NorthWestern Corporation (NASDAQ:NWE) is a regulated electric and natural gas utility that serves the states of Montana, South Dakota, Nebraska, and Yellowstone National Park. This is not exactly a very populated region of the nation, so the company does not have a lot of customers, but it still has many of the same characteristics that have long made the utility sector a popular one among conservative investors.

In particular, the company enjoys remarkably stable cash flows regardless of economic conditions. That is something that could prove to be very appealing, as we are seeing a growing number of signs that the United States may soon enter a recession. We are also seeing average Americans suffer severe financial strains, which would also prove to be an advantage for a utility company like NorthWestern Corporation. When we combine this with a very attractive 4.41% dividend yield and a very reasonable valuation, we can see numerous reasons to like NorthWestern Corporation as an investment today.

About NorthWestern Corporation

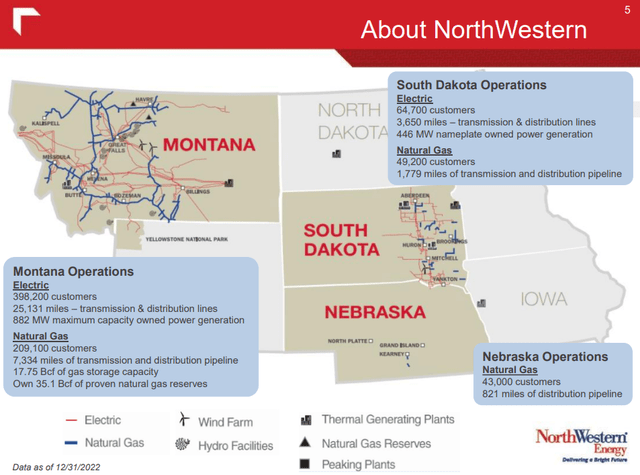

As stated in the introduction, NorthWestern Corporation is a regulated electric and natural gas utility that serves the states of Montana, South Dakota, and Nebraska. The company also serves Yellowstone National Park.

NorthWestern Corporation

As we can clearly see, the company has a huge service territory geographically, but it is one of the most rural regions of the country. In fact, the largest city in the company’s service territory is Billings, Montana, with a population of 118,288 according to the U.S. Census Bureau. Thus, the company does not have anywhere near the customer count of a much smaller utility servicing even a single city on the East Coast.

As I have pointed out in a number of previous articles, though, just because a utility has a relatively small customer base does not mean that it does not enjoy many of the same characteristics that investors have traditionally appreciated about utilities. Perhaps the most important of these characteristics is that the company has remarkably stable cash flows over time. We can see this quite clearly by looking at the company’s operating cash flow. Here are NorthWestern Corporation’s operating cash flows for each of the past eleven twelve-month periods, including the most recent quarter:

NorthWestern Corporation

As we can clearly see, the company’s operating cash flows do not typically exhibit huge swings as we might see with companies in other sectors. The biggest reason for this is that NorthWestern Corporation’s products are generally considered to be necessities for our modern way of life. After all, there are not very many people in the United States that do not have electric and natural gas services to their homes and businesses.

That is even more true in this company’s service territory, which includes some of the coldest regions of the nation. As such, most people will prioritize paying their utility bills ahead of making discretionary expenses during times when money gets tight. This is something that could be especially important today, as the high inflation in the nation has inflicted a great deal of pain on consumers, and many of them can no longer afford the luxuries that they may have become accustomed to. For example, keeping the electricity on in your home is much more important than buying the latest smartphone or going to a nice restaurant.

Thus, NorthWestern Corporation should be able to withstand difficult economic conditions much better than many other companies. This is exactly the kind of thing that anyone would want to have in their portfolios as the economy continues to weaken.

Growth Prospects

As investors, we want to see more than simple stability. After all, stability alone is not sufficient for acceptable investment returns. We want to see any company in which we are invested grow and prosper with the passage of time. Fortunately, NorthWestern Corporation is well-positioned to do this. There are two ways in which the company will achieve this growth:

- Population growth in its service territory.

- Rate base growth.

We will discuss each of these in turn.

One of the ways in which any utility can grow its operations is through increasing the size of its customer base. Unfortunately, since utilities tend to be monopolies that have government-controlled geographic service territories, their ability to grow through this method is rather limited.

Fortunately for NorthWestern Corporation, Montana is one of the most rapidly growing states in the nation. According to the U.S. Census Bureau, Montana’s population is growing at a 1.5% annual rate, which is sixth in the nation. This is being driven by people trying to leave crowded and expensive states such as California. Montana’s neighbor Idaho has also benefited from this trend, although NorthWestern Corporation does not serve that state. In the case of Montana though, we can see that the company’s service territory includes most of the state, including the major cities.

Thus, we can logically assume that the company will benefit from this migration through a growing customer base. As more customers translate to more people purchasing the company’s electricity and natural gas, and paying their bills, it should translate into revenue growth all else being equal.

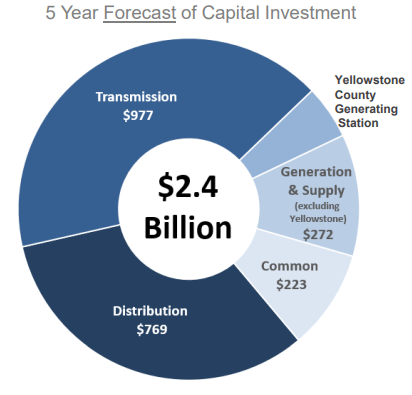

The second way through which NorthWestern Corporation can achieve forward growth is by increasing its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the price that it charges its customers in order to achieve that specified rate of return. The usual way in which a company grows its rate base is by investing money into upgrading, modernizing, or even expanding its utility-grade infrastructure. NorthWestern Corporation is planning to do exactly this, and has recently unveiled a $2.4 billion capital investment plan to this effect:

NorthWestern Corporation

The company plans to spend this money over the 2023 to 2027 period, which would represent a $300 million increase over the $2.1 billion that the company invested in its infrastructure over the 2018 to 2022 period. That is certainly not unusual, though, as most utilities increase their infrastructure spending over time due to inflation and general economic growth.

Unfortunately, NorthWestern Corporation did not provide a year-by-year breakdown of its investment plans, but it invested $580 million into its infrastructure in 2022 so 2023’s capital expenditures will probably be a bit above this and grow over time. We may also see this projected spending level increase going forward since $2.4 billion is only $480.0 million per year over a five-year period and thus it implies a decrease at some point from the 2022 level. NorthWestern Corporation expects that its capital investment plan will grow its rate base at a 4% to 5% compound annual growth rate over the period so it seems unlikely that it will cut spending to any significant degree in a given year.

This projected rate base growth gives the company a projected earnings per share growth rate of 3% to 6% annually over the 2023 to 2027 period. That is admittedly lower than most other utilities that we have discussed in this column. However, when combined with the company’s current 4.41% dividend yield, it still gives a total return of 7.5% to 10% annually. That is reasonable, albeit still a bit lower than some of the company’s peers.

Financial Considerations

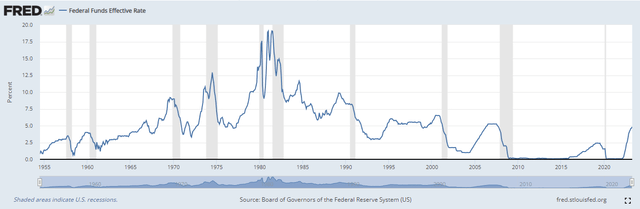

It is always important to investigate the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. This can cause a company’s interest expenses to increase following the rollover, depending on the conditions in the market. This is something that could be especially important today.

As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates over the last year in an attempt to combat the very high inflation that is running rampant in the United States. As we can see here, the federal funds rate is now at the highest levels that we have seen since 2007:

Federal Reserve Bank of St. Louis

Thus, it seems essentially certain that any company rolling over its debt today will see its interest expenses go up. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. Although utilities like NorthWestern Corporation usually have remarkably stable cash flows over time, bankruptcies have occurred in the sector so this is still a risk that we should not ignore.

One metric that we can use to analyze a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. In addition, this ratio tells us how well a company’s equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of March 31, 2023, NorthWestern Corporation has a net debt of $2.5854 billion compared to $2.693 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 0.96 today. This is one of the lowest ratios that can be found in the utility sector, which can be seen here:

| Company | Net Debt-to-Equity Ratio |

| NorthWestern Corporation | 0.96 |

| DTE Energy (DTE) | 1.83 |

| Eversource Energy (ES) | 1.49 |

| Exelon Corporation (EXC) | 1.65 |

| CMS Energy (CMS) | 1.82 |

| FirstEnergy Corp. (FE) | 2.10 |

As we can clearly see, NorthWestern Corporation is the only company out of this group that has lower net debt than its total shareholders’ equity. The company’s ratio has also improved substantially since the last time that we discussed it. This is a clear sign that the company is not employing too much debt to finance its operations, which is a very good thing considering the rising costs of debt refinancing and service. Investors, therefore, should not have to worry too much about NorthWestern Corporation’s debt load.

Dividend Analysis

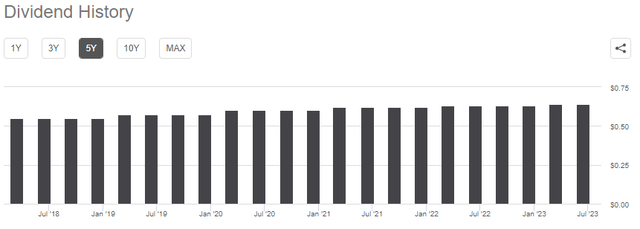

One of the biggest reasons why investors purchase shares of utility companies is because of the very high dividend yields that the stocks of these firms typically possess. NorthWestern Corporation is no exception to this as the stock yields 4.41% at the current price. NorthWestern Corporation also has a history of raising its dividend on an annual basis, although recent increases have been quite small:

Seeking Alpha

This is something that is quite nice to see during inflationary periods, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that can be purchased with the dividend that the company pays out, which can make anyone feel as though they are growing poorer and poorer with the passage of time. The fact that the company raises its dividend on an annual basis helps to offset this effect and maintains the purchasing power of the dividend that the company pays out. Admittedly, recent dividend increases have been less than the current inflation rate, so the dividend has still lost some of its purchasing power over time. However, the dividend increase was still better than nothing as it at least partially offset some of the impacts of inflation.

Naturally, it is important that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut, since such an event would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a company’s ability to afford its dividend is by looking at its free cash flow. The free cash flow is the money that is generated by a company’s ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the money that is available for tasks such as reducing debt, buying back stock, or paying a dividend. In the twelve-month period that ended on March 31, 2023, NorthWestern Corporation reported a negative levered free cash flow of $237.5 million. That is obviously not enough to pay any dividends, yet this company still paid out $144.2 million in dividends over the period. At first glance, this is likely to be quite concerning as the company clearly cannot afford to cover its dividend with free cash flow.

However, it is not uncommon for a utility to finance its capital expenditures via the issuance of equity and debt. It will then pay its dividends out of operating cash flow. The reason for this is that it is extremely expensive to build and maintain utility-grade infrastructure over a wide geographic area, and these costs would otherwise make it impossible for utilities to ever pay a dividend or provide a shareholder return. In the most recent trailing twelve-month period, NorthWestern Corporation reported an operating cash flow of $325.3 million. That was more than enough to cover the $144.2 million that was paid out in dividends and still leave a reasonable amount of money left over that can be used for other tasks. Overall, the company’s dividend is probably pretty safe.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like NorthWestern Corporation, we can value it by looking at the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa.

However, there are very few companies with such a low ratio in today’s overheated market. Thus, the best way to use this ratio today is to compare NorthWestern Corporation’s valuation to that of its peers in order to determine which company offers the most attractive relative valuation.

According to Zacks Investment Research, NorthWestern Corporation will grow its earnings per share at a 6.76% rate over the next three to five years. This is a bit more than we calculated earlier based on the company’s rate base growth, but it is not out of the realm of possibility considering the population growth of the company’s service territory. Thus, this growth estimate seems to be reasonable. This earnings per share growth rate gives the company a price-to-earnings growth ratio of 2.47 at the current stock price. Here is how that compares to the company’s peer group:

| Company | PEG Ratio |

| NorthWestern Corporation | 2.47 |

| DTE Energy | 2.94 |

| Eversource Energy | 2.63 |

| Exelon Corporation | 2.55 |

| CMS Energy | 2.53 |

| FirstEnergy Corp. | 2.35 |

As we can clearly see, NorthWestern Corporation appears to be quite reasonably valued relative to its peers. In fact, the only company that has a more attractive valuation is FirstEnergy, but that firm has a substantial debt load compared to every other utility in the chart. As NorthWestern Corporation has the strongest balance sheet here and a very reasonable valuation, it appears to be offering the best investment opportunity of any of these companies.

Conclusion

In conclusion, there appears to be a great deal to like about NorthWestern Corporation as the economy and the average consumer continue to weaken. In particular, NorthWestern Corporation should be able to weather any economic weakness much better than companies in most other sectors without suffering any ill effects. It also is positioned to benefit from demographics as people flee expensive high-tax states in favor of Montana. When we combine this with a very strong balance sheet and an attractive valuation, NorthWestern Corporation might be worth adding to a portfolio today.

Read the full article here