On our last coverage of Alibaba (NYSE:BABA), we acknowledged that the bulls were better setup, but did not attach a buy rating on that optimism. Specifically we said,

Yes valuation has compressed, BABA is buying back shares and even laying off people to improve profitability. At 1.8X sales you are not remotely paying as much as those cowboys ready to pony up 10X sales at the 2020 peak. So the odds are in your favor, but the risks are enough to make this a value trap and we are staying out.

Source: It Ain’t The Delisting, It Is Still The Bubble

Since then BABA has delivered pulse pounding action. It dropped 30% from that point and then almost doubled off the bottom. If the price action was not confusing enough, it then proceeded to wipe out all those gains, settling 9% lower.

It Ain’t The Delisting, It Is Still The Bubble

We look at the recently released results and update our outlook on the stock.

Q4 Results

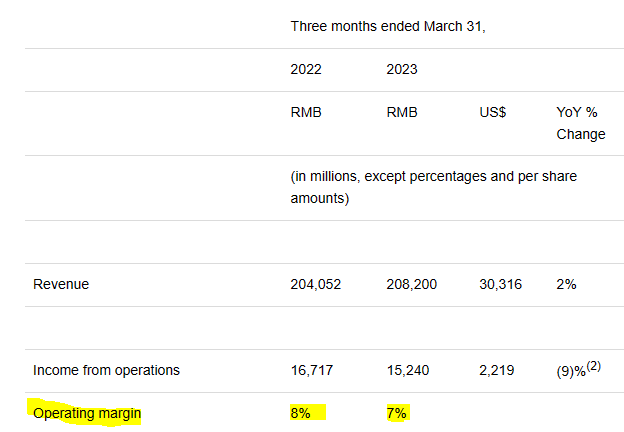

The quarter ended March 31, 2023 was the fourth quarter of BABA’s fiscal year. The company reported revenues of $30.32 billion, apparently “beating” estimates. Estimates beats are like a participation trophy. Everyone gets one these days. So if that was the extent of what you wanted to look at, sure, BABA did ok. But from our perspective, what is notable is the remarkable slowdown in the once fast growing powerhouse. Sales were up just 2% year over year. In 3 years, sales growth has dropped from the 40% range down to just 2%. This is now about in line with China’s trailing 12-month inflation rate. In other words, real sales (adjusted for inflation) have come to a standstill. Operating margins also show the pressure on the company to turn even those measly sales growth dollars into profits.

BABA Press Release

Outlook

It is not at all uncommon to find wildly optimistic outlooks on a company’s future. It is almost impossible to find a realistic assessment of how the company will do, just before a recession. Almost no analyst incorporates this into their modeling. Here we are seeing the same thing. BABA will apparently increase its sales by 10% a year.

BABA Press Release

Huh? Have any of them seen what the macro situation looks like in China? With a company the size of BABA, you are relegated to tracking nominal GDP in retail sales. With China’s property market still in the early stages of its downtrend, don’t expect those double digit growth days to come back. This is despite some creative measure by banks to try and push out the day of reckoning.

Some banks in the cities of Nanning, Hangzhou, Ningbo and Beijing have extended the upper age limit on mortgages to between 80 and 95, according to a number of state media reports. That means people aged 70 can now take out loans with maturities of between 10 and 25 years.

China’s property market is in the midst of a historic downturn. New home prices had fallen for 16 straight months through December. Sales by the country’s top 100 developers last year were only 60% of 2021 levels.

The new age limits, which aren’t yet official national policy, aim to breathe life into the country’s moribund property market while taking into consideration China’s rapidly aging population, said Yan Yuejin, a property analyst at E-House China Holdings, a real estate services firm, in a recent research note.

“Basically, it’s a policy tool to stimulate housing demand, as it can alleviate the debt payment burden and encourage home buying,” he added.

The new mortgage terms are like a “relay loan.” If the elderly borrower isn’t able to repay, his or her children must carry on with the mortgage, he said.

Source: CNN

And that is not all they are trying.

China is trying to manage down the oversupply of homes as well as prices to bring the market in balance, he says. In other words, a “controlled deflation” of the bubble rather than a dramatic burst. “If you want to improve affordability without having a systemic crisis, you don’t actually want house prices to fall. You want them to stabilize and incomes to rise,” Orlik says. “If prices fall 25% and everyone sells their houses, then you have a systemic crisis.”

China is even trying to limit price declines in some areas. Since the second half of last year, at least 20 small cities have blocked developers from slashing prices by more than 15%. That prompted an industry group in the province of Guangdong to petition authorities to loosen restrictions to boost sales, people familiar with the matter say.

Source: Bloomberg

If all of that screams “soft-landing”, then we wish you Godspeed.

It’s hard to overstate the importance of real estate to China’s economy, making the crackdown so painful for so many. With estimates ranging from $2.4 trillion for the new-home market to $52 trillion for existing homes and inventory, the size of the sector was twice that of the US’s in 2019. Real estate accounts for about a quarter of domestic output and almost 80% of household assets.

Some 100,000 companies operate in the sector, providing 27 million jobs as the nation’s second-biggest employer. Headcount shrank by 15% in the first half of 2022 alone among the 28 publicly listed developers that disclose staff levels, according to data compiled by Bloomberg.

Those still employed face steep pay cuts, usually 30% to 50%.

Source: Bloomberg

So trying to focus on the company specifics for BABA while ignoring the glaring macro is a recipe for disaster. Right or wrong (and anyone get things wrong), we are sticking to the macro over micro for this company and we have done that since our first coverage.

Seeking Alpha

Verdict

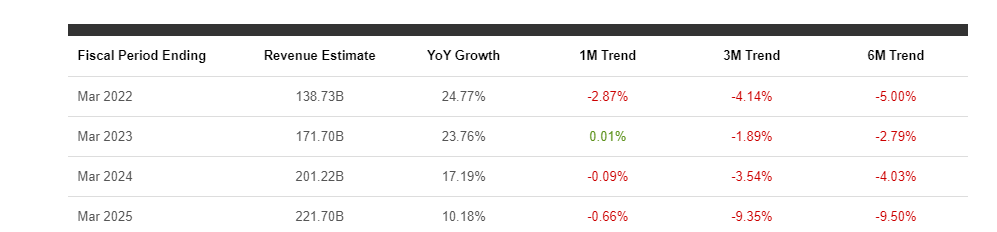

The big picture. We all like to talk about it, but we often get caught up in the trading noise. Back in 2021 analysts were fawning over BABA expecting, we kid you not, $221.7 billion of sales in fiscal 2025. The screenshot is from our first article dated November 19, 2021.

BABA Sales Estimates From November 2021

Note that even those estimates had dropped by 10%, so in March 2021 BABA’s sales were expected to be close to $250 billion in fiscal 2025. Those are now expected to be $150 billion, a number that has no chance in Hades of coming true.

Seeking Alpha

So that growth story has long since sailed and you would only be able to spot that ship if the earth was actually flat.

Of course, the second part of the “bubble” was the ridiculous valuations people assigned to BABA’s cloud segment. Anyone wanting an explanation for why the stock cratered despite the earnings beat just needs to read what is happening to that arena.

Chinese internet giant Tencent Holdings (OTCPK:TCEHY) is cutting prices for cloud services by up to 40% from June amid similar moves from rivals that have plunged the sector into a price war.

The fierce competition comes amid soft corporate demand, with the Chinese economy in the midst of a wobbly recovery since abandoning strict COVID-19 restrictions last year.

BABA said last month it would slash prices for some cloud products by up to 50%. State-owned China Mobile joined Tencent on Tuesday in announcing cuts, saying prices for some services would be reduced by up to 60% for a limited time.

Charlie Chai, an analyst at 86Research, said Chinese cloud service providers had in the past made efforts to avert a price war but “at the end of the day they still went down this path”. He noted the companies had expanded aggressively and now had too much capacity.

Source: Reuters (emphasis ours)

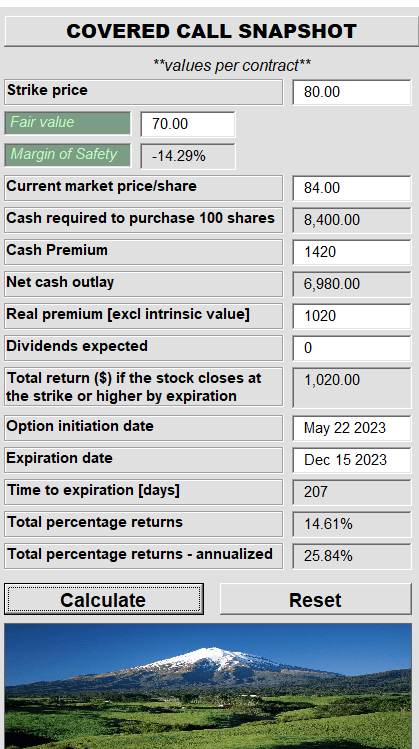

This is a time when we have not officially hit a recession and we are seeing up to 60% price cuts. So for us, both sales and earnings estimates are still too optimistic. The low-PE is a trap. We think that this “six degrees of separation” idea of spinning off all these units by BABA might reduce regulatory risk but will substantially increase overhead costs. It will also decrease pricing power further. We rate the stock a hold and think that those bullish should play it using covered calls (one example shown next).

Author’s App

With zero growth coming, and regulatory risk receding, BABA’s options actually appear quite rich relative to where they should be. Hence covered calls are a better alternative to a direct long.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here