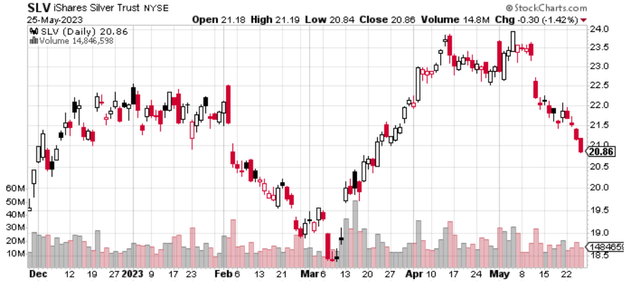

Silver prices recently retreated (as shown below in the chart of iShares Silver Trust ETF (NYSEARCA:SLV) (which represents 1 ounce for each share)) due to (i) Fed being more hawkish and expectations of Fed easing being pushed out and (ii) worries about Chinese economy.

silver prices (stockcharts.com)

I believe these factors are less important – the supply and demand fundamentals are extremely favorable for silver and as macro worries fade or become a new normal, silver prices will shine.

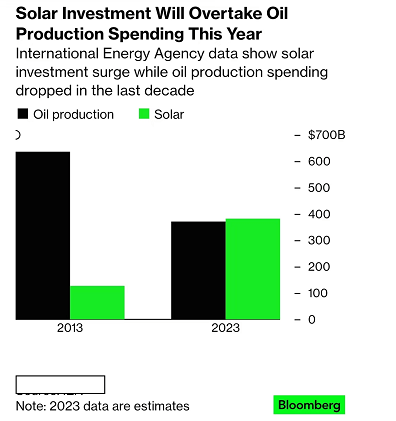

1. Solar investment expected to overtake oil production spending this year

According to an article from Bloomberg today, solar investment is expected to reaching c.$400 billion and exceed investment in oil production this year, further cementing its status as a major source of energy investment. This is in sharp contrast with 2013 when oil production investments were $600 billion and solar investments were around $100 billion.

solar investment (Bloomberg)

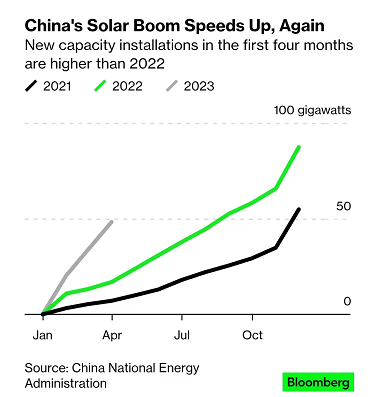

2. Solar growth is driven by stronger than expected China demand

Solar may be one of the biggest beneficiaries of China’s shift towards more focus on “security”. China’s solar capacity installations in the first four months of 2023 are higher than the full year 2022.

China solar boom (Bloomberg)

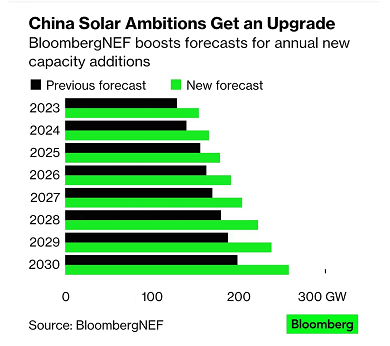

The increased and high level of Chinese installations is forecast to remain at a high level for the rest of the decade as shown below.

China solar forecast (Bloomberg)

In early 2023, consensus forecasts of global solar installation for 2023 was somewhere in the 200+GWs, but now this forecast to be nearer 350 GW as China installation growth accelerates far above expectations.

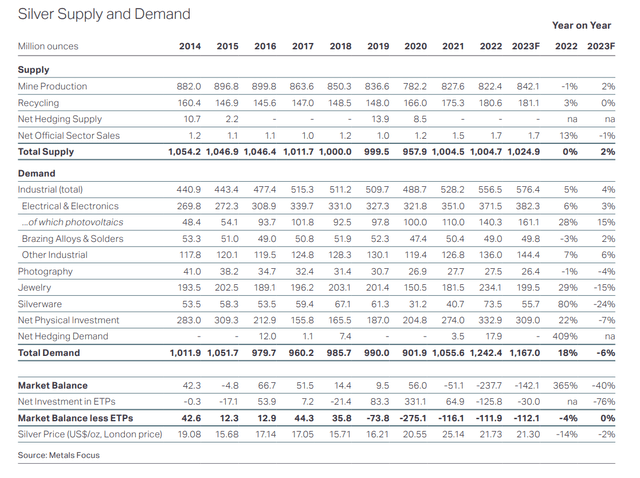

3. Silver demand has been relatively inelastic while new mine supply has peaked since 2016

silver supply demand (The Silver Institute)

Half of silver demand is from the industrial sector, but this demand is relatively inelastic. In 2020, the impact of the coronavirus pandemic only led to a 4% decline in silver demand (20million oz), whereas the increase in solar demand for silver was 30million oz (more than the decline in overall industrial demand in 2020) in 2021.

Even if the economy heads into a recession, the negative impact on silver demand is likely to more than covered by growth from solar (giving solar a margin of safety). And if there is no recession at all, once the market realizes that silver demand may persistently exceed supply for years to come, I believe prices will enter a bull market.

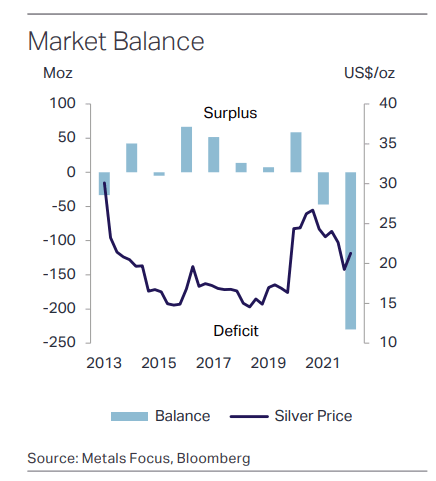

4. Supply and demand is king – monetary policy is second fiddle

Though precious metals are believed to benefit from low interest rates, the fundamental supply/demand situation probably plays a bigger role. For example, there was a surplus in silver from 2014 to 2020 as shown below.

silver supply demand (the Silver Institute, Metals Focus)

When comparing SLV (red line) and 10 year US treasury yields, we could see that there was no bull market in silver despite nearly a decade of low interest rates. While monetary policy could create an environment conducive to precious metals, at the end of the day, supply-demand fundamentals drive the situation.

Silver vs 10 year treasury yields (stockcharts)

If low interest rates have no noticeable impact on silver prices, then I would argue that high interest rates might not prevent silver from entering a bull market if demand is very strong and consistently outstrips supply.

5. Silver as a percentage of costs are miniscule

161 million oz of silver are expected to be used for solar in 2023, approximately $3.5 billion, which is less than 1% of the total forecast 2023 solar investment ($400 billion). So even if silver prices double or triple, it will only represent a miniscule portion of the overall investment and the industry is unlikely to completely shift from silver anytime soon.

Summary:

Strong growth in solar investment (particularly driven by Chinese solar installations, which year to date have exceeded that of the whole year of 2022) is increasing silver demand at a time when silver demand has already exceeded supply and the market is expected to remain in a deficit for many years to come. Buying silver on each dip (including the latest dip in prices) may be worth considering and I am buying the dip as well.

Read the full article here