level until 2027.

Alvopetro Investor Relations

This has now changed. If you have a closer look at the image above, you’ll see the futures market has gotten weaker as well. Based on the current situation, Alvopetro expects to remain above the ceiling price until 2025. While that still provides excellent visibility for the next 18-24 months, the inconvenient truth is that the received price may fall below the ceiling price two years earlier than what was anticipated and expected just four months ago.

Investment thesis

The main reason why I found Alvopetro Energy to be very attractive was its generous dividend and the pretty good visibility until 2027. The quarterly dividend payments are still nice but the higher share price means the yield has decreased. Additionally, prolonged weakness in the oil and natural gas prices have further reduced the “runway” until when the realized price may dip below the ceiling price which means the cash flows will likely decrease unless it will be mitigated by higher production volumes (new well 197(1) started producing at the end of May).

The Q1 free cash flow was very strong but keep in mind the total capex commitment for this year is still substantially higher than the Q1 capex. And add the fact that the April and May production volumes came in substantially lower than the Q1 volumes due to the lower demand from Bahiagas, and I expect the Q2 results to be pretty weak.

For those reasons, I am moving Alvopetro to a “sell” and it might be wise to lock in the 40% capital gain since my previous article was published in March while the total return is +124% since my initial article from December 2021. Perhaps a new buying opportunity will come along in the near future, but it could make sense to rotate into other natural gas producers. I tip my hat to the execution of the Alvopetro management, but I think it’s time to move to the sidelines here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here