I just finished my weekly review of what the Federal Reserve seems to be doing.

I closed with my concern about whether or not the Federal Reserve is really doing enough with its current effort at quantitative tightening.

The Federal Reserve has been removing securities held outright from its portfolio for more than 12 months now.

But, there is still the concern that the Fed’s targets to constrain the money going into the economy are too minuscule.

The Fed, in its move to protect the economy from the Covid-19 pandemic, pumped trillions of dollars into the banking system.

The amount of money the Fed appears to removing from the economy does not seem sufficient to reverse what it did previously.

In effect, over the past four years or so, the Federal Reserve has created an asset bubble…but, the “down” side of the bubble does not seem to be anywhere as large as the “up” side.

Furthermore, people and businesses are not “using” money nearly as often as in the past. That is, the velocity of circulation of the money stock has fallen so low that most of the money actually being pumped into the economy seems to be going into the financial sectors of the economy and not into the purchases of “real” goods and services.

Let’s look at this picture.

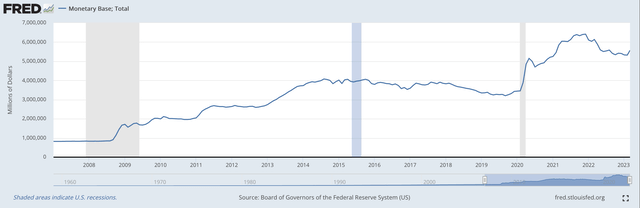

Monetary Base

The monetary base, the foundation of the money stock, has risen rather radically since the start of the Great Recession in December 2007.

Here is the chart for the monetary base over the past 16 years or so.

Monetary Base (Federal Reserve)

The Fed began its program of quantitative easing in the 2010 period. As can be seen, the monetary base increased fairly steadily into 2015 and then slowed down for a while.

Then, in 2020, the monetary base accelerated as the Fed pumped money into the banking system.

And, the monetary base kept on increasing up until March 2022, when the Federal Reserve began to tighten monetary policy.

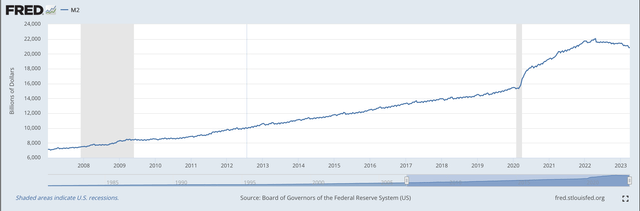

M2 Money Stock

The M2 money stock rose along with the increase in the monetary base.

Look at what happened to the M2 money stock as measured, but not seasonally adjusted.

M2 Money Stock (Federal Reserve)

The money stock, from before the start of the Great Recession, grew very, very steadily up until the impacts of the Covid-19 pandemic hit.

Then Fed Chair Jerome Powell generated the Fed’s asset bubble.

The cry here was always, “err on the side of monetary ease.” Don’t make a mistake on the downside.

Note, however, there was not one real downturn in the rise of the M2 money stock until 2022, when the Fed began its quantitative tightening.

Lots and lots of money got pumped into the banking system during this entire period. What did people… and businesses… do with all that money?

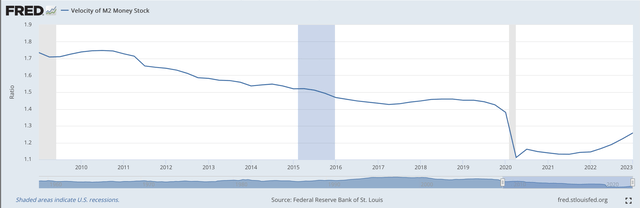

M2 Velocity

Well, the velocity of circulation of the money stock fell.

Velocity of M2 Money Stock (Federal Reserve)

I’m going to divide this time period up into two sections: the period up to the beginning of 2020, and then from that period up to the present.

Up to early 2022, the Federal Reserve followed a very consistent policy of quantitative easing.

One of the major things that then-Fed chairman Ben Bernanke apparently wanted to achieve was a slow, consistent thrust of monetary policy.

In looking at this chart up to 2020, this is what the Federal Reserve achieved.

The growth of the M2 money stock was also relatively stable.

But what the first part of this chart shows is that economic units were slowing down the velocity of the circulation of the M2 money stock and putting more and more money into “assets” rather than spending the money on goods and services.

During this period of time, the stock market also advanced, and increased at a slow, steady pace. There was little risk associated with investing in the stock market, and there was a pretty good return in the stock market throughout this whole period of time.

Sophisticated investors put more and more and more money into these assets, taking advantage of the “asset price bubble” that the Federal Reserve was creating.

Less and less money turned over in the purchase of real goods and services.

The real economy only grew by about 2.2 percent during this time period. Consumer prices also increased by about 2.2 percent during this time period.

The decline in the velocity of circulation of the M2 money stock captures, very closely, this narrative.

At the start of the 2020s, when the Fed was pumping a huge amount of reserves into the banking system, the velocity of circulation of the M2 money stock plummeted.

As I described in many of my posts over this period of time, investors were looking all over the place for opportunities to put the money they could get hold of.

Even more massive amounts of money went into financial assets.

This has created its own problem, but it also took lots and lots of money out of the spending stream, only to drive up assets prices.

The Current Period

Now, we get into the current period of time.

The Federal Reserve has run a program of quantitative tightening for more than 12 months.

Interest rates have risen rather dramatically as the Federal Reserve has raised its policy rate of interest 10 times since the middle of March 2022.

And, the velocity of circulation of the M2 money stock has risen… modestly.

This is the thing.

There is lots and lots of money in the financial system. As investors put a major amount of this money into asset markets, creating an “asset price bubble,” we got rising asset prices but very little economic growth.

Then things began to change.

Consumer price inflation began to increase. In fact, consumer price inflation increased at such a rapid pace that the Federal Reserve decided that the increase was not just a “temporary phenomenon”…it was a real, permanent problem.

And, the Fed began its program of quantitative tightening.

But, how far does this quantitative tightening have to go?

This, to me, is turning into the major question.

This, to me, means that we have to pay more attention to the spending and investing habits that people engage in.

If velocity now begins to increase more rapidly, the Federal Reserve may have a much tougher job to accomplish than was thought.

As the asset bubble was increasing, the velocity of circulation of the M2 money stock was decreasing.

Now, the asset bubble seems to be declining and the velocity of circulation of the M2 money stock is increasing.

If this continues, the Federal Reserve will just have to work stronger… and longer… to get its inflation target down to around 2.0 percent.

Can the Federal Reserve “stick it out” for that long of a time period?

Looks like we are going to find out which scenario is going to hold… velocity stays constant at its current low level… or velocity begins to accelerate its rise.

Read the full article here