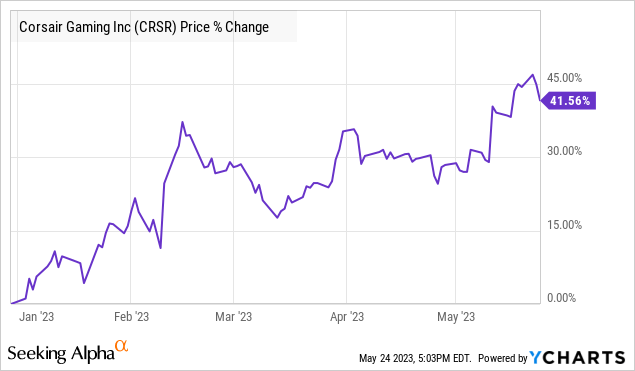

Corsair Gaming, Inc. (NASDAQ:CRSR) has been a surprising winner in 2023 with shares up more than 40%. The company recognized for its high-end gaming PC components has been on a roller coaster of extremes since its 2020 IPO, at first benefiting from the pandemic-era boom to dealing with the broader industry slowdown last year.

Indeed, while shares are still down more than 60% from its all-time high, the rally over the past year reflects an ongoing financial turnaround and improving earnings outlook. Efforts by management to control costs and push pricing are paying off, and we can also highlight encouraging operating trends.

Overall, we like Corsair Gaming as a segment leader with solid fundamentals. At the same time, we believe the rally in the stock over the last several months has already incorporated many of the positive developments. In our view, the company will need to continue executing while delivering stronger top-line momentum as a catalyst for the next leg higher. The upside may be limited in the near term.

CRSR Earnings Recap

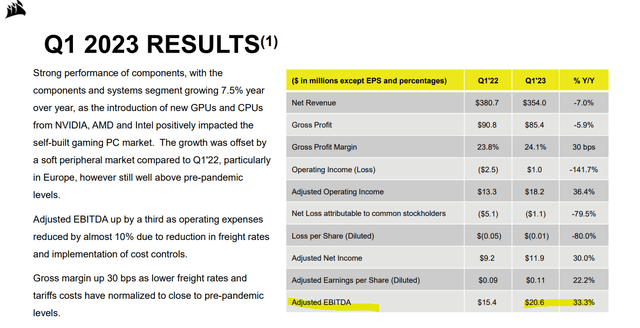

The takeaway from Corsair Gaming Q1 report was the rebounding profitability with adjusted EPS of $0.11, up 22% from $0.09 in the period last year. Adjusted EBITDA reached $20.6 million, climbed by 33% y/y even as net revenue of $354 million is down -7% from Q1 2022.

The effort was achieved through the combination of a 30 basis point increase in the gross margin while total operating expenses as a percentage of revenues declined by 70 basis points.

Corsair has been able to maintain premium pricing at a time when the rest of the market has been forced to discount. On the cost side, margins are benefiting from easing supply chain conditions and falling inflationary pressures that defined the environment in 2022.

source: company IR

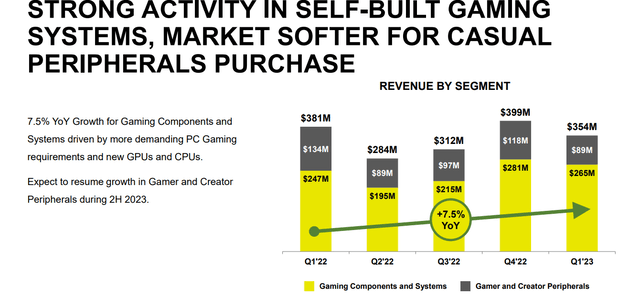

Operationally the core “Gaming Components and Systems” segment was the strong point in Q1 with a 7.5% y/y revenue increase in Q1. Management explains that new enthusiast-oriented GPUs and CPUs from chip leaders like NVIDIA Corp (NVDA) and Advanced Micro Devices, Inc. (AMD) are driving an upgrade cycle in the self-build gaming PC market.

The theme follows a trend in PC gaming with the latest releases demanding more powerful PC hardware, particularly memory where Corsair is the market leader in the high-performance category.

On the other hand, the smaller and more volatile “Gamer and Creator Peripherals” segment, which represents about 25% of the business has been a drag amid broader industry weakness in these categories translating to a -34% decline in revenue. Corsair expects a recovery in this market through the second half of the year.

In terms of guidance, the target is for full-year revenue between $1.35 and $1.55, representing a 7% y/y increase at the midpoint. Corsair is also forecasting 2023 adjusted EBITDA between $90 and $110 million, which is more than double the $46.5 million result in 2022. Again, this would be from the firming margins coupled with a top-line rebound.

Finally, we can mention that Corsair ended the quarter with $179 million in cash against $230 million in total debt. A net leverage ratio under 1x is a strong point in the company’s investment profile.

source: company IR

Is CRSR A Good Stock?

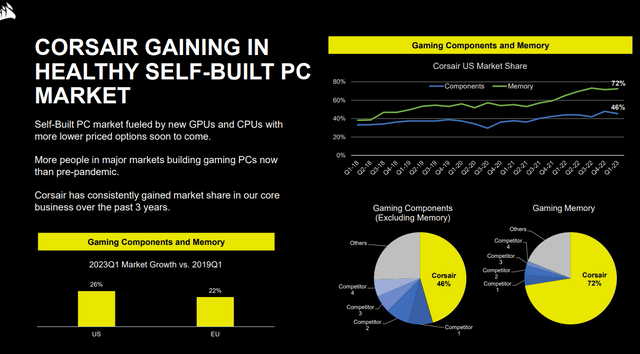

The attraction of Corsair Gaming is the company has established a leadership position with a 46% share of the U.S. PC gaming components market and even 72% just considering gaming memory.

By this measure, the latest Q1 results in the segment with positive growth is even more impressive considering the broader weakness in the global PC market and video games sales which are down compared to 2022. In other words, Corsair is something of an exception, managing to gain market share reflecting the brand momentum and customer loyalty.

We already mentioned the gaming industry shift of requiring higher levels of RAM as a tailwind for Corsair’s memory business. Similarly, those increasingly powerful builds require more advanced energy management systems and efficient cooling which all fall into Corsair’s portfolio.

On this point, Corsair is also benefiting from the relative strength in the “self-built” PC market where more gamers are choosing to source the components for high-performance PCs individually. This is positive for Corsair because its parts and components are often seen as category benchmarks where the company can lead on pricing.

source: company IR

What’s Next For CRSR?

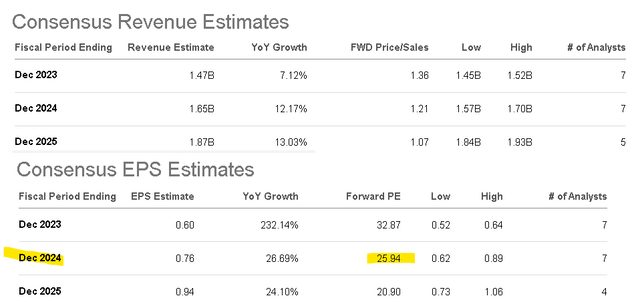

Overall, we see Corsair as well-positioned to key capture these trends supporting a positive long-term outlook. According to consensus estimates, the market is forecasting full-year 2023 revenue at $1.5 billion, in line with management guidance for a 7% increase.

The market also sees EPS reaching $0.60, which compares to just $0.18 in 2022 but remains below the record $1.60 in 2021. Looking ahead, the expectation is for revenue growth to average about 12.% through 2025, while EPS trends towards $0.76 by next year.

Overall, we believe these estimates are reasonable, although we’ll need to wait to see the annual net revenue growth turn positive compared to the decline in Q1.

Seeking Alpha

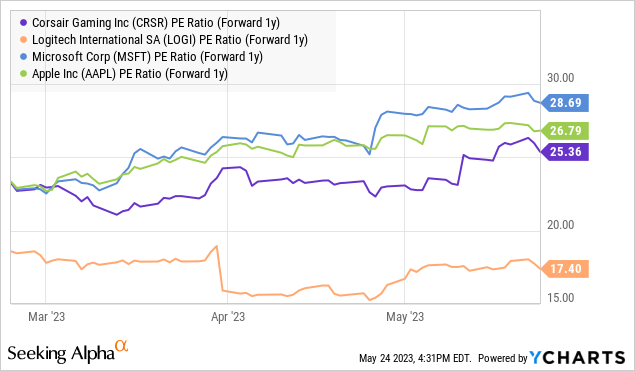

As it relates to valuation, we’re a bit more skeptical here. The metric we’re focusing on is the 1-year forward P/E of 26x based on the 2024 consensus EPS. Assuming the forecasts are reached, this type of earnings premium can be justified considering the expected growth momentum.

The concern, however, is that these multiple leases have little room for error, where weaker-than-expected results would force a re-pricing of the stock and likely push shares lower.

We’d also highlight how CRSR is being priced at a level similar to mega-cap tech names like Apple Inc (AAPL) and Microsoft Corp (MSFT), both with a 1-year forward P/E ratio of around 27.5x, while at a large spread to a name like Logitech International S.A. (LOGI) at 17x on the metric.

Final Thoughts

We rate CRSR stock as a hold, balancing our positive long-term outlook for the company against a sense that valuation remains pricey. CRSR may have been undervalued at the start of the year, but the share price climb in recent months has taken it closer to fair value around $20.00.

To the upside, a string of strong quarterly reports through 2023 could work to push earnings estimates higher as a catalyst for further share price gains.

The main risk to consider would be a deeper deterioration of the global macro backdrop. A scenario where economic activity sputters would likely pressure demand and the sales environment for Corsair.

Industry market data across PC sales and video game trends will also be key monitoring points with Corsair rooting for a stronger recovery sooner rather than later.

Read the full article here