Note:

I have covered Vicinity Motor Corp. (NASDAQ:VEV) previously, so investors should view this as an update to my earlier articles on the company.

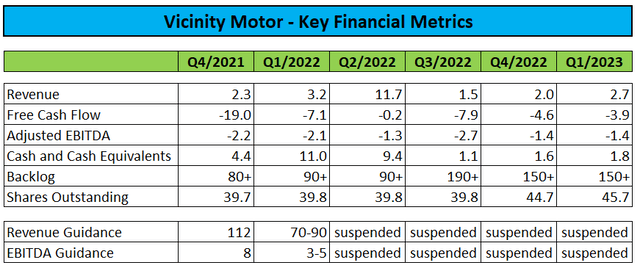

Earlier this month, small Canadian, BEV-focused bus and truck manufacturer Vicinity Motor Corp. or “Vicinity” reported another set of weak quarterly results with disappointing sales and significant cash burn:

Regulatory Filings

During the first quarter, Vicinity sold another 0.9 million newly issued shares into the open market for net proceeds of $0.8 million.

The company also raised CAD$4.0 million in gross proceeds from an expensive convertible debenture financing in late March (emphasis added by author):

The Convertible Debentures are issued in denominations of CAD$1,000, bear interest at 15% per annum, and mature 18 months from the closing date. Interest payments on the Convertible Debentures have been deferred to the twelve-month anniversary and/or maturity.

Each Convertible Debenture is convertible at the holder’s option into units of the Company (the “Units”) at any time prior to maturity at a conversion price of CAD$1.45. Upon conversion, each Unit will consist of one common share of the Company (“Common Share”) and 0.2 common share purchase warrants (each whole warrant a “Warrant”). Each Warrant is exercisable into one Common Share of the Company at an exercise price of CAD$1.45 for a period of thirty-six months following the closing of the Private Placement.

That said, management expects sales to improve going forward as the company’s new U.S. facility in Ferndale, Washington is expected to commence vehicle assembly operations in the very near future (emphasis added by author):

Our new U.S. manufacturing campus in Ferndale, Washington is slated to initiate production in the next several weeks – as we have completed key hires and have recently secured Foreign-Trade Zone status with the U.S. Department of Commerce, reducing customs and duty-related fees. To support the immediate-term ramp up of Ferndale, we recently supplemented our $30M VMC 1200 specific credit facility with the Royal Bank of Canada and Export Development Canada (“EDC”) with a further $9M working capital credit facility with EDC, fully funding our near-term operations with non-dilutive debt financing.

In addition, supply chain issues for the company’s core transit bus business have improved in recent months:

Our transit bus business has seen supply chains improve – and to that end, we have restarted delivery of transit buses to our customers as of Spring 2023. We continue to see strong demand for our Vicinity Classic transit bus line, proving out our established market leadership in the mid-size heavy duty transit bus space.

Just recently, Vicinity announced the receipt of a new purchase order from Transdev Canada for 42 Vicinity Classic diesel buses with delivery expected for next year.

On the conference call, management stated expectations for the company to achieve EBITDA profitability in the second half of this year which I find hard to believe considering the requirement to ramp U.S. operations basically from scratch and the fact that BEV trucks are an entirely new segment for Vicinity.

Given these issues, I wasn’t exactly surprised by the CFO declining analyst requests for more granularity on anticipated truck and bus deliveries this year during the questions-and-answers session of the call:

I think for the trucks, I’d like to say that we are just getting our facility up and running for the trucks in Ferndale. (…)

We can actually start ordering all of the parts and ramping up, but it’s tough to give a range right now until we actually are delivering out of Ferndale and see how quickly we can ramp that up. I think let us deliver these first 50 and then we can tell you exactly how long it’s going to take us to start delivering on the rest of the backlog, which is over 1,000 trucks.

For buses, we have over 100 buses in our backlog right now. We’re going to get — try to get as many of those as possible out this year. But I can’t tell you exactly how many of those will get out.

Moreover, Vicinity will soon have to address $6.9 million in convertible debentures currently scheduled to mature in early October as disclosed in a recent SEC-Filing (emphasis added by author):

On October 5, 2021, the Company issued C$10.3 million in unsecured debentures with a maturity 12 months from the date of issue. On June 15, 2022, the maturity date of the debentures was extended to October 4, 2023, with the extension being treated as a modification of the original debt with the classification changing from current to long-term liabilities. As a result, a gain of $803 on modification of debt was recorded during the three months ended June 30, 2022. In connection with the extension, the Company cancelled 412,000 warrants from the previous agreement. On extension the Company issued 1,000,000 warrants to purchase common shares at an exercise price of C$2.25 per share. The value of these warrants was incorporated in the $803 gain on modification of debt. The warrants expire on the debt maturity date of October 4, 2023.

The unsecured debentures include 8% annual interest paid at maturity with $449 being recorded as borrowing costs on June 15, 2022, and an effective interest rate of 24%.

During the three months ended March 31, 2023, the Company incurred $452 in interest expense (March 31, 2022 – $449) on this loan, $915 is included in accounts payable and accrued liabilities as at March 31, 2023.

On the conference call, management stated its expectation to address the debentures in a timely manner but another extension would almost certainly come at even worse terms.

Lastly, the company has initiated arbitration proceedings against Optimal Electric Vehicles LLC (“Optimal EV”) after having terminated the sales and marketing agreement in Q4/2022. According to statements made in the company’s annual report on form 20-F, Vicinity is looking to recover the majority of its original $20 million investment in Optimal EV.

Bottom Line

Vicinity Motor Corp. reported another set of weak quarterly results but on the conference call, management projected substantial improvements in sales and profitability for the second half of the year as BEV truck and transit bus production ramps up.

That said, I remain skeptical of the company’s ability to achieve positive EBITDA over the next couple of quarters as Vicinity’s new U.S. facility has not yet commenced operations and given the fact that BEV trucks represent an entirely new segment for the company.

In addition, Vicinity will have to extend or refinance close to $7 million in convertible debentures until October 4.

While I remain concerned about potential debt and execution issues as well as additional dilution from ongoing open market sales, I am raising my rating on the shares from “Sell” to “Hold” on expectations for substantial sales improvements in the second half of this year.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here