I have mentioned in several articles about different banks, that I hardly own any banking stocks right now. To be even more precise: there is only one bank in my portfolio – Svenska Handelsbanken (OTCPK:SVNLF) from Sweden. In my other articles about different banks (see here and here for example), I always was very reluctant to open a position although some stocks seem extremely cheap (for example when looking at P/E ratios).

Svenska Handelsbanken is the exception and a position I will continue to hold. And it is not that Svenska Handelsbanken is not facing any risks or that Sweden (or the other Scandinavian countries in which the bank mostly operates) are not facing the risk of a potential recession. Svenska Handelsbanken has an excellent track record of being very risk-averse and has a disciplined risk management. But checking on all the positions in a portfolio from time to time is appropriate and therefore let’s take another look at Svenska Handelsbanken.

(Note: When talking about share information, I am talking about the A share – in my first article I briefly talk about the different types of shares)

Quarterly Results

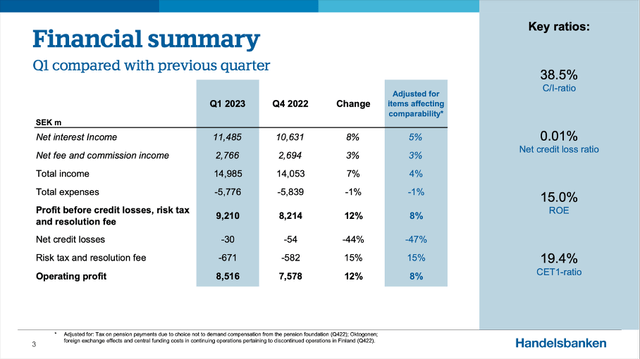

Similar to many banks in the United States or Canada, Svenska Handelsbanken could report great results for the first quarter of fiscal 2023. For starters, net interest income increased 43.3% year-over-year from SEK 8,014 million in Q1/22 to SEK 11,485 million in Q1/23. Total income also increased from SEK 12,323 million in Q1/22 to SEK 14,985 million in Q1/23 – resulting in 21.6% year-over-year growth. Operating profit also increased from SEK 6,624 million in Q1/22 to SEK 8,516 million in Q1/23 – a 28.6% YoY growth. And finally, diluted earnings per share increased 19.9% from SEK 2.87 in Q1/22 to SEK 3.44 in Q1/23.

Handelsbanken Q1/23 Presentation

Additionally, return on equity could improve from 13.6% in the same quarter last year to 15.0% in the first quarter of fiscal 2023.

Cost Control

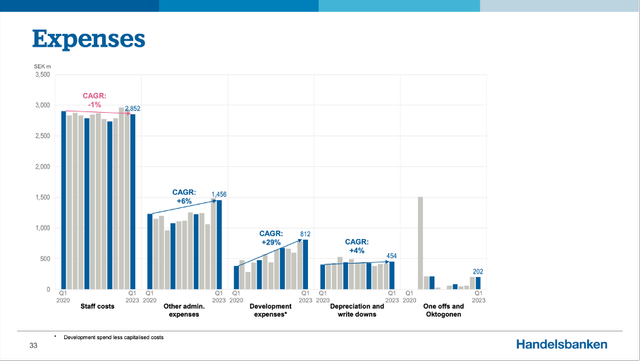

Aside from higher interest rates, which are leading to higher net interest income for almost all banks around the world, Svenska Handelsbanken is also trying to lower its expenses and therefore improve the bottom line (also a strategy we saw quite often in the last few years). And in the last twelve months, the total number of branches declined from 511 in Q1/22 to 439 in Q1/23, which is mostly the result of Svenska Handelsbanken divesting its Finland and Denmark business, which also led to a lower number of employees. But for the remaining branches and countries in which the bank is still operating, the number of employees increased from 10,743 (average in Q1/22) to 11,331 (average in Q1/23).

Handelsbanken Q1/23 Presentation

Overall, Svenska Handelsbanken could keep staff costs stable (they actually declined a little bit) over the last few quarters, which is a good sign. Other expenses increased, but as staff expenses by far exceed all other expenses, it makes sense for the bank to focus on these expenses. Of course, Svenska Handelsbanken has interest expenses as every other bank, but these expenses are much harder to control.

Risk-Averse Bank

But the top- and bottom-line growth and performance metrics are only one part of the picture. Especially when talking about banks we also must look at financial stability metrics and the last few months have demonstrated why this is important.

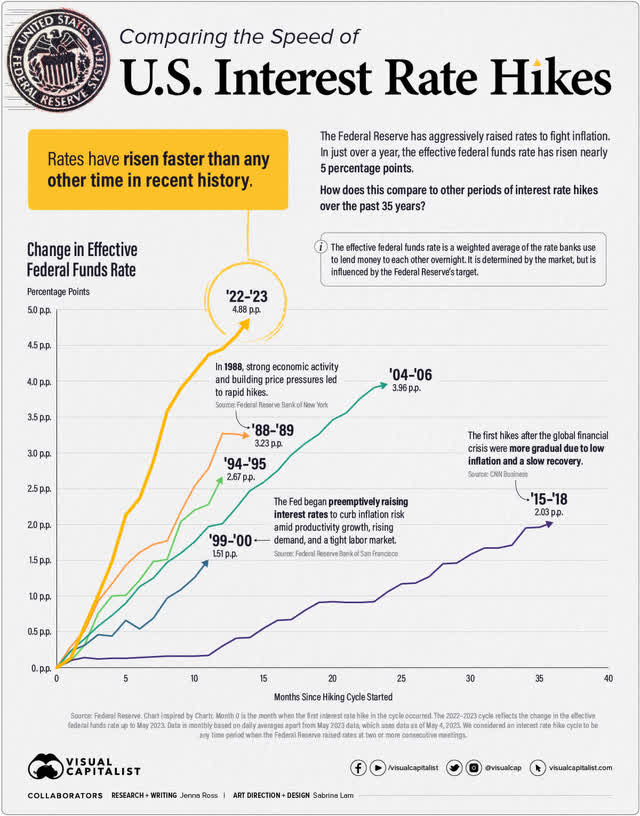

When talking about risk, we can start by looking over the pond at the Federal Reserve and why we witnessed bank failures in the United in the last few months. I am certainly not belonging to those seeing the risk of a banking crisis contained or seeing the collapse of Signature Bank or Silicon Valley Bank as outliers or isolated incidents. Nevertheless, we can clearly identify a major problem that contributed to the collapse – the speed of the U.S. interest rate hikes by the Federal Reserve.

Visual Capitalist

Since the early 1980s, this has been the fastest pace by which the Federal Reserve has increased interest rates. In a little more than one year the Fed has raised the Federal Funds rate almost 500 basis points. In comparison, the Swedish Central bank also increased interest rates, but with a slower pace: From 0.25% in mid 2022, the interest rate was increased to 3.00% right now. And this more moderate pace will lower the risk for banks also collapsing in Sweden.

However, for Svenska Handelsbanken the risk to collapse in a similar scenario as the Silicon Valley Bank collapsed (having billions of low yield bonds which are suddenly worth less in an environment with higher interest rates) is unlikely as the biggest part of Svenska Handelsbanken’s assets is not in bonds.

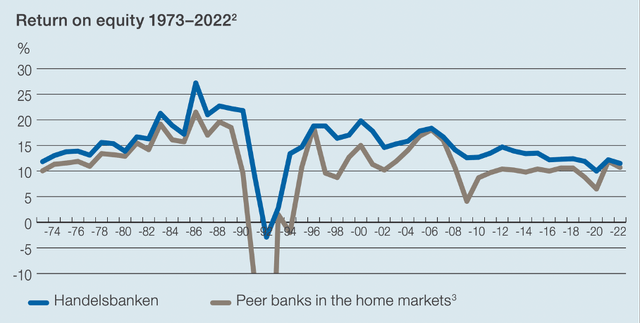

Aside from the lower pace of interest rate hikes in Europe, Svenska Handelsbanken always was risk-averse and always weathered economic storms quite well (it only struggled in the early 1990s when Sweden was hit by a severe recession). And this is visible in most metrics.

Handelsbanken Q1/23 Presentation

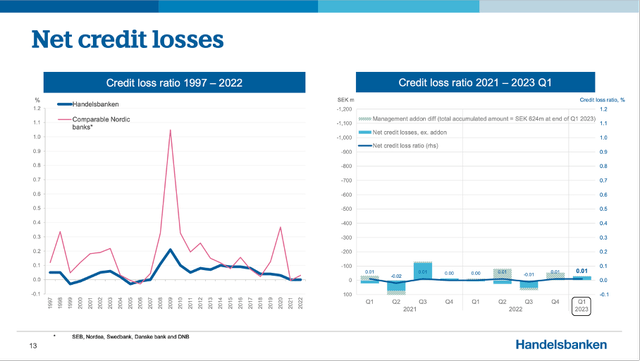

For starters, the credit loss ratio in the first quarter of fiscal 2023 was 0.01% – lower than its Nordic peers and no comparison to most banks in the United States. Additionally, Svenska Handelsbanken has a common equity tier 1 ratio of 19.4% (increased from 18.7% one year earlier) – a metrics almost all U.S. banks can only dream of and even when comparing it to Canadian banks or Australian banks a CET 1 close to 20% can be called outstanding.

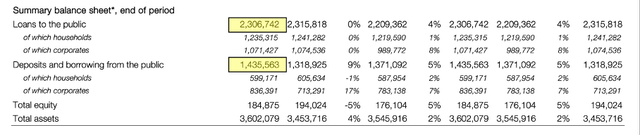

In my other articles about banks – mostly U.S. banks and Canadian banks – I also looked at the loan-to-deposit ratio as well as the loan-to-asset ratio as two metrics for the financial stability of a bank. I must admit I had some difficulties to find the accurate numbers in the reports. While total assets (SEK 3,602 billion) were easy to identify, the total deposits and total loans were rather difficult to find out (contradicting numbers in reports and presentations). But when looking at the end-of period numbers, total deposits were SEK 1,436 billion and total loans were SEK 2,307 billion (in my opinion).

Svenska Handelsbanken Q1/23 Earnings Release

When calculating with these numbers we get a loan-to-asset ratio of 0.64 and a loan-to-deposit ratio of 1.61. And while the loan-to-asset ratio can still be seen as acceptable (usually, a loan-to-asset ratio should be below 0.6), the loan-to-deposit ratio is not what we like to see and could be potentially a red flag.

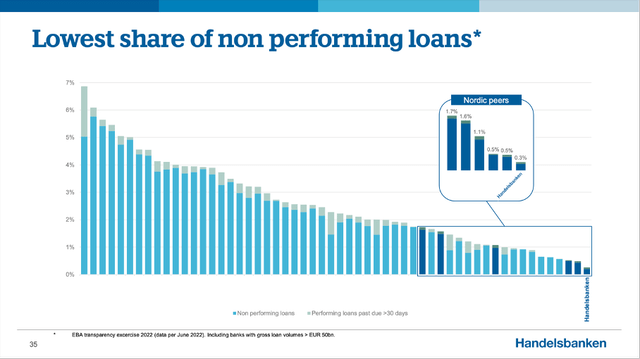

But Svenska Handelsbanken being such a risk-averse business, I don’t see it as problematic. I already mentioned the low credit loss ratio of Svenska Handelsbanken above. And the major reason for that low ratio is the “church spire principle” – management is basically demanding that every branch manager should be able to see all the customers from the steeple. Or to put it differently: Branch managers should know their own customers extremely well, which will minimize the risk of lending to people which are not credit worthy. As result, it is not surprising that Svenska Handelsbanken has a very low rate of non-performing loans.

Handelsbanken Q1/23 Presentation

In the last few years, Svenska Handelsbanken closed about half of its branches in Sweden, which is undermining the “church spire principle” a bit. But it is more a risk management principle to live by and even with half the branches, the bank can remain risk-averse and take a close look before lending – and maybe rather pass up on the opportunity to make another loan. When looking at the numbers over time and comparing Svenska Handelsbanken to its peers we can see the focus of Svenska Handelsbanken on its risk averse principle paying off.

Dividend

In the end, Svenska Handelsbanken is not an investment to expect excessive profits. But it is an investment that will literally pay dividends. In fiscal 2022, Svenska Handelsbanken was paying a total dividend of SEK 8.00 resulting in a current dividend yield of 9.3%. Of course, we must point out that the ordinary dividend was “only” SEK 5.50 (which is still resulting in a dividend yield of 6.4%) and SEK 2.50 was a special dividend.

But Svenska Handelsbanken increased its ordinary dividend from SEK 5.00 in fiscal 2021 to SEK 5.50 in fiscal 2022 and reached pre-crisis levels again (it already paid a dividend of SEK 5.50 in 2019 for fiscal 2018). And considering earnings per share of SEK 10.84 in fiscal 2022, the ordinary dividend of SEK 5.50 is well covered. Considering the challenging environment, we are in right now, I would not bet on dividend increases in the years to come and we could also face the risk of the dividend being suspended again for one year.

Conclusion

It is not surprising that Svenska Handelsbanken also lost about 25% in value in the last few months – many banking stocks (especially regional banks in the United States) declined much more. And I don’t want to rule out further downside risks in the coming months and quarters (however, I see the stock well supported around SEK 70), but Svenska Handelsbanken remains a hold for me. It might actually be one of the few banks where I see it being a possibility to add to my position in the coming months as I see the risk of default or severe troubles as very low. Additionally, with interest rates probably increasing further in Europe in the coming months, Svenska Handelsbanken might report good results for fiscal 2023 with even higher earnings per share than in fiscal 2022.

Of course, we must expect lower interest rates again in the coming quarters, which will have a negative impact on results again and I don’t expect impressive growth rates in the years and decades to come from Svenska Handelsbanken. But it is a solid well-run bank that will pay continuous dividends in the years to come.

Svenska Handelsbanken Annual Report 2022

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here