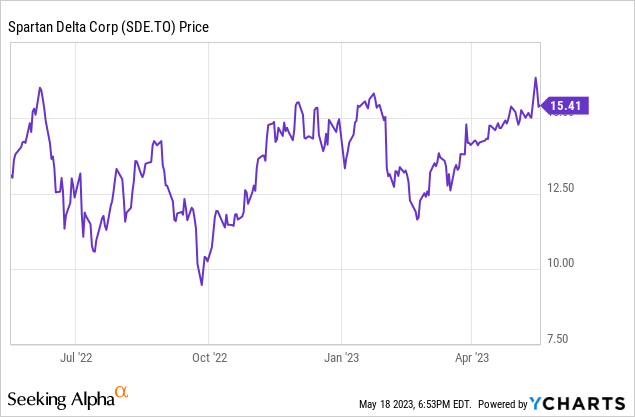

Introduction

Shareholders of Spartan Delta (TSX:SDE:CA) (OTCPK:DALXF) are on the verge of benefiting from a massive cash windfall. While I have been bullish on Spartan Delta for several years, the recent events will speed up the monetization process and provide a cash windfall for shareholders who invested in 2020 (and later).

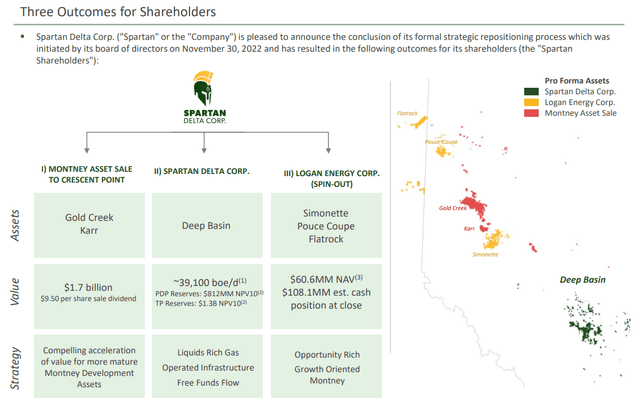

Shareholders can look forward to a massive cash windfall

In March, Spartan Delta announced it has entered into an agreement with Crescent Point Energy (CPG) (CPG:CA) whereby the latter was acquiring the Gold Creek and Karr Montney projects for C$1.7B in cash. That’s a good deal, and Spartan Delta accepted the offer while making it very clear its shareholders will participate in the upside created by this deal.

Long story short, shareholders of Spartan Delta will receive C$9.5/share in cash in a combination of a special dividend and capital repayment, a C$0.10 quarterly dividend, 1 share in Logan Energy (which will own 193,000 acres of land with a production of 4,500 barrels of oil-equivalent per day) as well as 1 share purchase warrant in Logan Energy. And on top of that, the ‘remaining’ part of Spartan Delta that hasn’t been spun out or sold will obviously continue to exist.

Spartan Delta Investor Relations

The Logan spinoff is actually pretty interesting as it appears to become the growth vehicle while the ‘remaining’ Spartan Delta will focus on shareholder returns from its asset base which will produce approximately 40,000 barrels of oil-equivalent per day. The company has published an updated guidance for Spartan Delta 2.0 on a standalone basis (excluding the assets that have been sold or will be spun off).

Moving over to the cash portion of the shareholder rewards, Spartan Delta will pay C$9.50 in a special dividend and capital repayment. While the exact amounts per share still have to be disclosed, Spartan Delta has already published the approximate dollar amounts.

According to the update, the company will distribute ‘up to’ C$540M in assets as a capital repayment. Approximately C$60.6M will be distributed in the form of Logan shares while the remainder, C$479.4M will be paid in cash. There are currently 171.4M shares outstanding, which means the implied cash payment in the form of a capital reduction will be approximately C$2.80. This means the remainder of the C$9.5 cash payment (so C$6.70) will be paid as a dividend, subject to the normal dividend withholding taxes in Canada. Assuming a foreign dividend withholding tax of 15% (your country may have additional tax treaties with Canada, so every investor’s situation will be different), the net cash proceeds from the C$9.5/share distribution will be approximately C$8.50 (again, subject to an investor’s own tax situation). The C$0.10 dividend (payable in July) will be subject to normal dividend taxes. And as mentioned, the Logan shares will be distributed as a capital repayment, and this should be tax-free.

The ‘new Spartan Delta’ will benefit from existing hedges

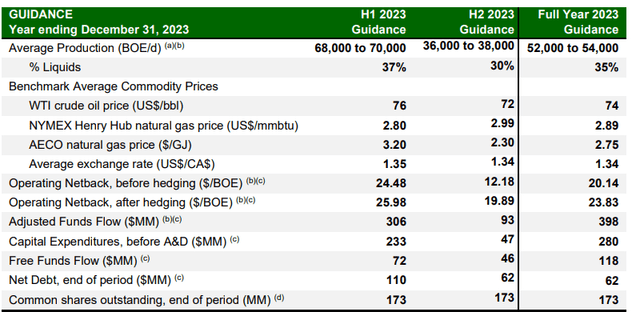

The company has now also published an update on the assets that will stay behind in Spartan Delta. While the spin-out of Logan hasn’t been completed yet and while the cash distribution to the Spartan Delta shareholders still have to occur, Spartan Delta has already published a pro forma guidance update.

It expects to produce 36,000-38,000 barrels of oil-equivalent in the second semester and based on an average WTI price of US$72/barrel and C$2.30 AECO natural gas price, the adjusted funds flow would be around C$93M. After spending C$47M on capex, the underlying free cash flow would be C$46M or just over C$0.25 per share.

Spartan Delta Investor Relations

That’s great but keep in mind the existing hedges will remain with Spartan Delta (and haven’t been transferred to Crescent Point Energy). This means about 2/3rd of the anticipated production has been hedged at an AECO natural gas price of in excess of C$4 which means the average realized AECO natgas price will likely be closer to C$3.75.

Fortunately, Spartan Delta has also provided the operating netback before hedges, and the C$12.18/boe would result in a loss of about C$40-50M in operating cash flow. This does emphasize the importance of a decent natural gas price and fortunately the futures market for AECO natural gas is looking a bit stronger heading into the winter, so hopefully Spartan Delta will be able to secure some additional hedges for next year.

Investment thesis

I first discussed Spartan Delta here on Seeking Alpha in the summer of 2020 (calling it a ‘once in a decade opportunity’) when the stock was trading at around C$3/share, so getting a cash payment of C$9.50/share (after already receiving C$0.50/share earlier this year) means I will receive in excess of 300% of my original investment within 3 years after buying the stock.

The main unknown element here is the share price of Spartan Delta after completing the cash payments and after completing the Logan spinout. I would expect a share price of C$4-6 to be pretty reasonable, but there’s no guarantee.

I have a substantial long position in Spartan Delta, and I am looking forward to seeing the cash hitting my account. Depending on the share price level of Spartan after completing all the cash and stock payments, I may add to this position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here