Introduction

Two quarters have passed since I last had a look at Summit Hotel Properties (NYSE:INN). I own both series of the preferred shares so every once in a while I need to keep a finger on the pulse to make sure the preferred shares remain in my income-focused portfolio. This article is meant as an update to previous articles so I would recommend you to read the older articles to get a better understanding of Summit Hotel Properties and its hotel portfolio.

The FFO and AFFO result in the first quarter of the year are looking good

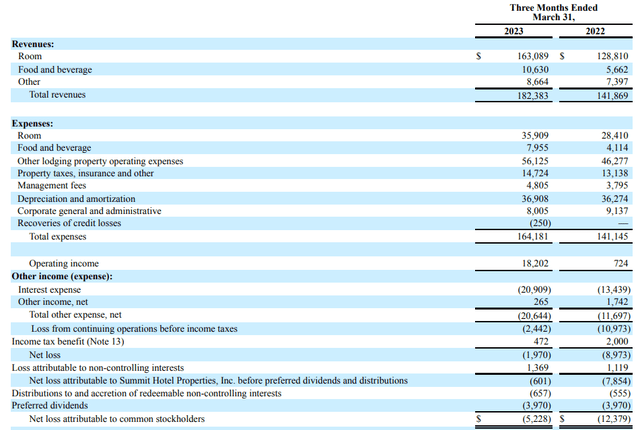

While I acknowledge the FFO and AFFO result of a REIT are the most important metrics, the FFO calculation usually starts with the net income or net loss and Summit Hotel Properties isn’t any different.

The hotel REIT reported a total revenue of just over $182M of which the vast majority (90%) was generated by the rental revenue from hotel rooms, which obviously has the highest margin as the operating costs associated with those rooms were just under $36M.

Summit Hotel Investor Relations

The hotel REIT reported a total operating income of $18.2M, which includes about $37M in depreciation and amortization expenses on the entire hotel portfolio. Unfortunately, Summit Hotel Properties also has to deal with increasing interest rates and the interest expense during the first quarter of the year increased to almost $21M and this resulted in a pre-tax loss of $2.4M and a net loss of $2M.

We still need to deduct the preferred dividend payments (almost $4M), the payments to non-controlling interests and add back the net loss attributable to non-controlling interests. This means the net loss attributable to the common unitholders of Summit Hotel Properties was approximately $5.2M.

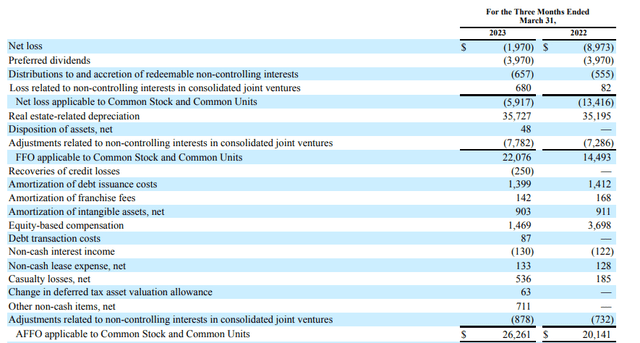

As mentioned before, the FFO and AFFO of a REIT are more important than a net income or net loss. As you can see below, Summit generated about $22.1M in FFO while the AFFO was even higher at $26.3M after adding back the amortization of the debt issuance costs and the equity based compensation to the equation.

Summit Hotel Investor Relations

This resulted in an FFO of $0.18 per share and an AFFO of $0.22 per share. An important improvement compared to the $0.12 and $0.17 FFO and AFFO per share in Q1 2022, despite the increased share count (122M shares outstanding versus less than 119M shares in Q1 2022).

That’s great news for the preferred shares as the REIT only needed about 13% of its AFFO to cover the preferred dividends.

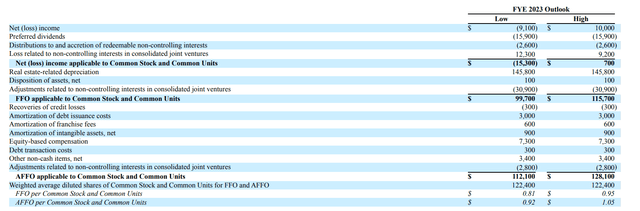

Looking at the outlook for this year, the coverage ratio of the preferred dividends should continue to increase.

Summit Hotel Investor Relations

As you can see in the image above, Summit anticipates a full-year AFFO of $112-128M. If I would use the lower end of the guidance, $112M, the net AFFO before taking preferred dividends into account would be approximately $128M. This means that in order for Summit Hotel Properties to cover the preferred dividends, it only needs to spend about 12.5% of the AFFO. In case Summit reaches the higher end of its AFFO guidance, it only needs about 11.1% of the AFFO to fully cover the preferred dividends.

The preferred shares are getting safer

The REIT currently has two publicly traded preferred shares outstanding. It issued 6.4M preferred shares series E while there are an additional 4 million preferred shares issued as a Series F. The E-Series pay $1.5625 per share per year in equal quarterly installments and can be called anytime while the F-shares can only be called from August 2026 on. The preferred dividend payable on the F-shares is $1.46875 per share, also payable in four equal quarterly payments.

The E-Series closed at $17.97 on Monday, May 22nd while the F-Series closed at $17.36. This results in a yield of 8.7% and 8.46% respectively which means the E-Series are per definition more attractive. Not only because the yield is higher but also because that series is more likely to be called (note: I don’t expect Summit to call these shares anytime soon).

I already established the excellent preferred dividend coverage levels in the previous section of this article, but I also wanted to have a look at the asset coverage levels.

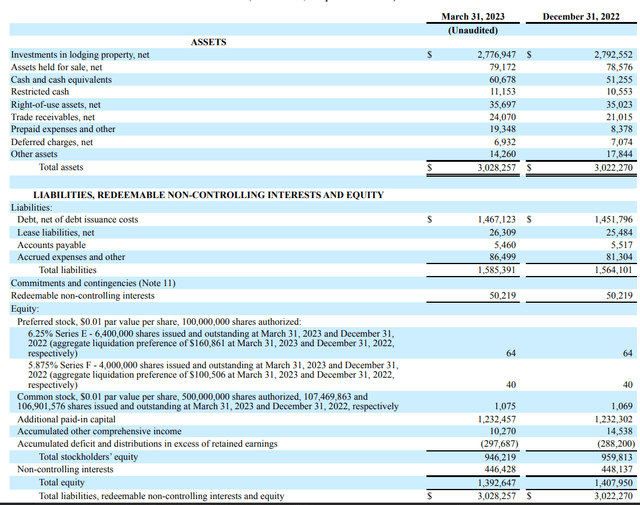

The image of the balance sheet below shows the net equity attributable to Summit Hotel Properties is $946.2M. This includes the 10.4M preferred shares which have a total value of $260M (as the issue price was $25 per preferred share).

Summit Hotel Investor Relations

This means there is just under $700M in equity ranked junior to the preferred shares while the asset coverage ratio (attributable equity versus the principal value of the preferred shares) is approximately 363%. That’s pretty decent, and keep in mind the book value of the real estate assets already includes about $727M in accumulated depreciation.

Investment thesis

While I am still focusing on the preferred shares of Summit Hotel Properties, the common shares are actually also getting pretty attractive as the REIT expects to generate an AFFO of $0.92-1.05 per share. This means that based on that guidance, INN is currently trading at just 6.5-7.3 times the AFFO and that’s very reasonable. Meanwhile, Summit Hotel is currently selling six hotels (for a total of 750 rooms) in two separate transactions at a capitalization rate of 3.9%. As that’s lower than the average cost of its debt, Summit may be able to increase its FFO and AFFO after completing the asset sale.

That being said, I will continue to focus on the preferred shares in the foreseeable future. I fully realize I may lose out on potential capital gains but a portion of my portfolio is dedicated to a (reliable) income stream. An interesting feature of the Summit Hotel preferred shares is that both series are convertible in common shares in case there is a change of control event happening. This should prevent the preferred shares from ending up as ‘orphans’ in case the acquirer doesn’t care about this element of the capital structure.

I currently have a long position in both series of the preferred shares, but I will add to my position in the E-Series as the yield is currently higher.

Read the full article here