Plug Power Inc. (NASDAQ:PLUG) investors had a brief respite last week as it attempted to recover from a post-earnings selloff triggered by its poor guidance in its early May earnings release.

I noted that short-sellers loaded more bets into PLUG, as its short interest as a percentage of float surged to nearly 22% in mid-May. Last week’s rally could have driven some short-covering, as investors reacted positively to Plug Power’s announcement of 5MW of “containerized electrolyzer modules for first-ever use of industrial-scale green hydrogen” in Europe.

I believe PLUG bulls had been looking for better execution from the company in scaling its green hydrogen projects before adding exposure. However, the initial rally fizzled out toward the end of last week, suggesting that dip buyers likely aren’t convinced to hold on to their bets, quickly taking profits/cutting exposure on rallies.

But why? I have already cautioned in my March update that management was too confident in its outlook for FY23, persisting with revenue guidance of $1.4B and a gross margin outlook of 10%.

However, it now sees risks in its outlook, as it provided a bear case commentary to its guidance. Accordingly, management indicated that Plug Power envisages revenue of $1.2B and gross profit of $50M (4.2%) “in case of missed opportunities.”

As such, it’s a significant reduction from its initial gross profit guidance of $140M (10%), indicating that the company’s ability to scale could have been overstated (overpromising and underdelivering).

Wall Street analysts have learned their lessons as they revised down their expectations of the company’s revenue and earnings projections. Accordingly, analysts now expect Plug Power to deliver revenue of $1.29B for FY23, up 84.5% YoY. The revised gross margin forecasts have also been slashed to an average of 5.8%.

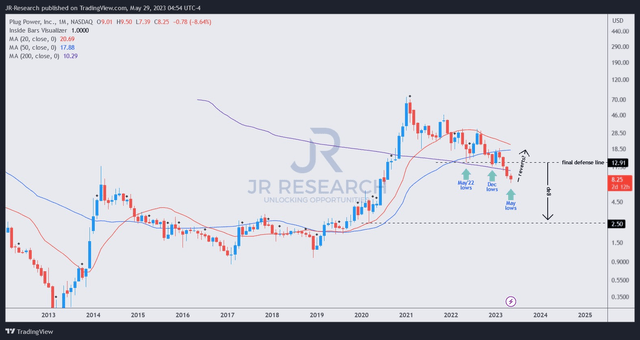

Market operators have clearly anticipated that Plug Power would disappoint as the year progresses. Notably, PLUG topped out in early February 2023 at about $19. Based on last week’s close of $8.25, PLUG investors have suffered a dramatic hammering at the hands of sellers, as it fell nearly 45% over the past three months.

Making matters worse for investors is that the Nasdaq (QQQ) (NDX) has been making new recent highs, as the leading mega tech players and semiconductor companies (SOXX) led the surge.

Hence, it all boils down to the critical question of when will high-conviction buyers return to support PLUG’s continued battering from its early 2021 highs? I urge investors not to bet on it, as sellers remain in significant control. Moreover, Plug Power is not expected to report adjusted EBIT margins until FY25.

Making matters worse, Plug Power will likely need to conduct fundraising, as its cash and short-term investments balance fell to just $1.64B in Q1, down from last year’s $3.4B.

Management stressed that it would likely seek “non-dilutive financing” to placate investors’ fears about share dilution. However, the critical question is whether it has sufficient positive cash-flow-generating assets for monetization?

Management telegraphed its confidence that Plug Power “will achieve positive operating cash flows by early next year due to their growth in margin trajectory.” As such, it would help the company leverage more “institutional opportunities,” mainly as it has been rapidly burning through its cash flow.

Plug Power is expected to report cumulative free cash flow or FCF of -$2.4B through FY25. As such, the reality of raising financing is likely not a matter of if but when and how.

Revised Wall Street estimates expect Plug Power to report about $74M in operating cash flow in FY24. However, I don’t think Plug Power has a significant enough runway to demonstrate sustainable and stable positive operating cash flow before it runs out of cash.

As such, I see the opportunity of raising asset-backed financing as unlikely. In contrast, investors should be prepared for potentially dilutive financing, which I believe the market is trying to price in, given the battering. Hence, the question is whether investors should buy the recent dips through its May lows?

PLUG price chart (weekly) (TradingView)

I observed that investors trying to pick up the pieces now would need to face the prospect of catching falling knives.

PLUG buyers failed to defend the “final defense line” in the chart above. That line was predicated against May 2022 lows, which was re-tested in December subsequently. However, the early-2023 rally fizzled out as sellers returned to hammer the dip buyers.

With PLUG falling into the “gap,” I assessed that the final resting point is too early to determine, even though PLUG could stage a short-term rally bolstered by short-covering activities.

However, Plug Power’s fundamentals and balance sheet look increasingly tenuous, with weakness implied in PLUG’s price action. Moreover, PLUG’s valuation grade of “C” by Seeking Alpha Quant suggests that it’s not undervalued. Hence, fundamentals and price action concur that there isn’t an optimal entry point at the current levels, even for a speculative opportunity.

Rating: Hold (Reiterated).

Important note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have additional commentary to improve our thesis? Spotted a critical gap in our thesis? Saw something important that we didn’t? Agree or disagree? Comment below and let us know why, and help everyone in the community to learn better!

Read the full article here