Co-authored with Treading Softly.

Raising livestock is a difficult business. Beyond the day-to-day care and responsibilities, there is the mental aspect as well. Many new hobby farmers get too attached to the individual lives of very fragile creatures. While I’m not advocating for mistreating or improperly caring for animals, getting too attached to a living creature that has a very fragile existence is a recipe for sadness and failure.

One study on recently hatched baby chicks revealed that up to 50% of them will die before adulthood. This means that if you get really attached to a baby chicken, you have a coin flip of a chance of whether or not that chicken will become an adult. It can be emotionally taxing, and many give up their dreams of raising chickens because they fear the risk of loss.

More than one would-be hobby farmer raised cattle or hogs for meat and ended up with permanent pets. In essence, they quit before they receive the payoff.

When it comes to the market, people will often try to cut losses or avoid losses before they potentially occur. Peter Lynch famously said,

“Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.”

The big mistake people make is that they think they need to exit the stock market or leave the economy due to the fear of a recession. When they believe that things will get tough, they quit – never getting the long-term payoff that the market has proven to provide routinely.

What I like to remind members of my High Dividend Opportunities community is that, while a bull market mints millionaires, it’s the bear market that decides who those people are going to be when the recovery occurs. As professional income investors, we’re here to scoop up income on sale and enjoy it for decades to come. All those people trying to time the market and get out before potential losses or recessions happen are simply providing us with outstanding and amazing opportunities to reap high yields for years to come.

I’d rather be a buyer of great income than lock in losses for no reason other than fear. Today, I want to look at two excellent companies that are on sale and are providing high yields now and will continue to do so going forward.

Let’s dive in!

Pick #1: ORCC – Yield 10.4%

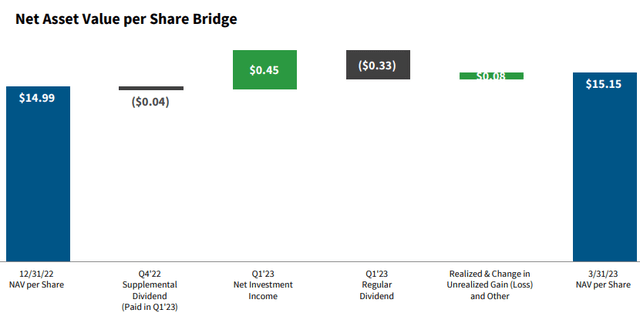

Owl Rock Capital Corporation (ORCC) is the second-largest public BDC (Business Development Company) in the U.S. by market cap. It focuses on lending to upper middle-market companies, with most of its portfolio in sponsor-backed companies. ORCC knocked it out of the park with Q1 earnings, reporting Net Investment Income (“NII”) of $0.45, a new record for the company and easily covering its $0.33 dividend and $0.04 supplement paid last quarter. For Q2, ORCC announced it is increasing the supplement to $0.06, which will be paid in June, while the regular $0.33 dividend will be paid in July. ORCC management continues to believe that getting dividends more frequently is better – we agree.

ORCC is achieving these fantastic results while maintaining leverage at 1.21x debt/equity. Over the past year, leverage has ranged from 1.17x-1.21x, essentially flat, even as earnings have grown from $0.31 to $0.45/share.

On top of record NII, ORCC also grew its NAV by $0.16/share. Source

ORCC Q1 2023 Investor Presentation

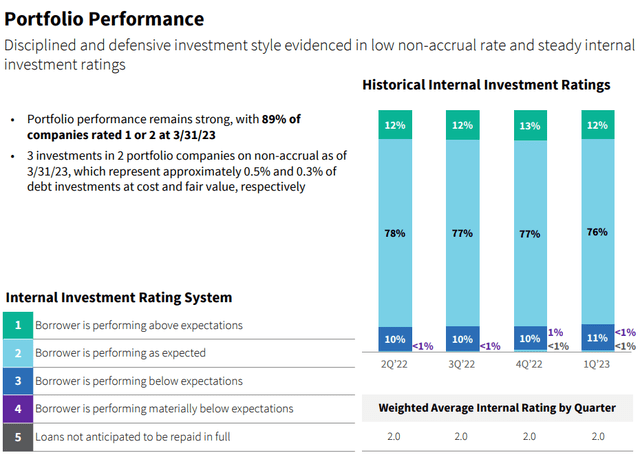

ORCC focuses on larger businesses than most BDCs do. Like Ares Capital (ARCC), ORCC focuses on the “upper middle market” with their borrowers having an average EBITDA of $176 million. These larger companies are lower risk, contributing to ORCC having very stable credit metrics. Only two borrowers are on non-accrual, accounting for 0.5% of ORCC’s portfolio at cost basis.

ORCC Q1 2023 Investor Presentation

ORCC is seeing growing NII, rising NAV, frequent supplemental dividends, and high credit quality in its portfolio. We’ve been saying for the past several years that ORCC is a high-quality BDC that deserves to trade at a premium to NAV. The proof is in the numbers, ORCC is crushing it. Eventually, Mr. Market will wake up and notice. Until then, we are happy to collect multiple dividends every quarter and buy more shares at a discount to NAV.

Pick #2: SLRC – Yield 11.8%

SLR Investment Corp. (SLRC) is a BDC that focuses on asset-based and equipment-based lending. This form of lending is lower risk because SLRC has specific collateral that can be seized or repossessed in the event the borrower defaults. As a result, SLRC has frequently outperformed peers in terms of credit quality.

Where SLRC ran into difficulty during COVID was the volume of loans they held. When speaking about “concerns” over leverage, our concern is usually that the company might be overleveraged and taking on too much risk. Over the past two years, the problem for SLRC has been the opposite – SLRC was underleveraged. When COVID happened, companies simply stopped borrowing. So, as SLRC’s borrowers were so inconsiderate as to actually pay off what they owed, SLRC saw its earnings decline.

In Q1 of last year, SLRC reported NII of $0.32 with leverage at 0.98x debt/equity, failing to cover the dividend. By Q1 this year, SLRC grew NII 28% to $0.41, meeting its $0.41 dividend. This increase was primarily thanks to increasing leverage to 1.12x, with some help from rising interest rates.

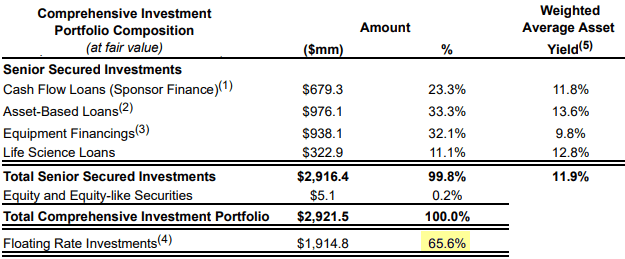

Most BDCs borrow at a fixed rate and lend floating-rate loans. This is the main reason why BDCs have seen significant earnings growth over the past year. Most BDCs have 90%+ loans at floating rates. SLRC has a different profile, with about 2/3rds of its portfolio paying a floating interest rate. Source.

SLRC Q1 2023 Earnings Release

As a result, SLRC is less interest rate sensitive than the average BDC. The positive is that when interest rates start to decline, SLRC will be able to maintain its NII.

While SLRC’s leverage has increased from 0.98x to 1.12x over the past year, leverage is still very conservative. Management has indicated they would be willing to bring leverage up to a maximum of 1.25x. We believe the ideal range would be 1.15x-1.2x.

SLRC continued to pay the current dividend through the difficult years, and now they are covering it. As it leverages up more, the dividend will become even more secure.

NAV is $18.04/share, making SLR Investment Corp. a very attractive price opportunity today.

Conclusion

Even if the economy may be slowly approaching a recession or is in the midst of a recession, the economy is still in motion.

If every business was to shut down and every person were to become unemployed, there would be absolutely no economic activity whatsoever. Of course, this is a ridiculous thought, as somebody would have to be doing something for us to be fed or to get water or power – there will always be some level of economic output, even if it’s pockets of small regional activity.

These two investments that we’ve looked at, Owl Rock Capital Corporation and SLR Investment Corp., are both engaged in various sections of the economy. They provide vital financial liquidity and management services to middle-market companies to enable them to continue to operate and provide basic services to you and me.

Don’t make the big mistake that so many make, and lock in losses simply because you fear losses. Instead, think like a professional income investor – make the big choices to get the big income and then enjoy it over and over again.

My goal for each one of you is that if you choose to be an income investor, you can proudly wear a shirt that says, “My retirement is paid for by dividends!“, and have it be the truth. Nothing beats financial security for a more relaxing and enjoyable retirement. Financial security can be achieved through having excess income that overwhelms and overpowers your expenses.

That’s the beauty of our income method. That’s the beauty of income investing.

Read the full article here